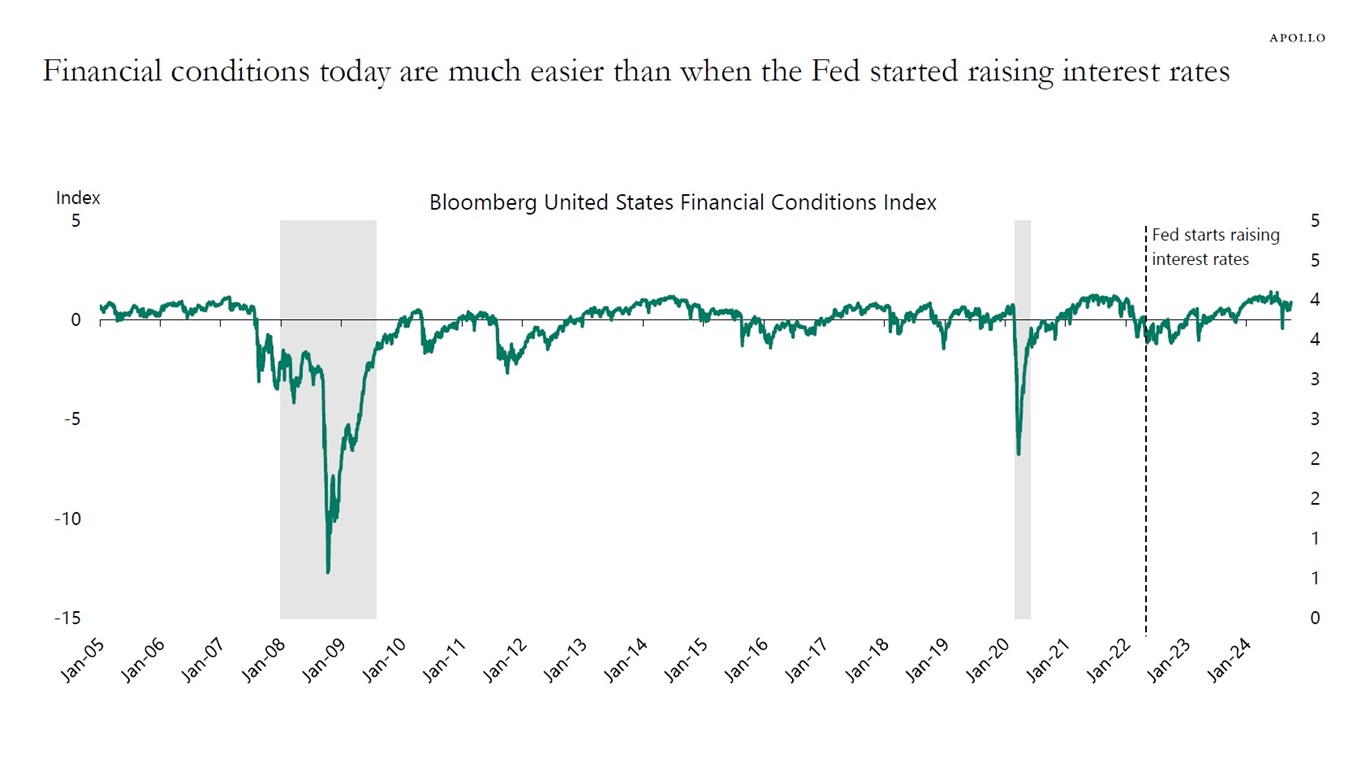

The idea that real interest rates become tighter when inflation falls and, therefore, the Fed must follow along with cuts is misguided. No household or firm borrows at the Fed funds rate. It is financial conditions that matter. With record-high stock prices and very tight credit spreads, cutting 50bps makes financial conditions even easier, see charts below.

More broadly, the source of recessions and why the economy suddenly goes from calm to chaos in a nonlinear way is because of a shock. In the 2020 recession, Covid was the shock that triggered a sudden stop in consumer spending and capex spending. In 2008, the shock was Lehman. In the 2001 recession, the shock was a 50% decline in the S&P 500 index.

But there is no exogenous shock today. Households don’t suddenly stop spending unless there is some shock hitting their income or wealth.

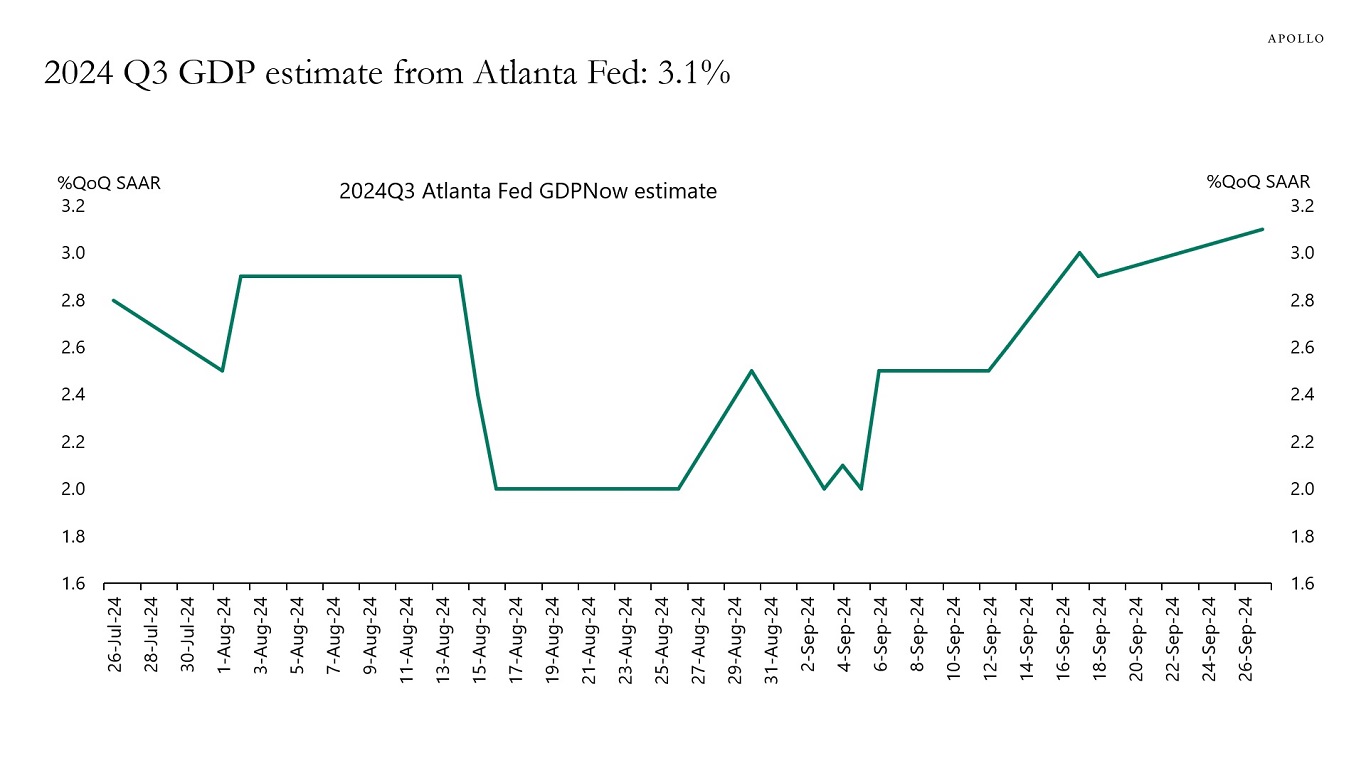

The shock during this cycle was interest rates going up since March 2022, and that didn’t generate a recession. Now, interest rates are going down, and financial conditions are easing rapidly. Inflation is currently close to 2%, and growth is strong, and the Atlanta Fed GDP estimate for the third quarter stands at 3.1%.

Summing up, current economic conditions can be best described as “goldilocks.” Not too hot, and not too cold. But the story doesn’t end here. The risk with cutting interest rates too much too quickly is that the economy becomes too hot again.

See our chart book with daily and weekly indicators.

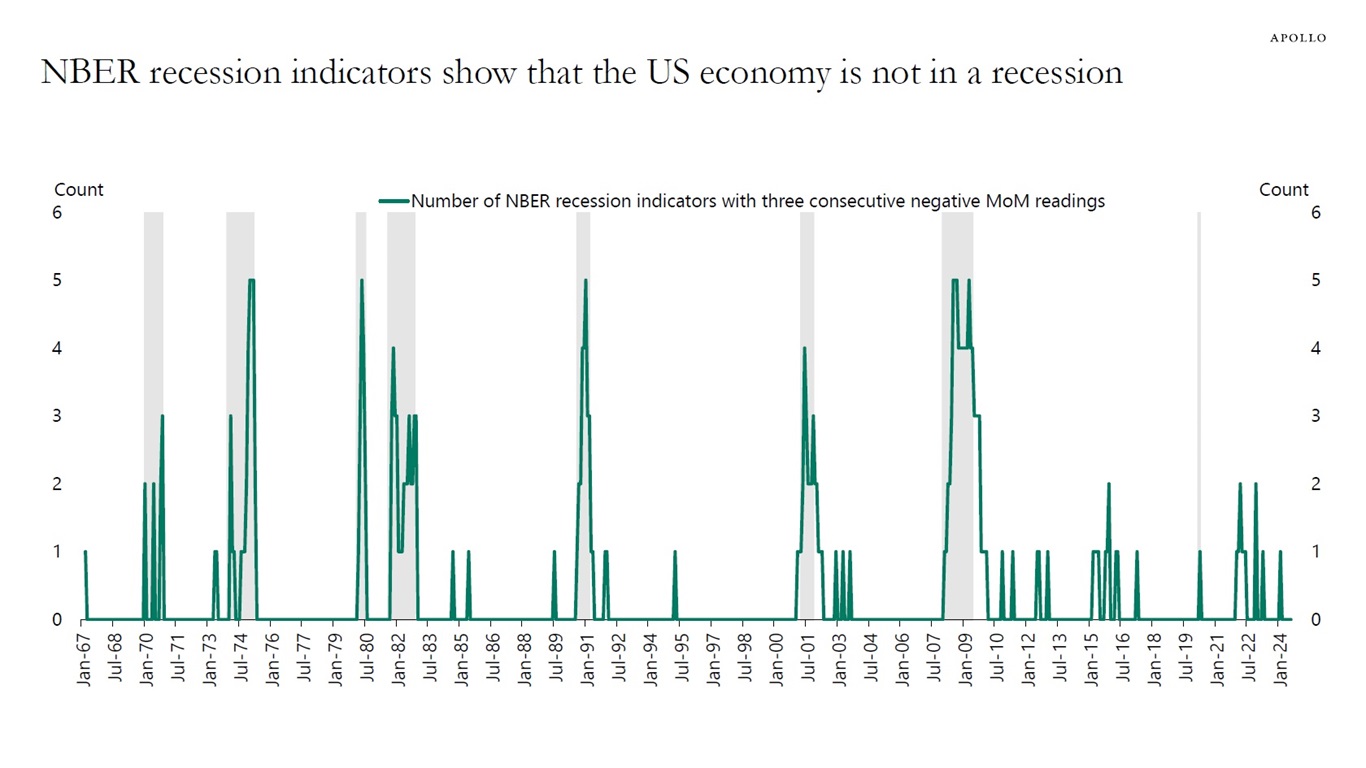

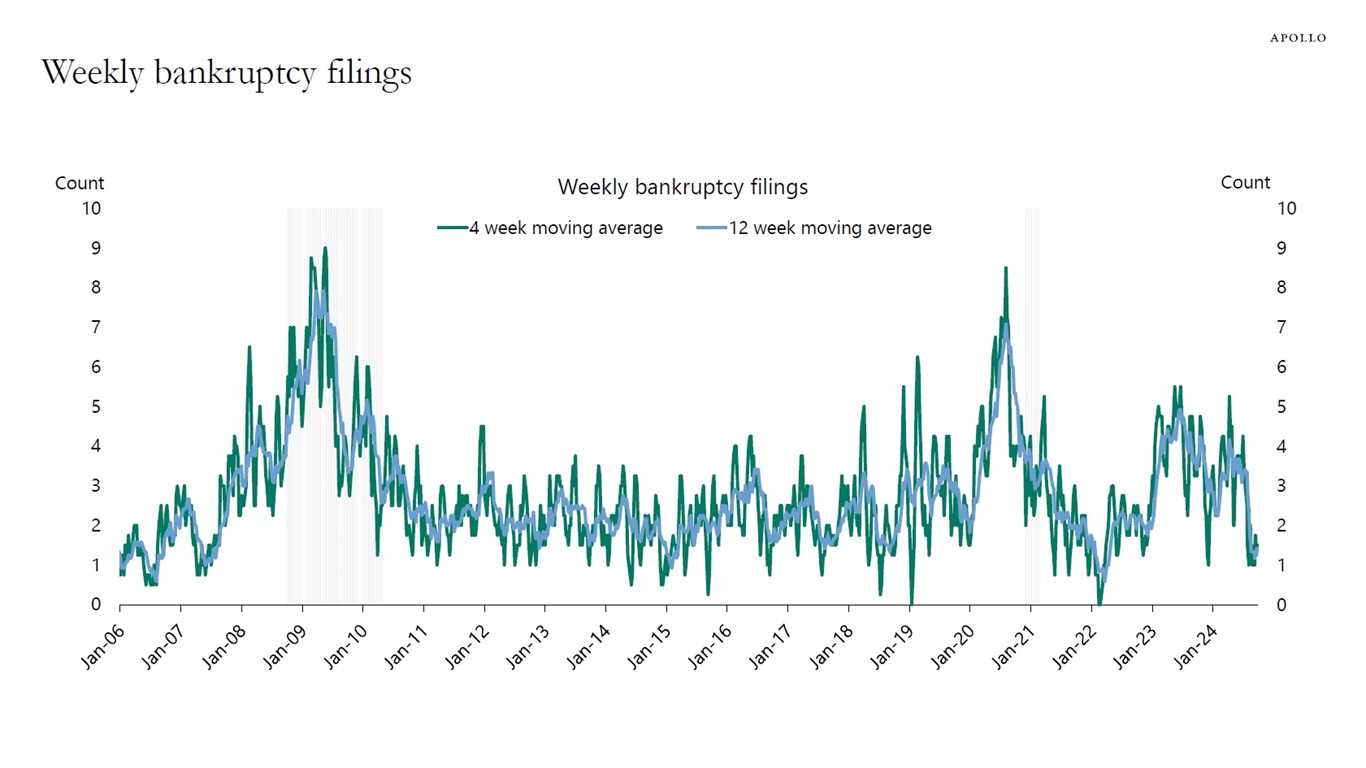

Source: Bloomberg, Apollo Chief EconomistNote: NBER recession indicators include Real Manufacturing & Trade Sales, Industrial Production Index, Real Personal Income less Transfer Payments, Real Personal Consumption Expenditures, Nonfarm payrolls, and Household survey employment. Source: BEA, FRB, BLS, NBER, Haver Analytics, Apollo Chief EconomistSource: Federal Reserve Bank of Atlanta, Haver Analytics Apollo Chief EconomistNote: Filings are for companies with more than $50mn in liabilities. For week ending on September 28, 2024. Source: Bloomberg, Apollo Chief Economist

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.