It is inconsistent to say that the incoming economic data is strong but the labor market is weakening.

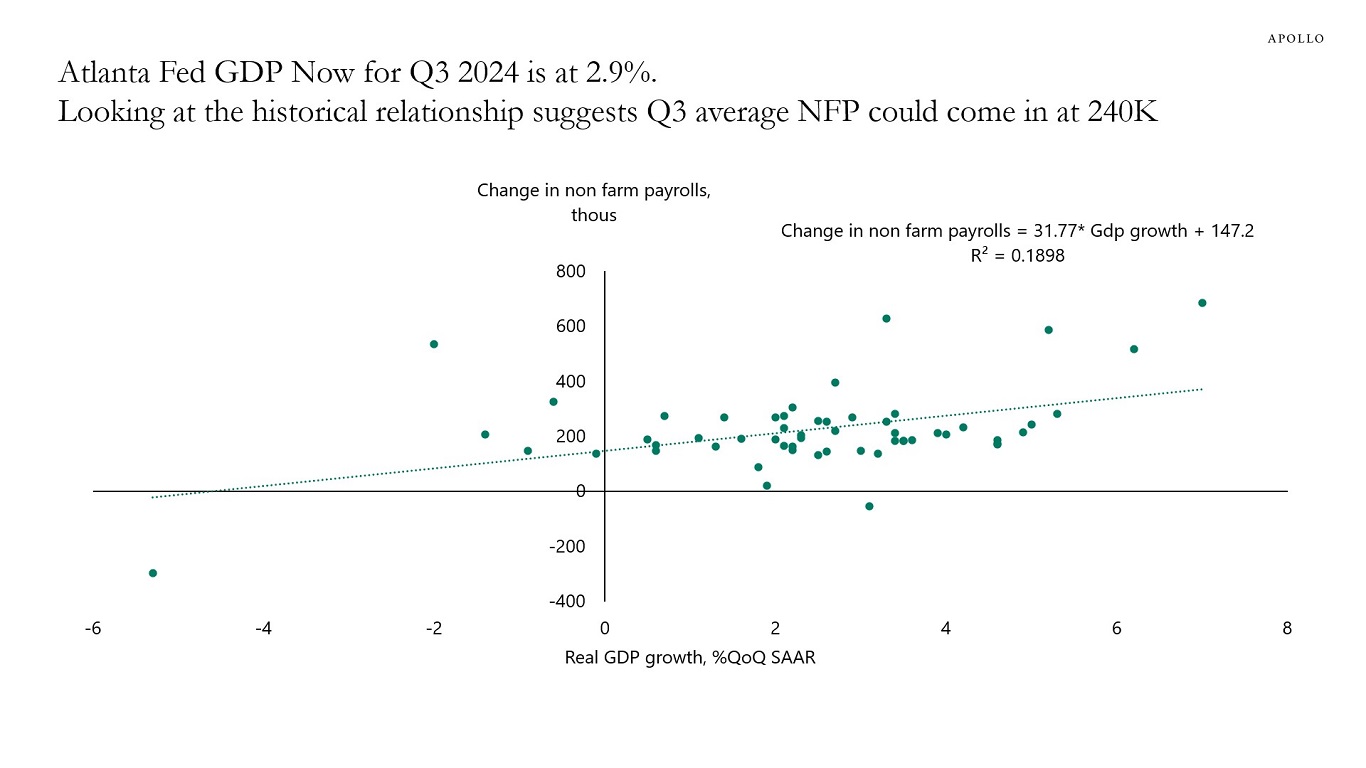

For example, if the Atlanta Fed GDP Now estimate is 2.9%, significantly above the CBO’s 2% estimate of long-run growth, then job growth is accelerating and the unemployment rate is declining.

With the data for consumer spending, capex spending, and government spending still strong, we should soon begin to see a rebound in nonfarm payrolls and a decline in the unemployment rate.

That is also what the incoming data is showing:

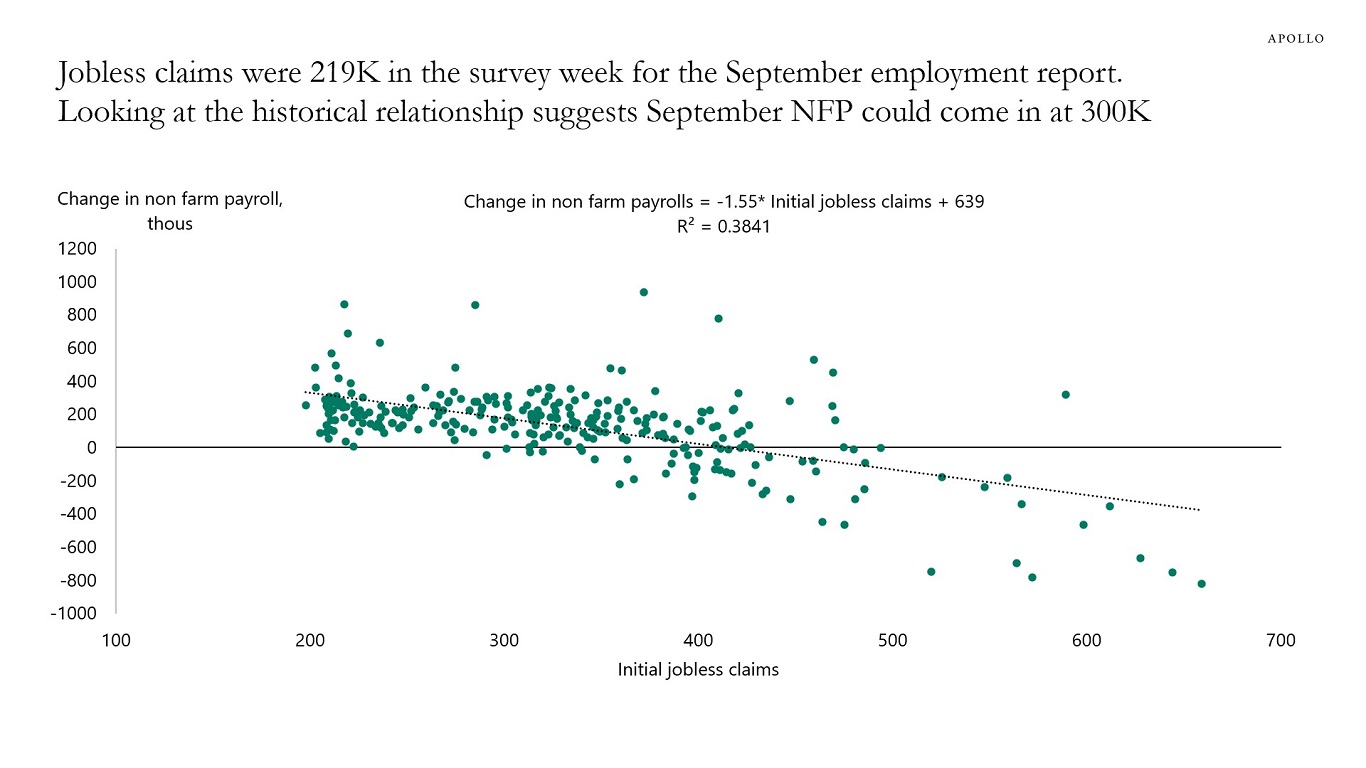

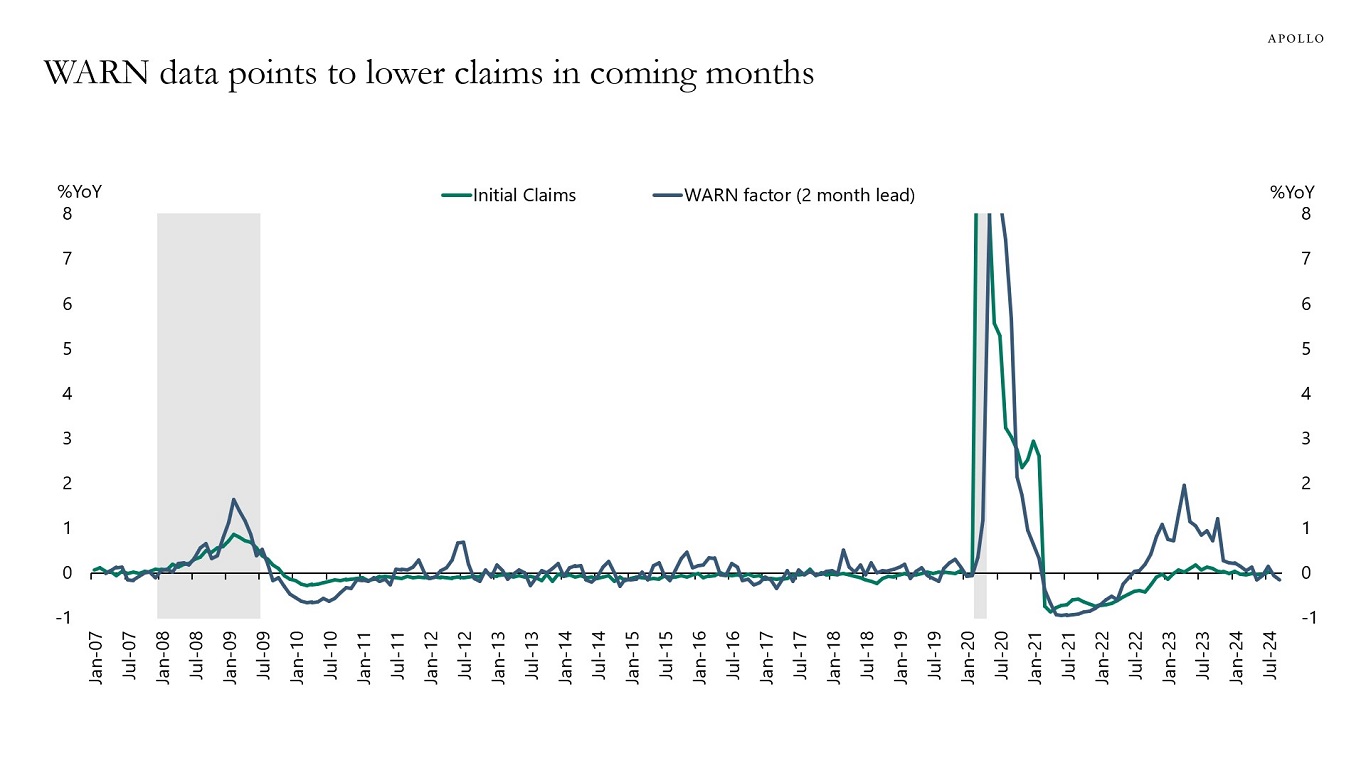

1) This week, jobless claims declined to 219,000, and given this was the survey week for the September employment report, this suggests that nonfarm payrolls for September could come in at 300,000, see the first chart below.

2) The Atlanta Fed GDP Now estimate currently stands at 2.9%, and looking at the historical relationship, this implies that nonfarm payrolls in the third quarter will come in at 240,000 jobs created each month in July, August, and September, see the second chart. In other words, we could see a sharp rebound in job growth in September from the low levels we saw in July and August.

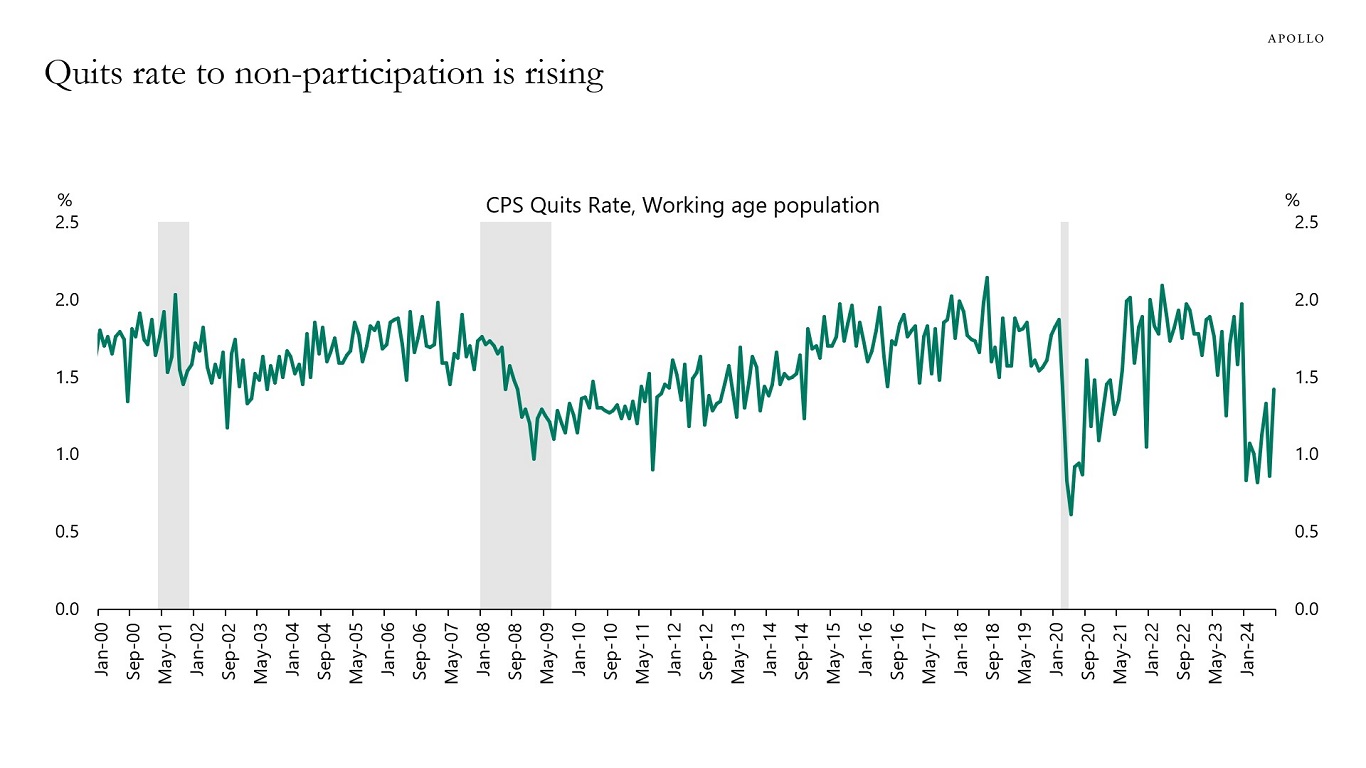

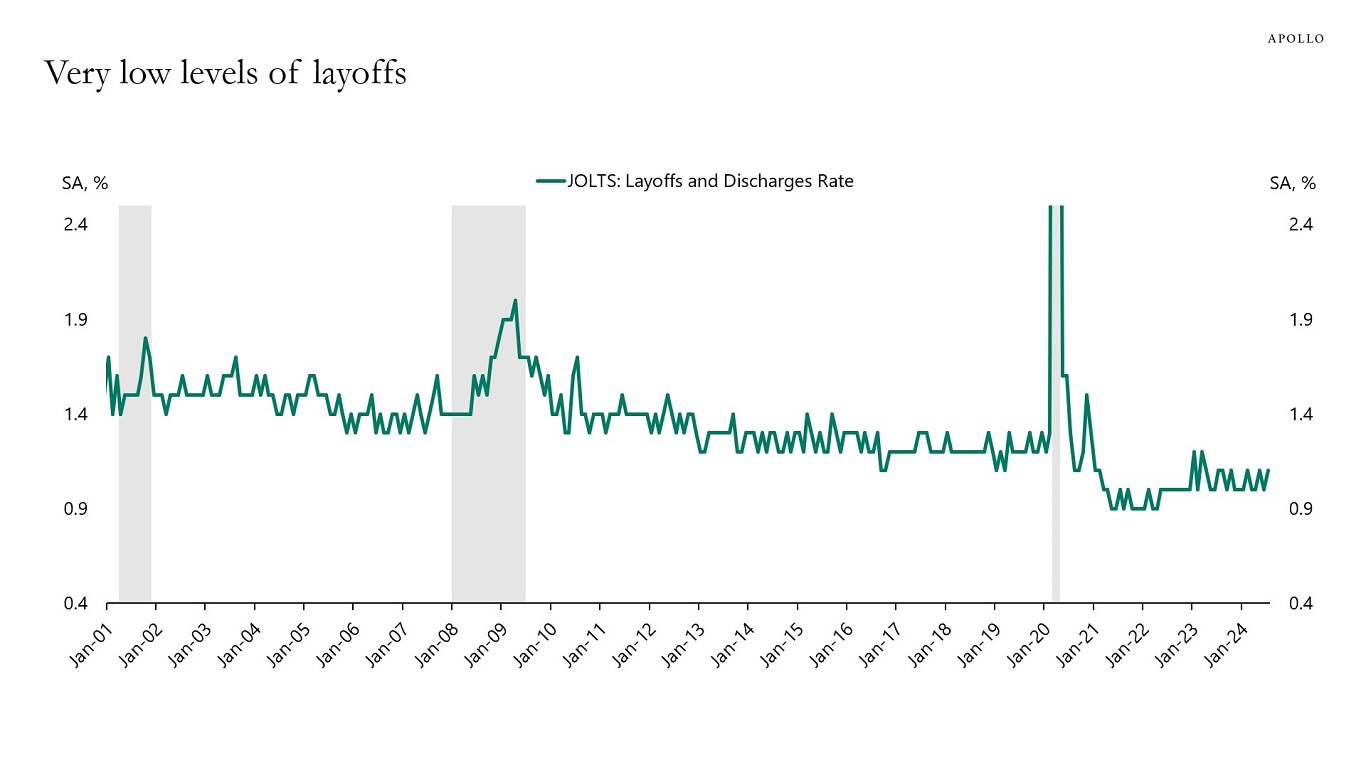

3) A new Fed paper looks at the procyclicality of quits and countercyclicality of layoffs and finds that layoffs are a leading indicator of a recession. During recessions, quits decline as layoffs increase. But this is not what the latest data for layoffs and quits to non-participation show, see the next four charts below.

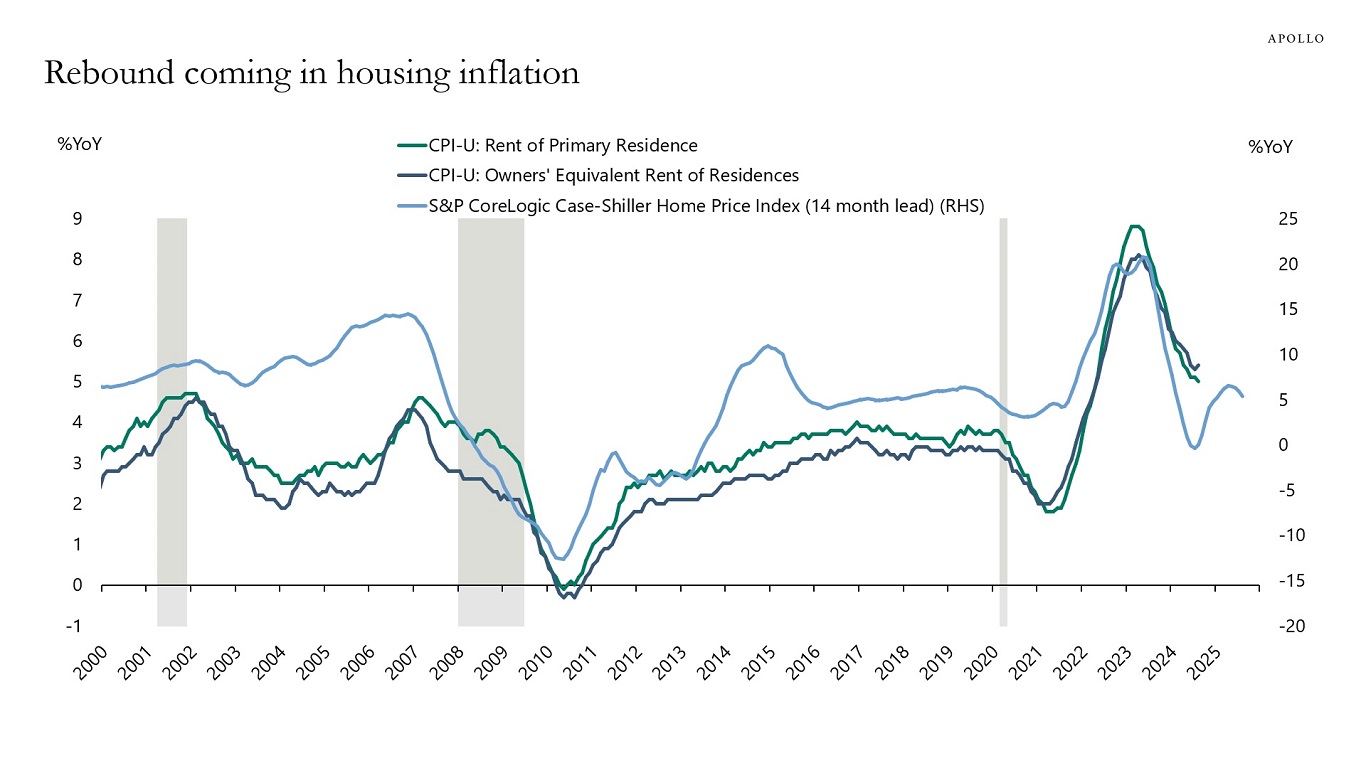

4) Finally, with mortgage rates coming down and Case-Shiller at 5% we could see a rebound in the housing market, which could trigger a rebound in overall inflation, see the last chart.

With financial conditions easing further because of the 50bps Fed cut and still strong tailwinds to economic growth from the CHIPS Act, the IRA, the Infrastructure Act, strong AI spending, and strong defense spending, the bottom line is that there are no signs of the economy entering a recession. And because of these tailwinds, there are no reasons to expect a recession. On the contrary, the incoming data seen in our chart book (available here), in particular jobless claims and the Atlanta Fed GDP Now, are pointing to a reacceleration in employment growth over the coming months.