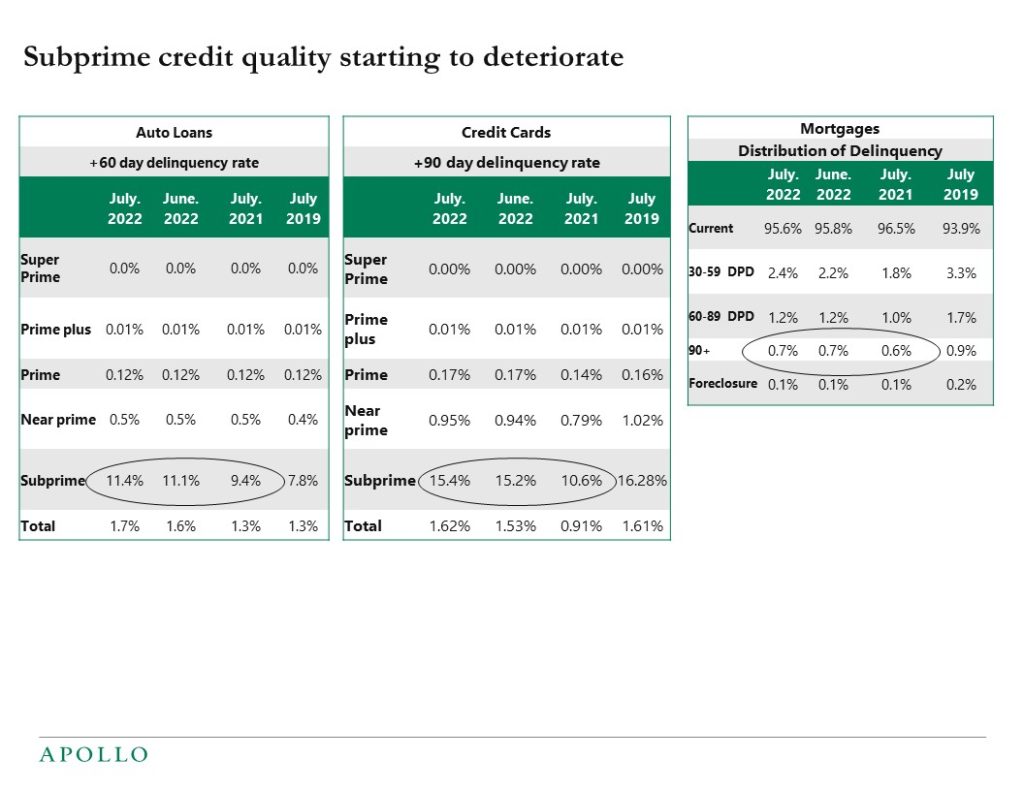

Delinquency rates for subprime borrowers are starting to rise, see chart below.

Delinquency rates for subprime borrowers are starting to rise, see chart below.

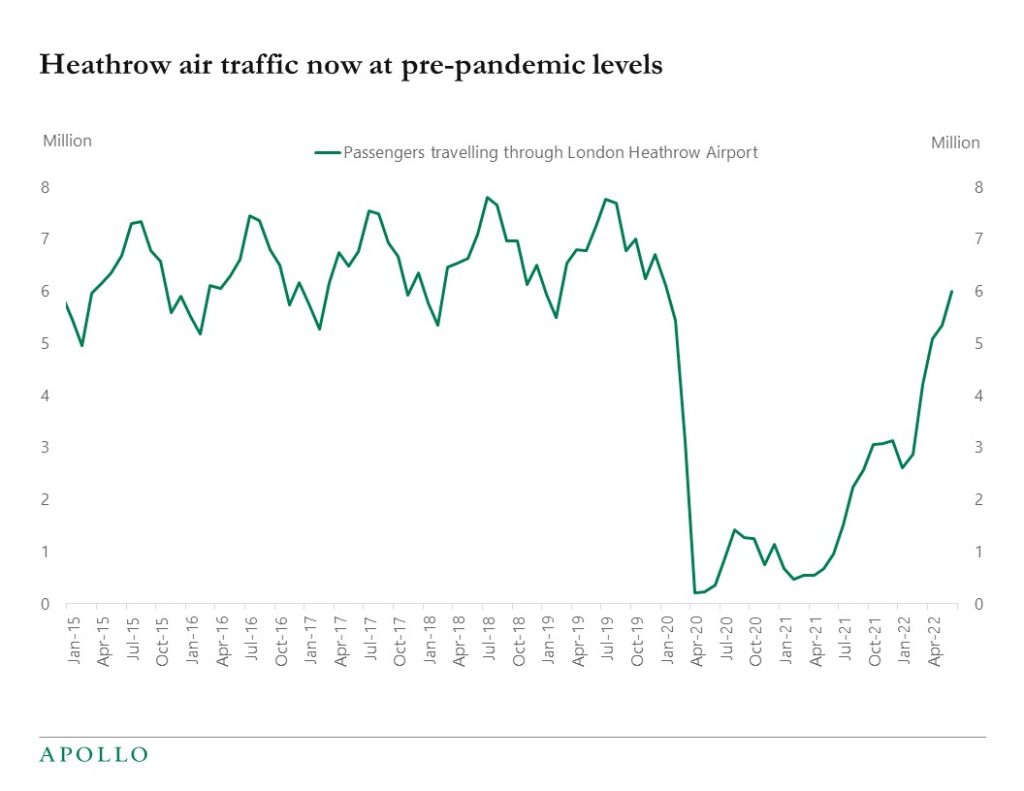

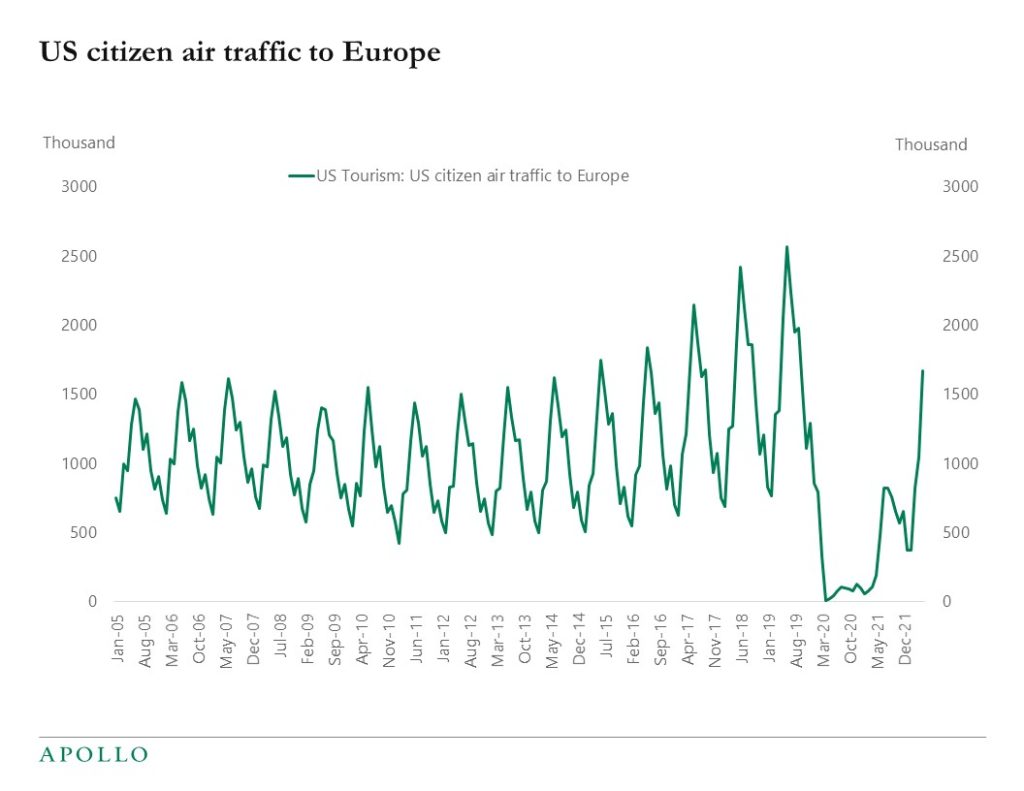

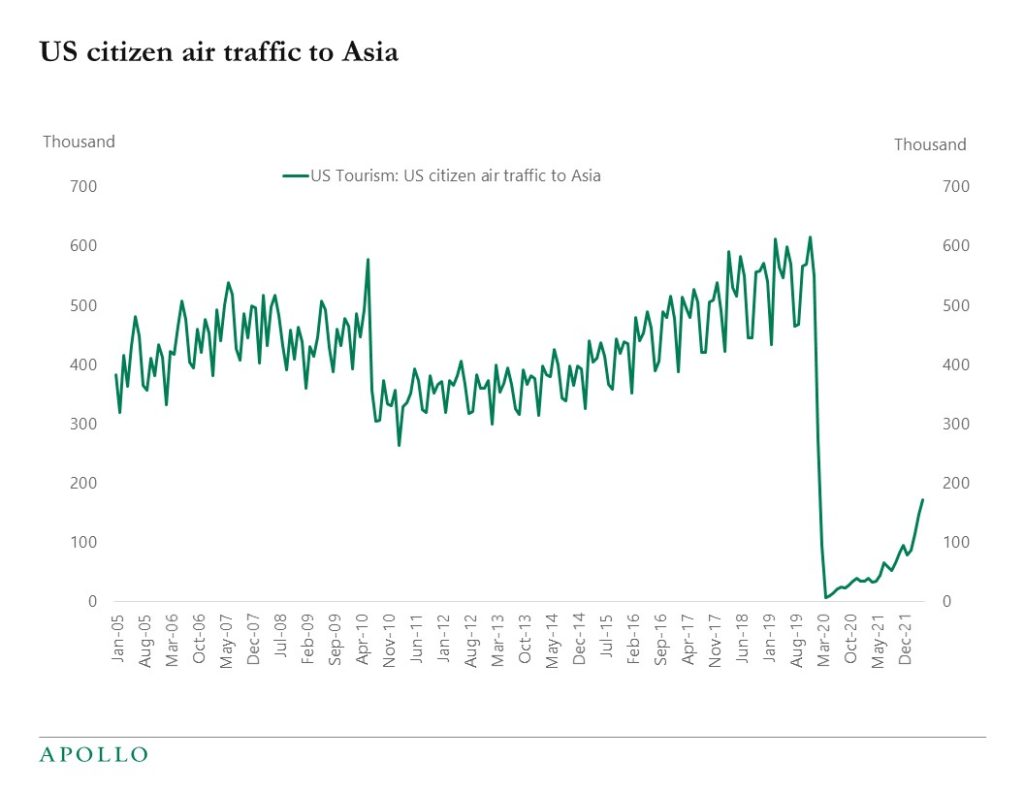

Air traffic in London’s Heathrow airport is back at pre-pandemic levels, and US air traffic to Europe is also at pre-pandemic levels, but US air traffic to Asia is still significantly below 2019 levels, see charts below.

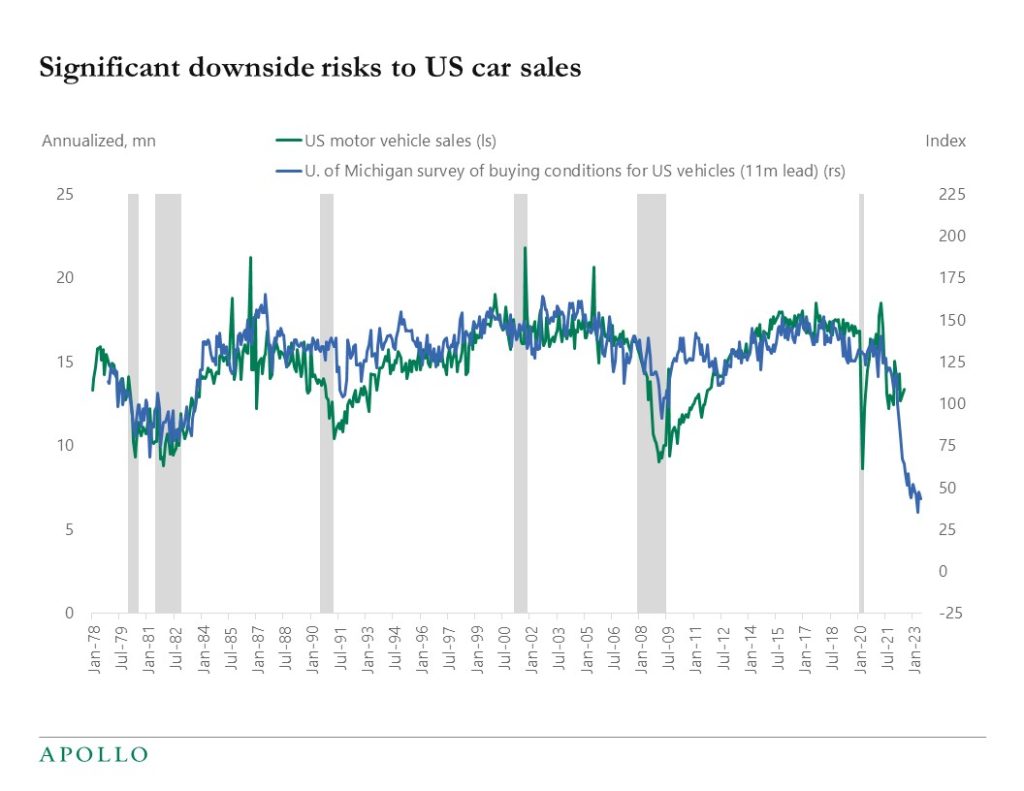

The interest-rate sensitive components of GDP are starting to respond to higher rates and recession worries, see charts below

Last week, Federal Reserve Chairman Jay Powell delivered a hawkish speech at the Jackson Hole Economic Symposium. Specifically, he pointed out that inflation remains much too high and that we should expect the Fed to keep rates elevated for an extended period of time. This resulted in a market sell-off and also indicates that the Fed will not turn dovish anytime soon. This week, we will receive the August employment report. The consensus expects non-farm payrolls to come in at 300,000 and for the unemployment rate to remain unchanged at 3.5%. If the consensus is correct, the labor market remains relatively strong despite the Fed’s efforts to cool the economy down to combat high inflation. However, the economy is starting to show some cracks, for example in interest-rate sensitive components of GDP like housing and auto sales. In this edition of the Weekly Brief, we take a closer look at the University of Michigan’s survey of buying conditions for US vehicles, which shows a significant decline in the months ahead.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.

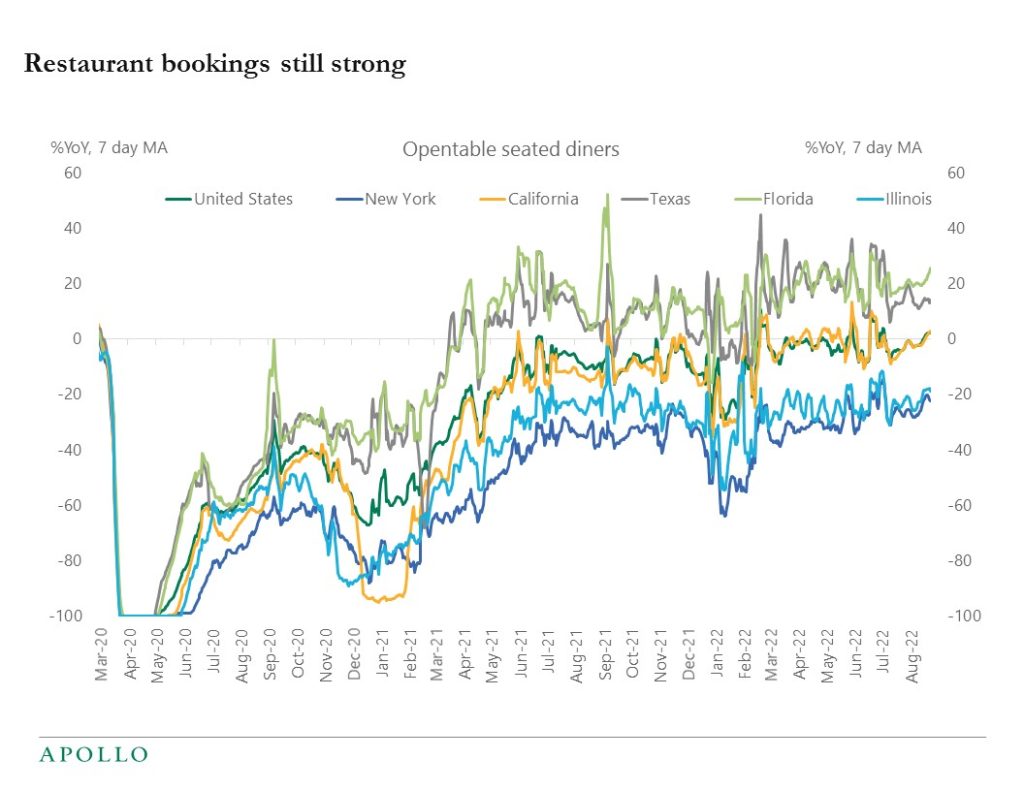

Weekly jobless claims declined this week and US indicators for air travel, hotel bookings, and restaurant visits continue to show no signs of slowing down, see chart below. Inflation at 8.5% is too high, and the labor market is overheated, with unemployment at 3.5%. The only part of the economy slowing down is housing. Our weekly Slowdown Watch is available here.

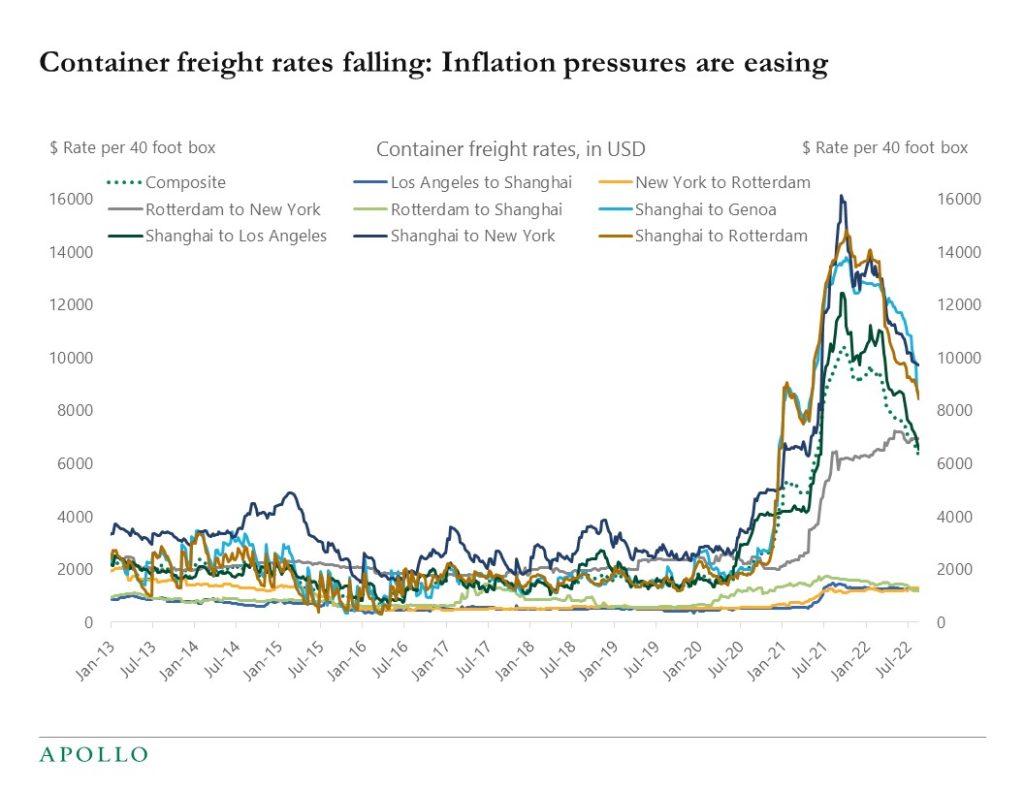

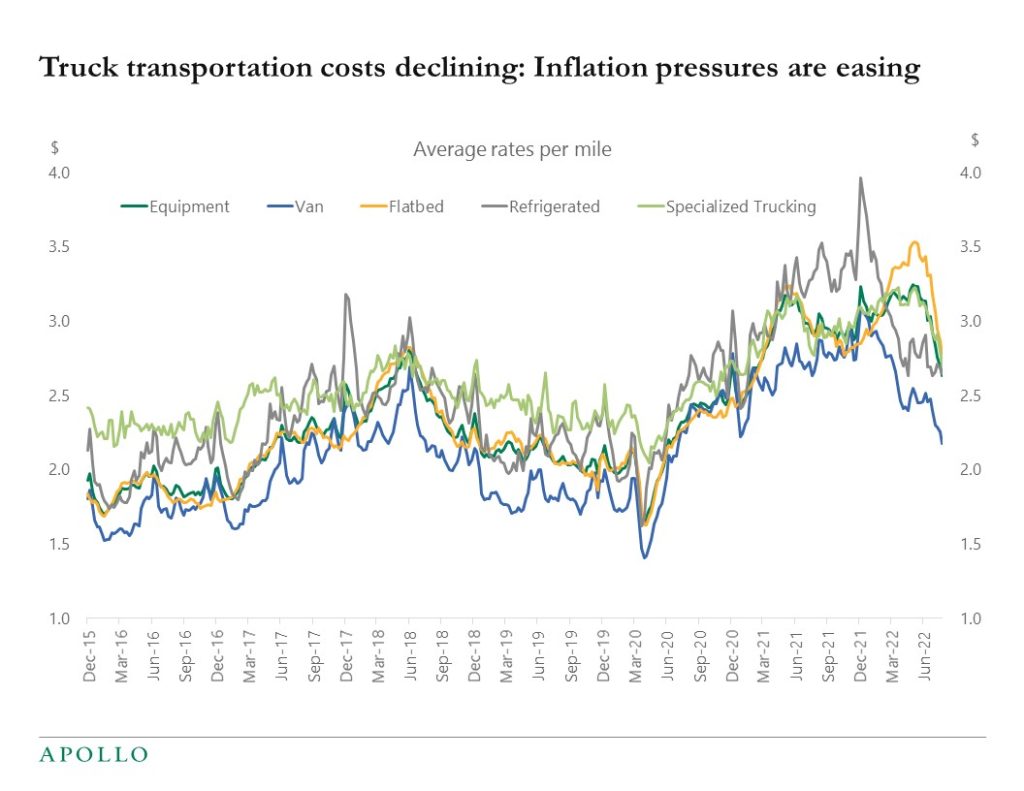

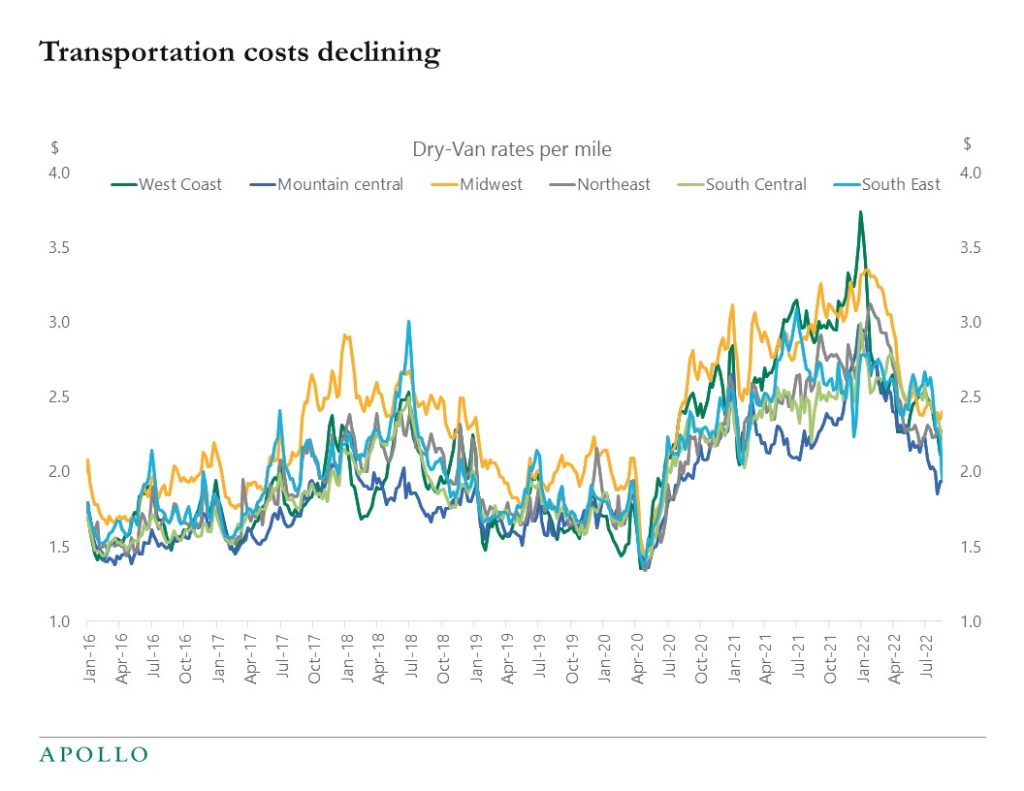

The costs of transporting goods are normalizing across all types of transportation, see charts below. For example, the dry van spot rate per mile has declined over the past six months from $3 to $2. This is all putting downward pressure on inflation and costs of production.

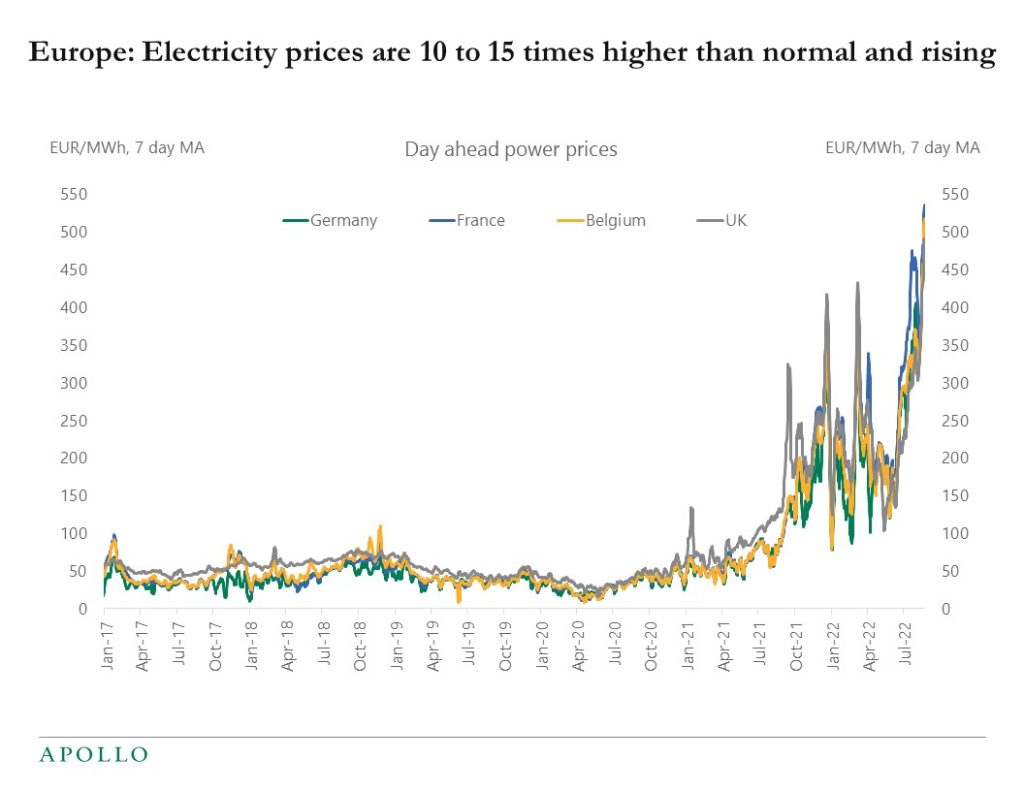

The energy crisis is intensifying in Europe, and the significant increase in natural gas prices and electricity prices is starting to spill over to the US economy. Once a week we will update this outlook.

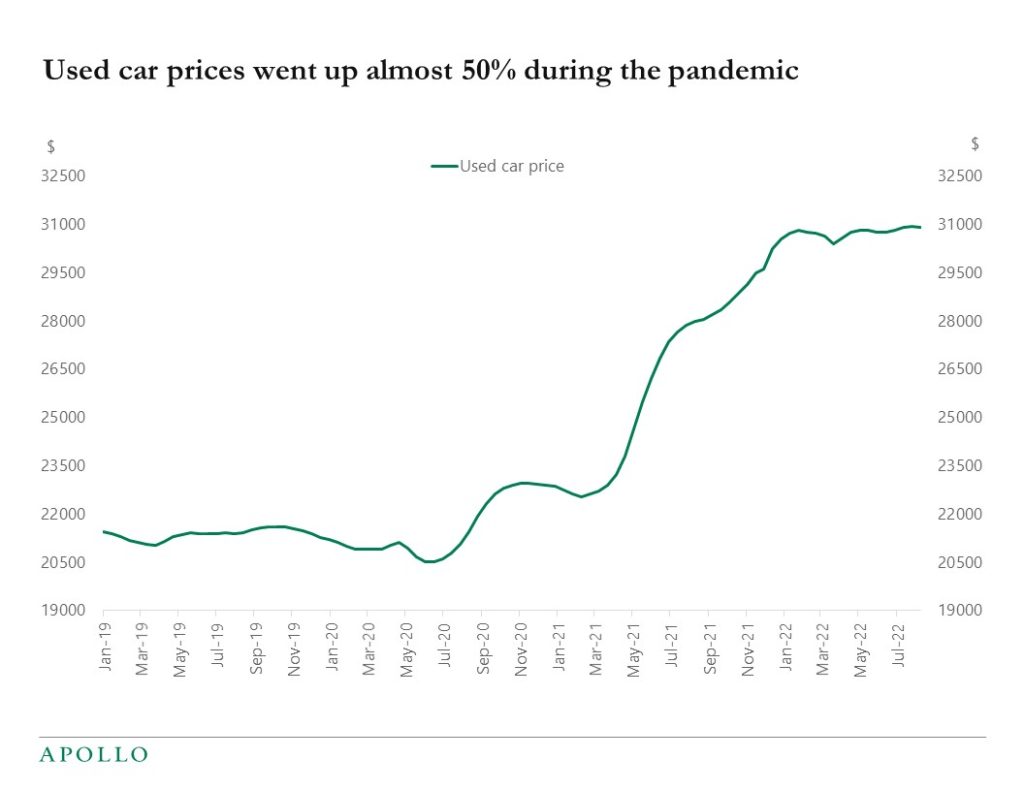

Why did used car prices go up 50% during the pandemic, was it because of more demand for vehicles, or was it because of supply chain problems with semiconductors? The answer to this question will determine where the Fed funds rate will peak during this cycle.

Specifically, identifying the sources of the increase in inflation is essential for understanding how quickly inflation will return to the Fed’s 2% target. A recent Fed working paper suggested that only 1/3 of the inflation increase during the pandemic was due to demand. If that is the case, the Fed today will not need to destroy much demand, and inflation will automatically come down to 2% again.

With supply chains improving every day and growth slowing, the trend in inflation should be lower. If supply problems mainly drove the run-up in inflation, then inflation could come back to 2% faster than the market currently thinks. In that case, a soft landing is likely, and equities and credit should be trading higher.

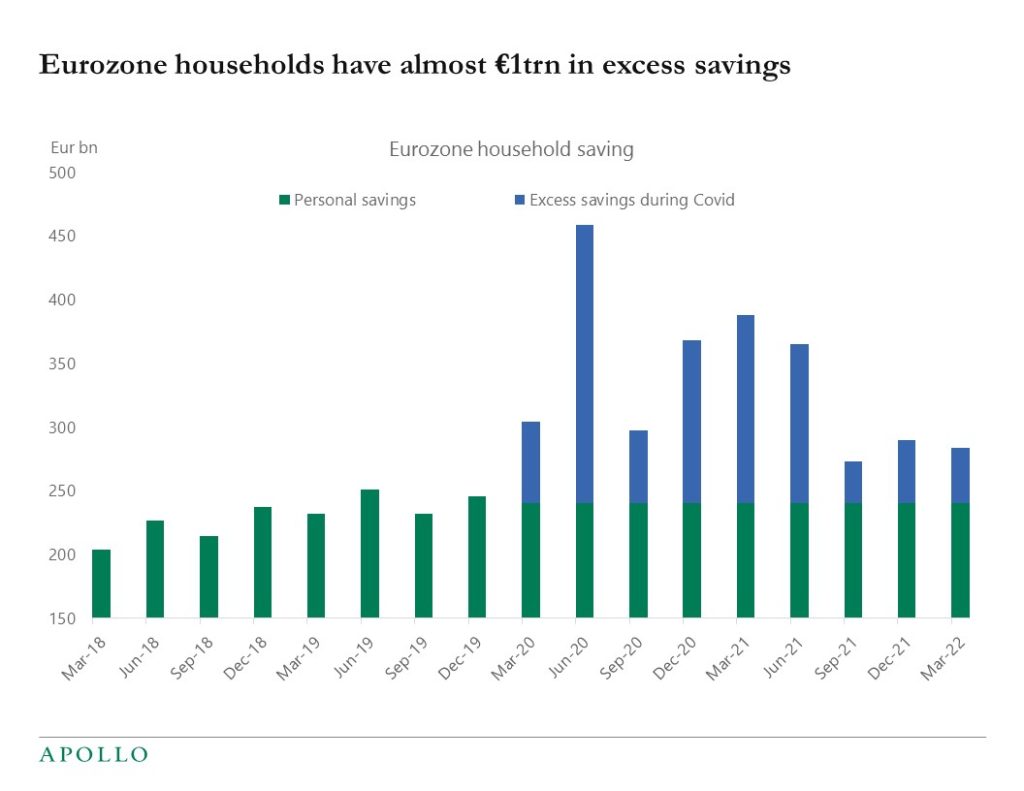

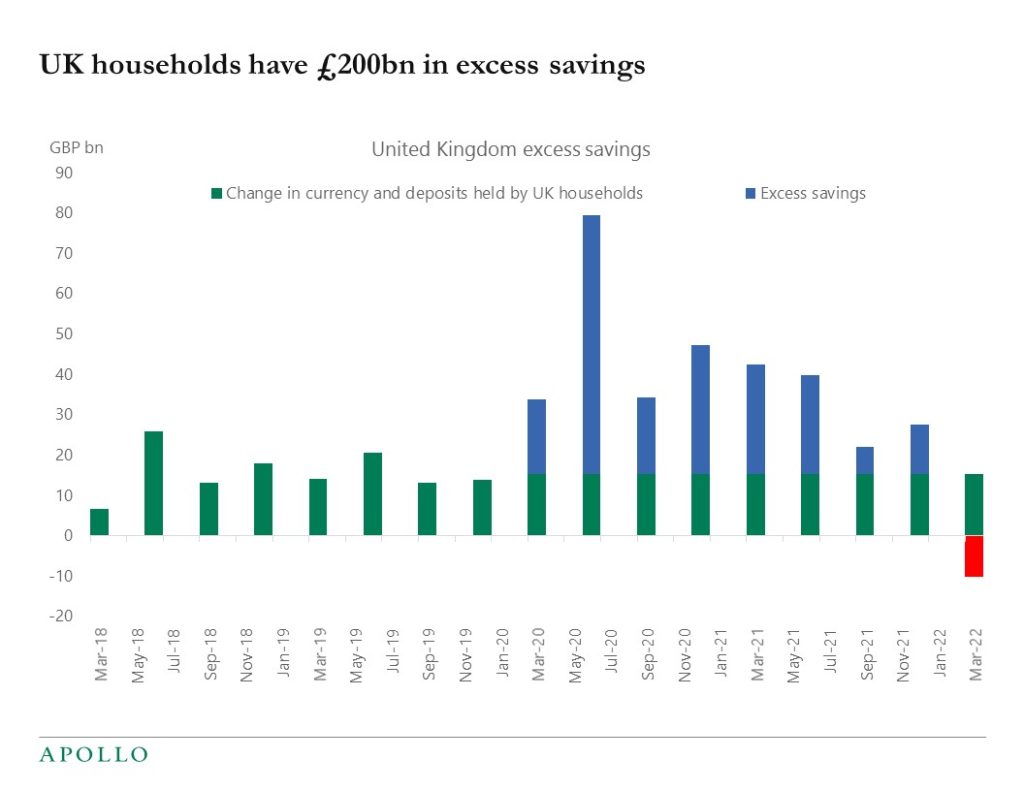

A high level of savings in the household sector during covid can also be seen in the Eurozone and in the UK, see charts below. This is a tailwind for the outlook for consumer spending across Europe. The headwinds to European private consumption include slowing growth, sanctions, and higher inflation, including higher energy prices.