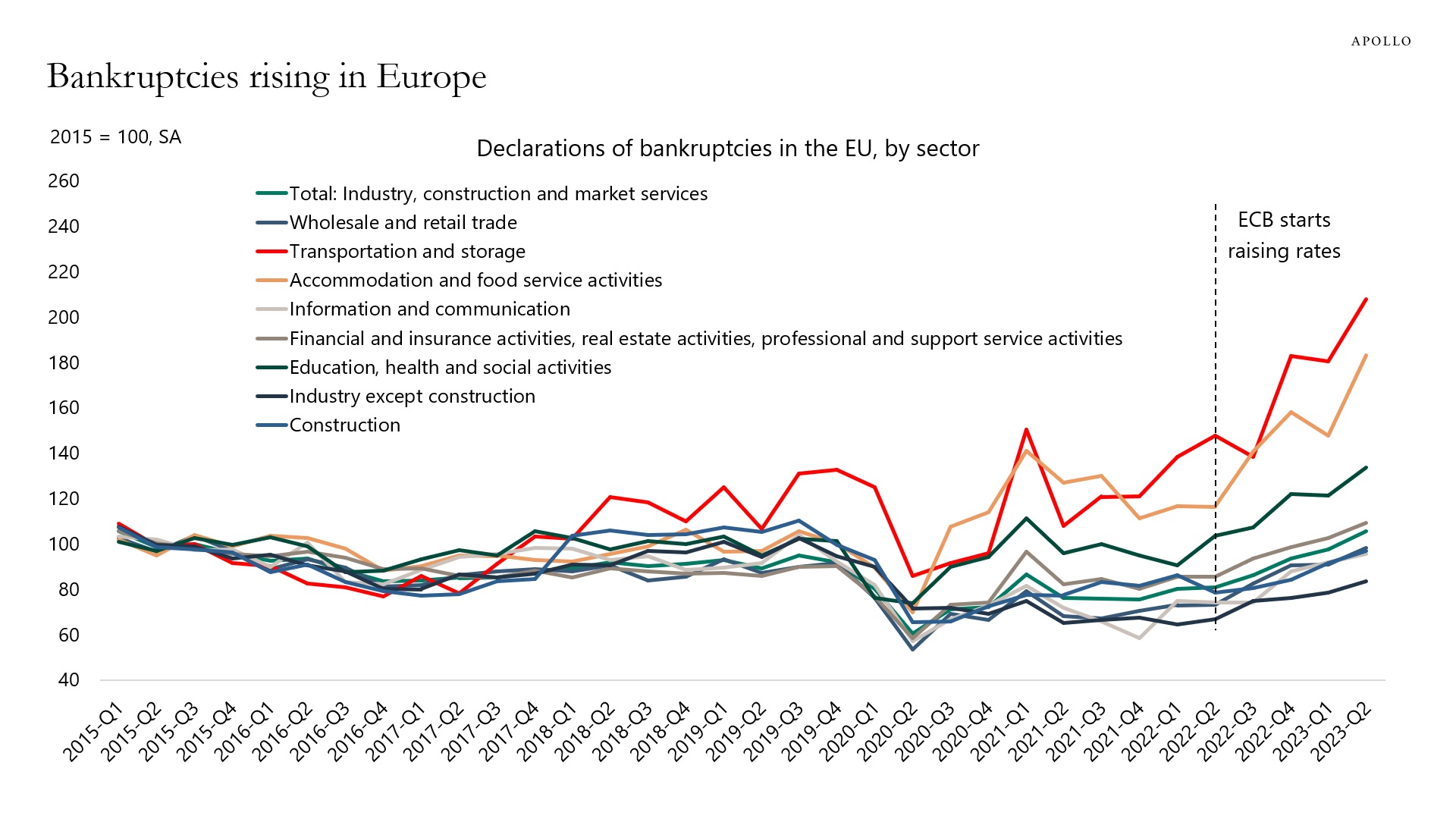

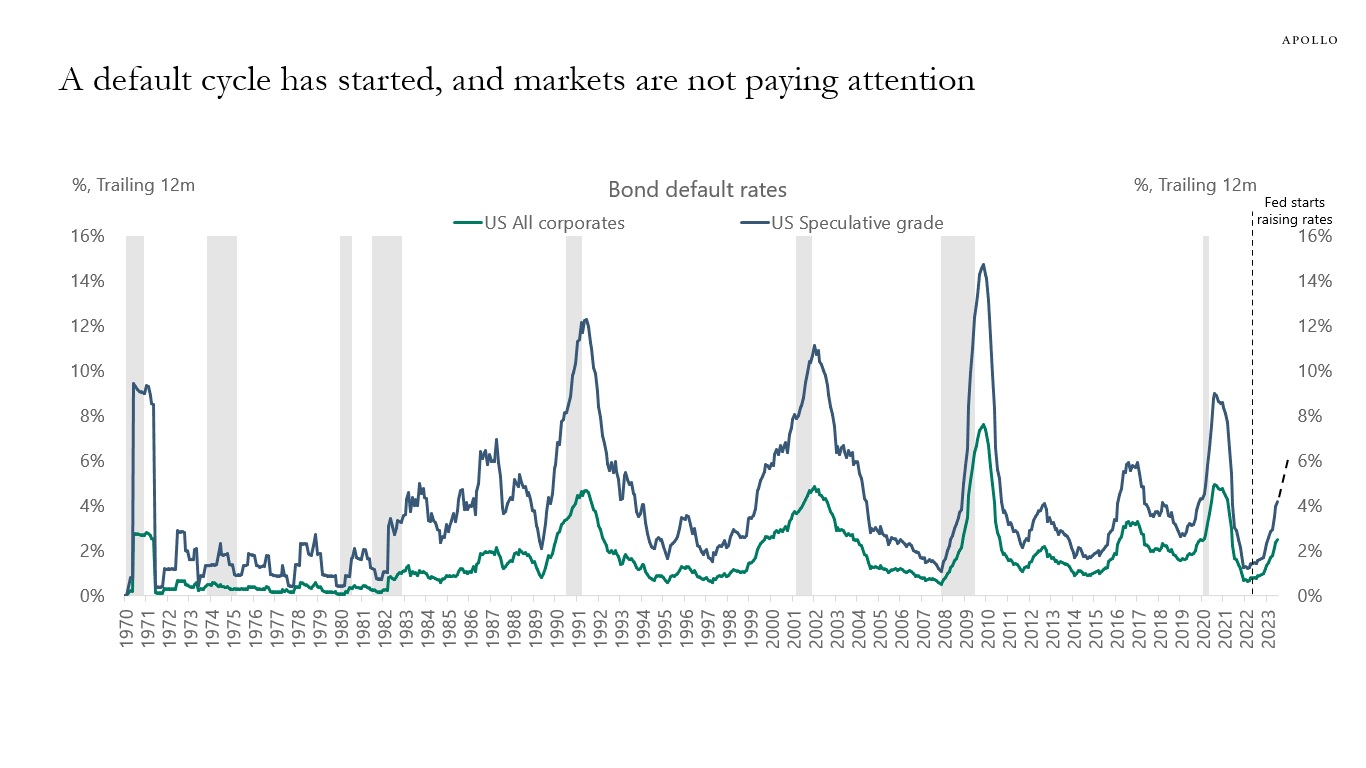

Since the ECB started raising rates in July 2022, corporate bankruptcies have trended higher, driven by transportation and storage; accommodation and food services; and education, health, and social activities—see chart below.

With the ECB keeping rates high well into 2024, we should expect these trends to continue.