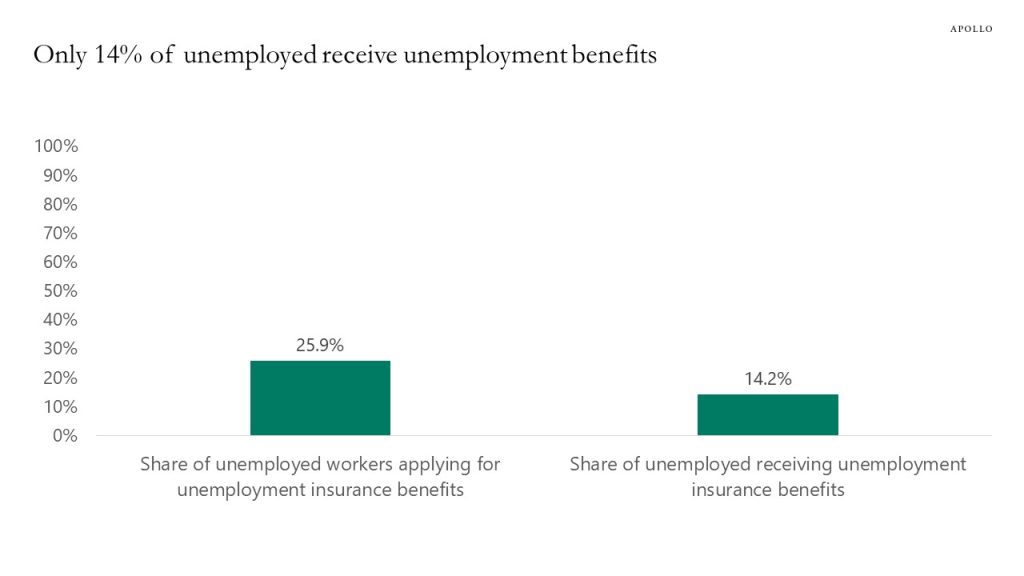

With hiring in the service sector and layoffs in the tech sector, jobless claims may underestimate the ongoing slowdown in the labor market because only 14% of unemployed receive unemployment insurance benefits, see chart below. In other words, with a strong service sector and a weak tech sector, jobless claims may not be a good reflection of what is happening in the labor market.