We have updated our US consumer outlook chart book, see the attached PDF.

US Consumer Still Strong

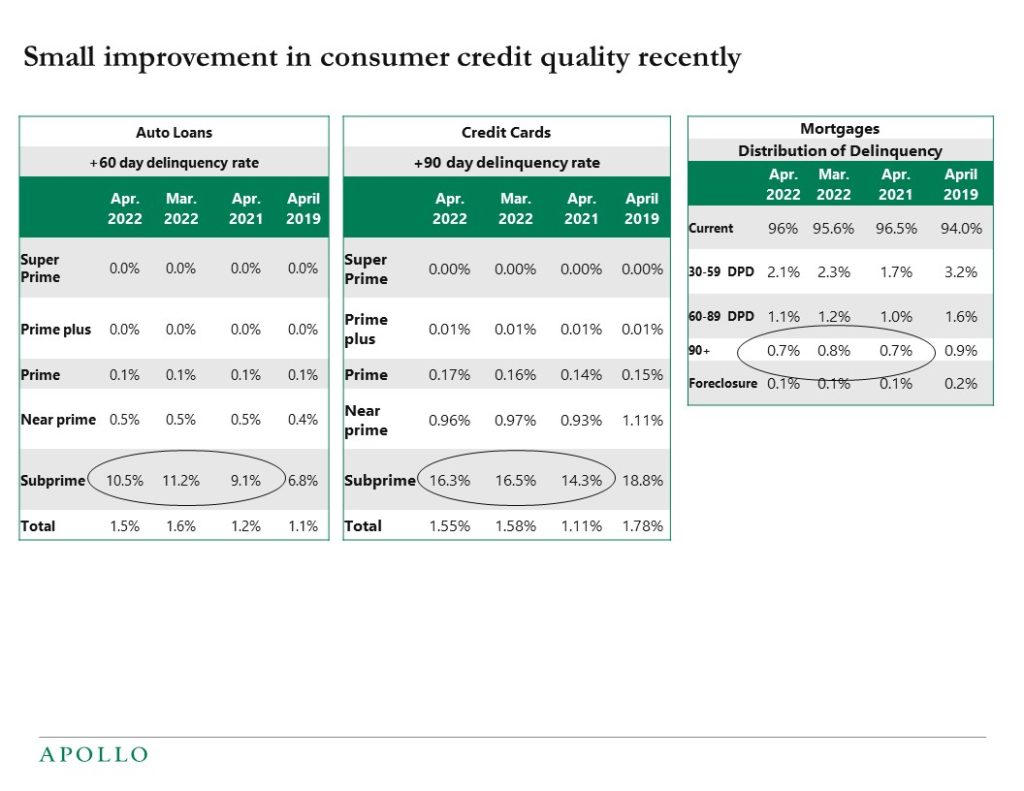

After a brief period of rising delinquency rates on credit cards and auto loans for subprime borrowers, the latest data shows a modest improvement in consumer credit quality with delinquency rates falling, see table below. This is consistent with a strong labor market, high wage growth, and a high level of household savings. US consumer spending will eventually grow at a slower pace because this is what the Fed wants to see, but the bottom line is that there are no signs yet in the macro data of the US consumer slowing down.

Two Questions for Investors

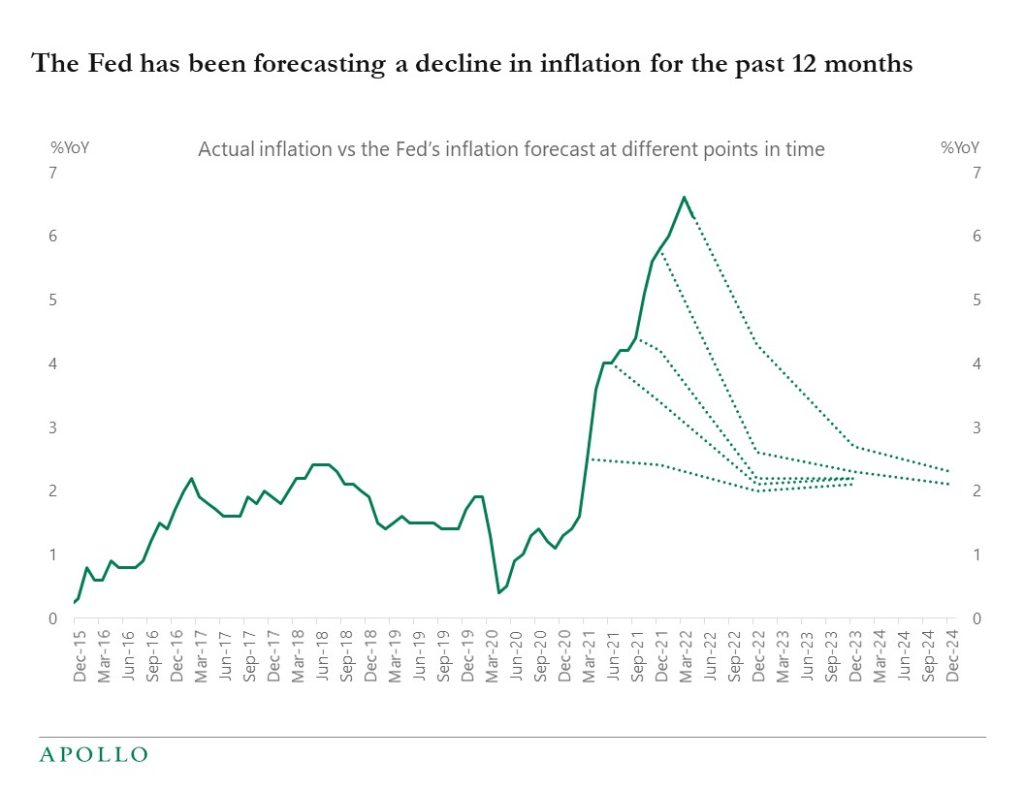

The Fed and markets continue to expect a quick reversal in inflation back to the Fed’s 2% target, see chart below. This raises two questions for investors: As the Fed destroys demand to cool down inflation, what level of the unemployment rate is required to achieve this path, and can the Fed engineer a soft landing without increasing the unemployment rate too much and thereby triggering a recession?

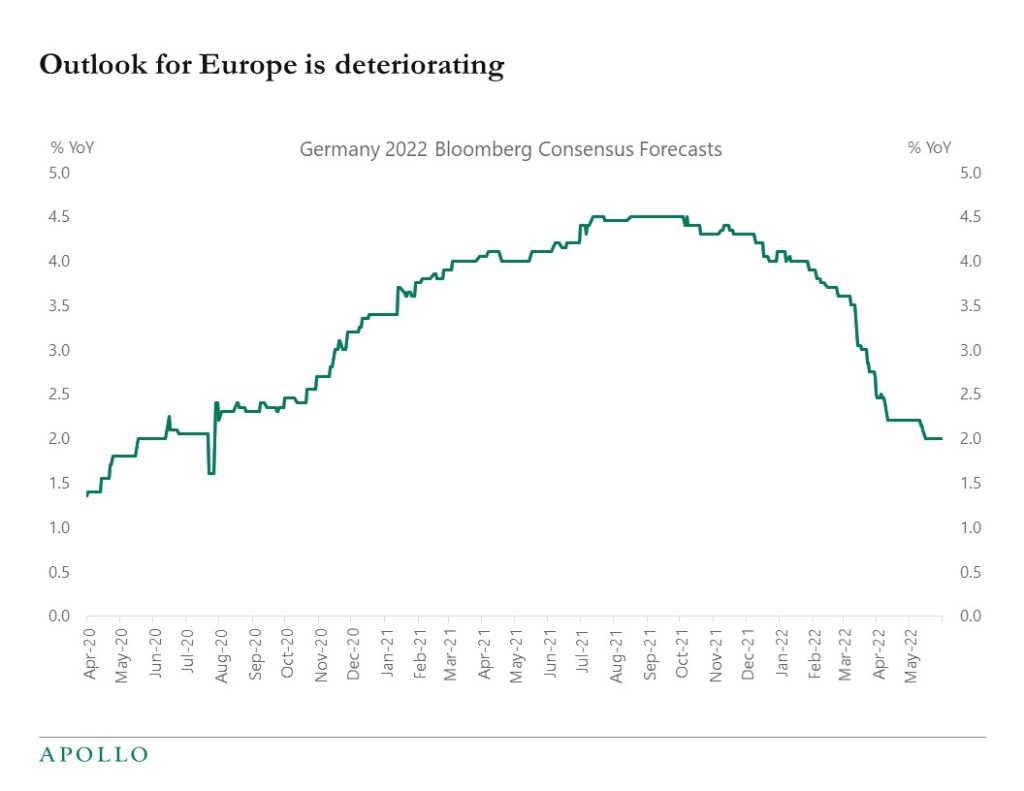

Outlook for Europe Deteriorating

The consensus continues to downgrade growth expectations for Europe, raising questions about ECB rate hikes and the rising risk of loan losses and defaults in Europe, see chart below.