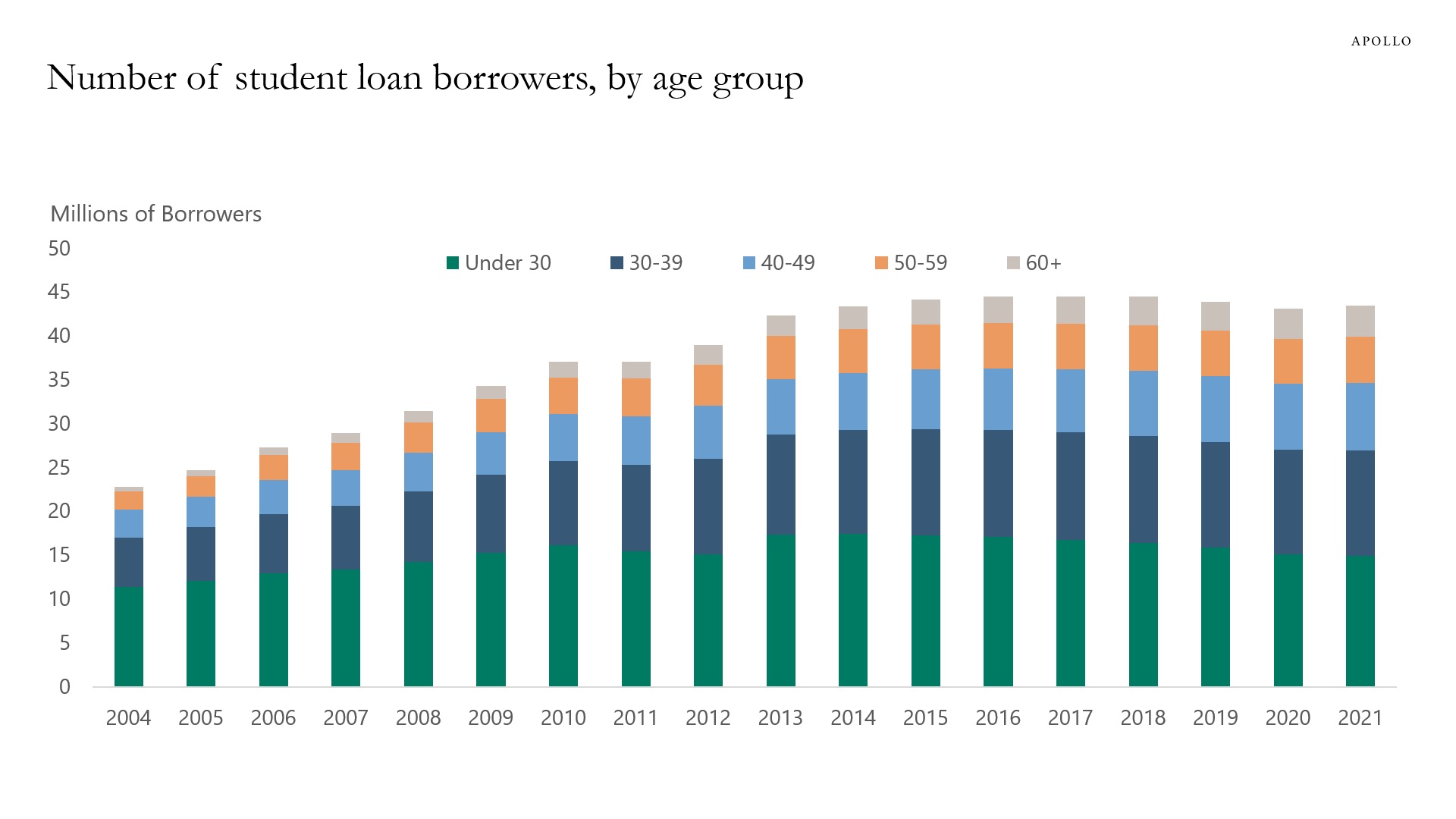

There are a total of 45 million people with student loans, and the average monthly student loan payment is around $200. So resuming student loan payments in October will subtract roughly $9 billion from consumer spending every month, or roughly $100 billion a year, and this will mainly have an impact on younger households, see chart below.