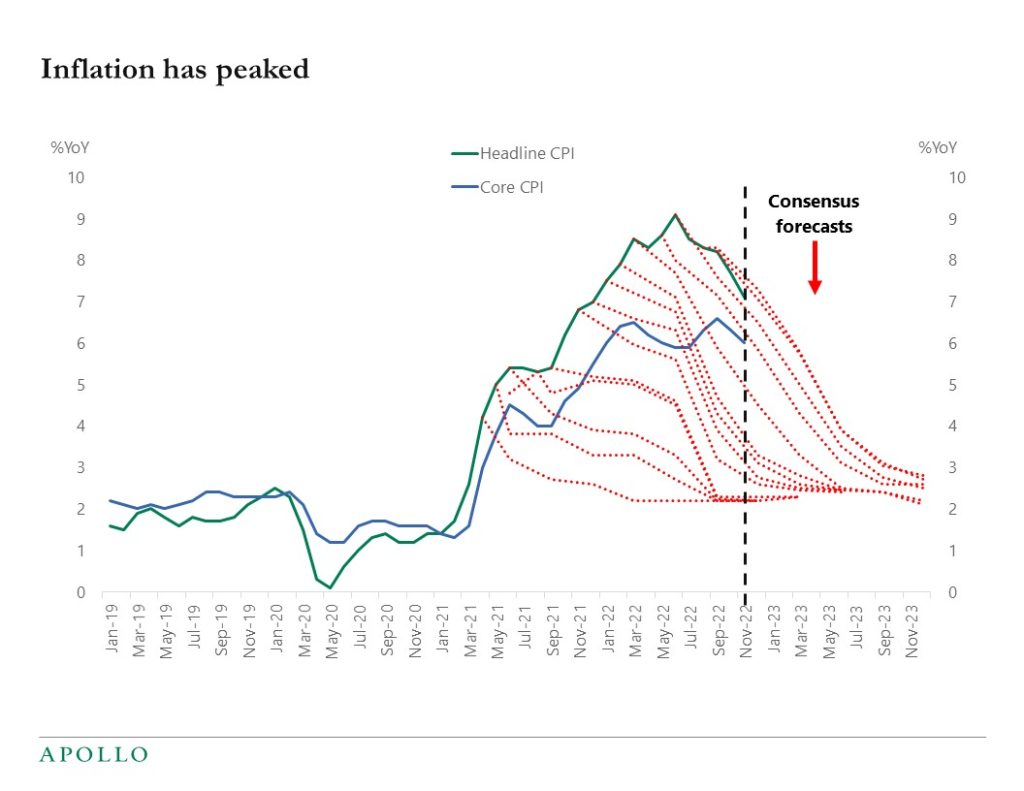

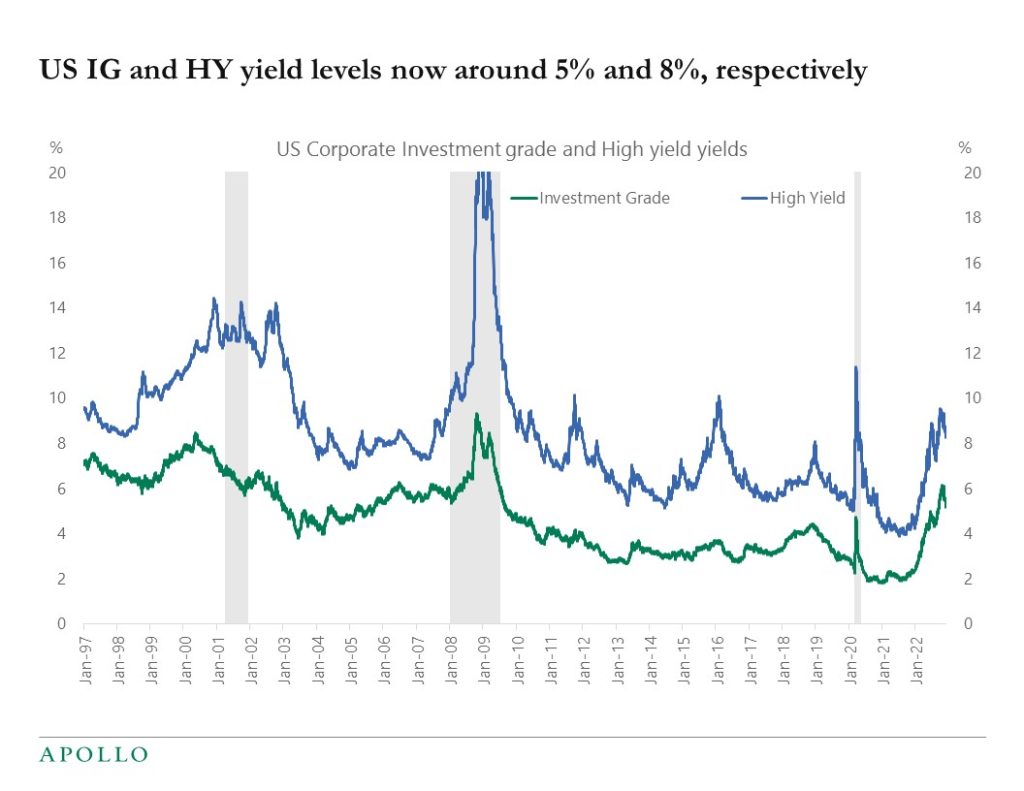

I will be on Bloomberg TV today at 8:30 am to preview the Fed meeting. Inflation continues to trend lower, which is good news for the Fed and markets. But the level of inflation at 7.1% is still significantly above the FOMC’s 2% inflation target. As a result, the Fed today is likely to argue that rates need to remain high for an extended period to ensure that inflation gets all the way back to 2%.