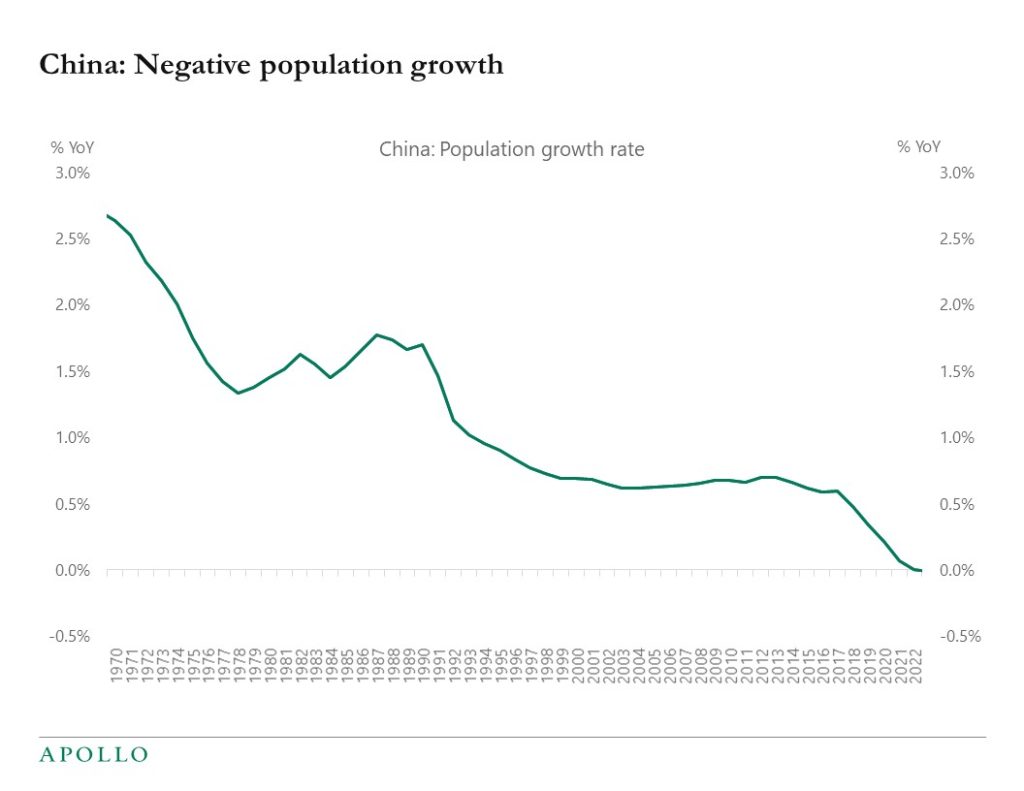

The latest data from the United Nations shows that population growth is now negative in China, see chart below.

The latest data from the United Nations shows that population growth is now negative in China, see chart below.

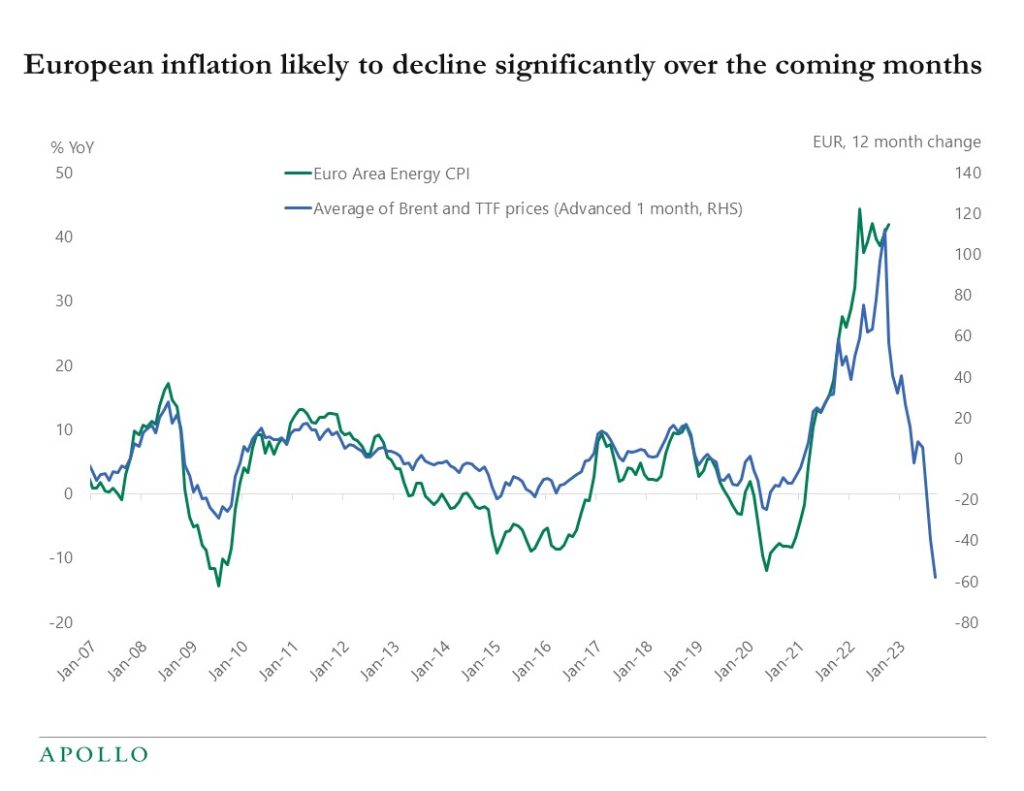

Euro area inflation in October came in at 10.7%, much higher than the ECB’s 2% inflation target. The sub-components showed a 42% increase in energy prices and a 4% increase in service prices.

With European energy prices coming down significantly at the moment, energy will soon turn into a significant drag on European inflation, see the first chart below.

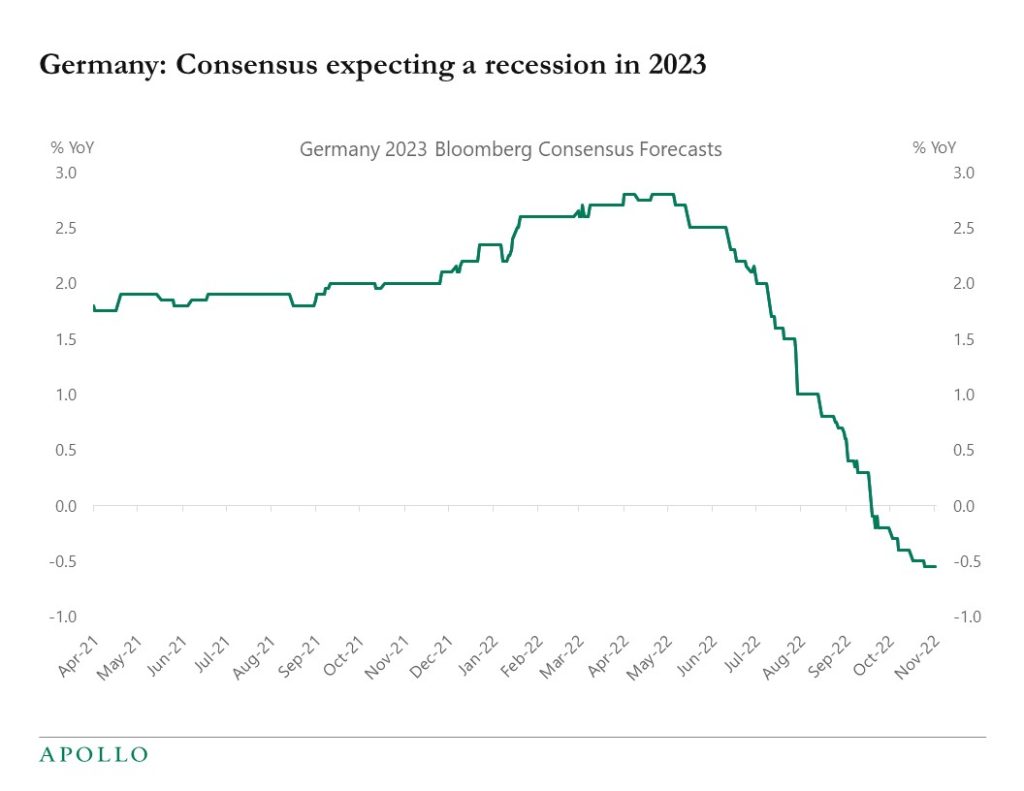

Combined with Germany likely having a recession in 2023, European inflation will soon come down very quickly, see the second chart.

The bottom line is that inflation in Europe is mainly energy. Whereas in the US, inflation is much more broad-based.

As a result, the ECB will soon turn even more dovish. And the Fed will have to remain hawkish.

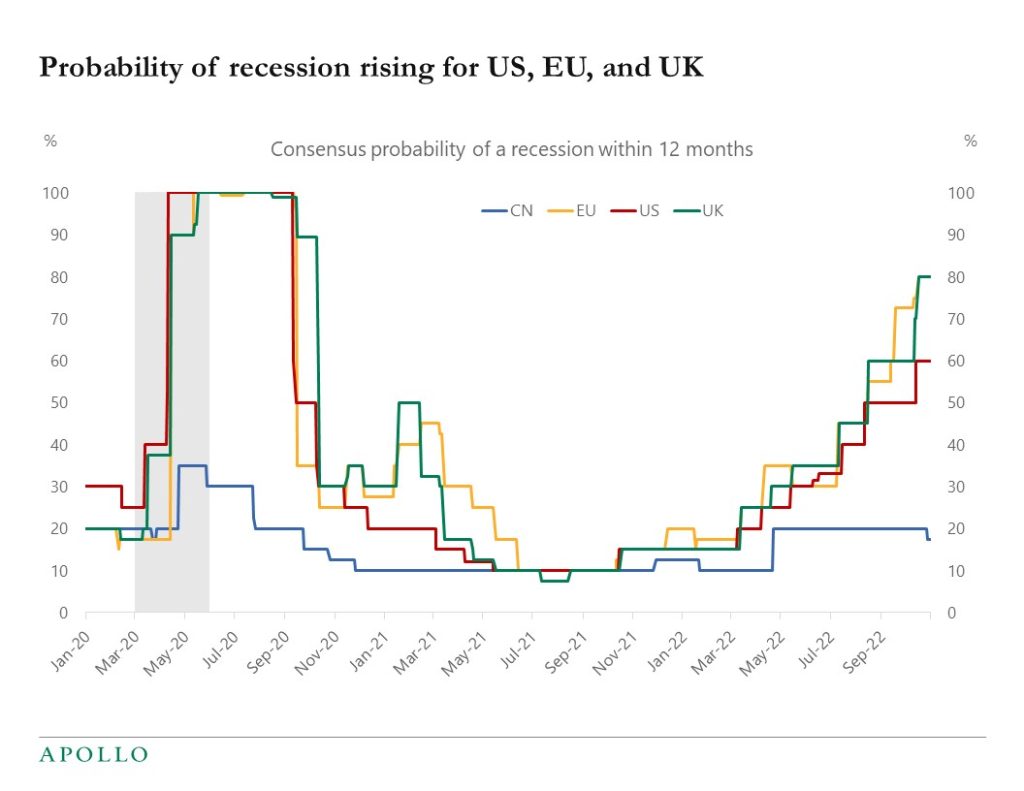

The consensus now sees a 60% chance of a recession in the US over the next 12 months. For Europe and the UK the probability is 80%, see chart below.