The narrative that the labor market is cooling is inconsistent with the continued strength seen in the incoming data for above-trend GDP growth, strong retail sales, strong durable goods, low jobless claims, and rising average hourly earnings.

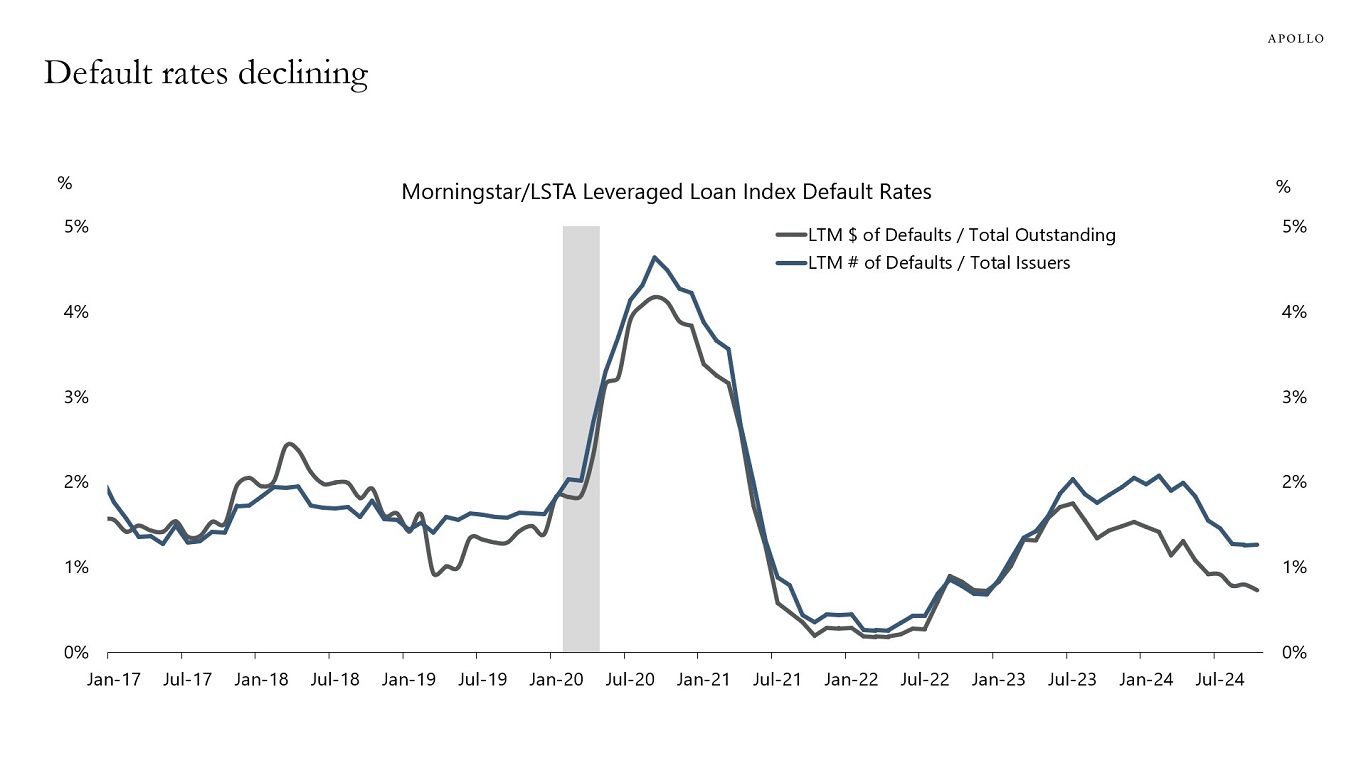

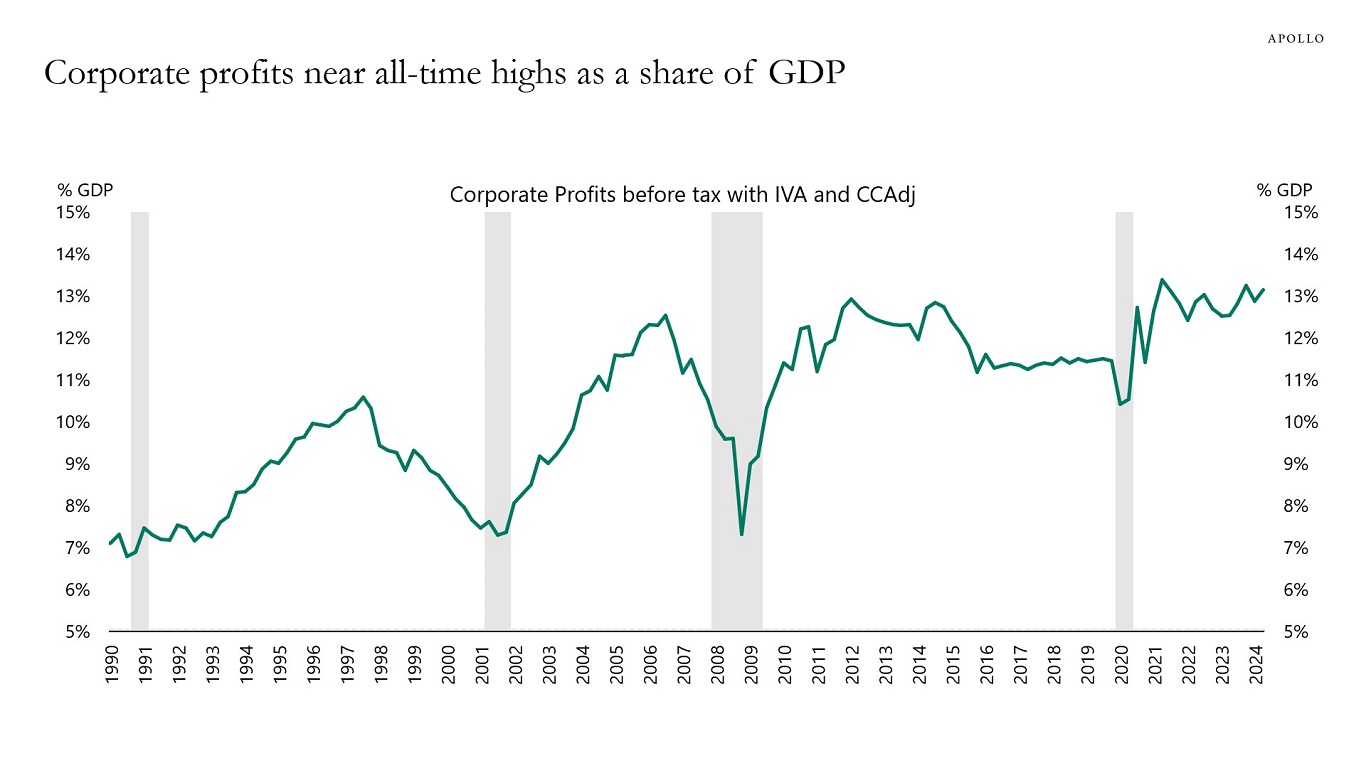

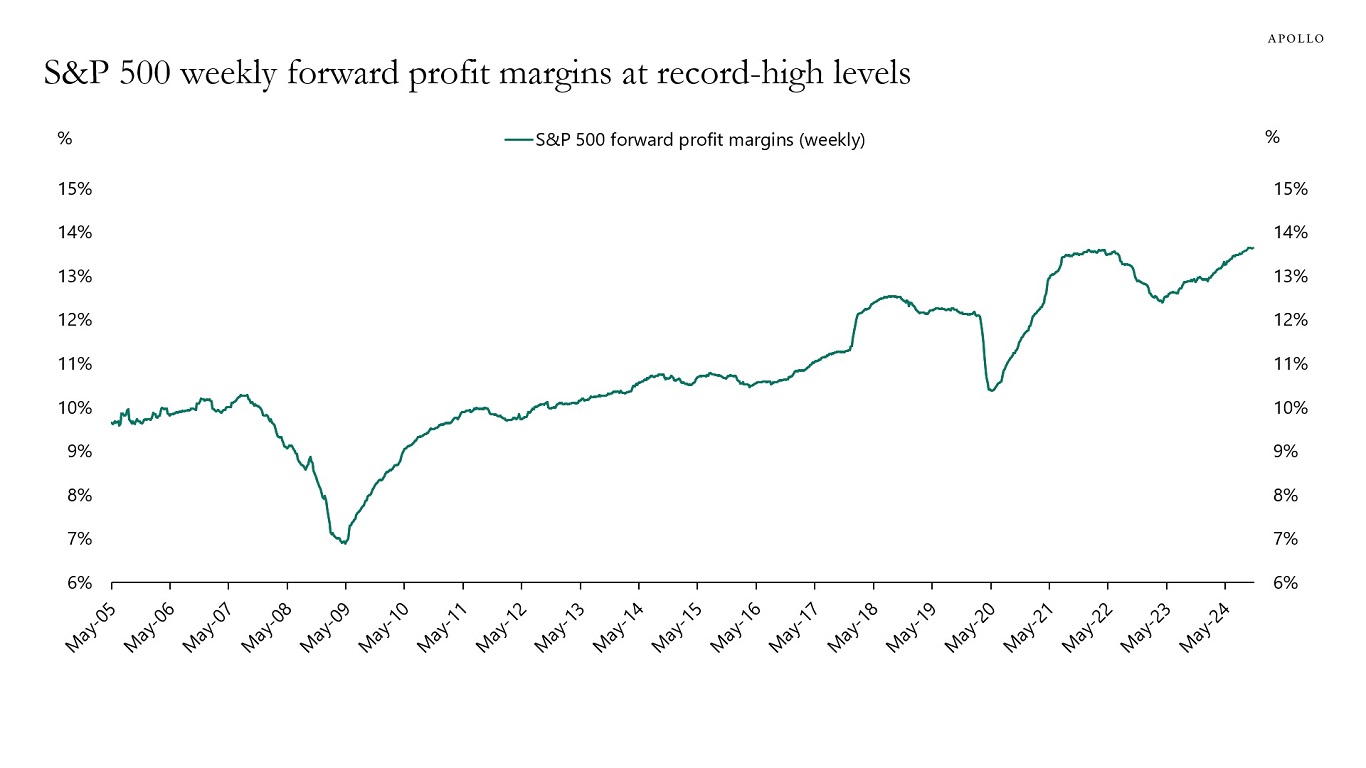

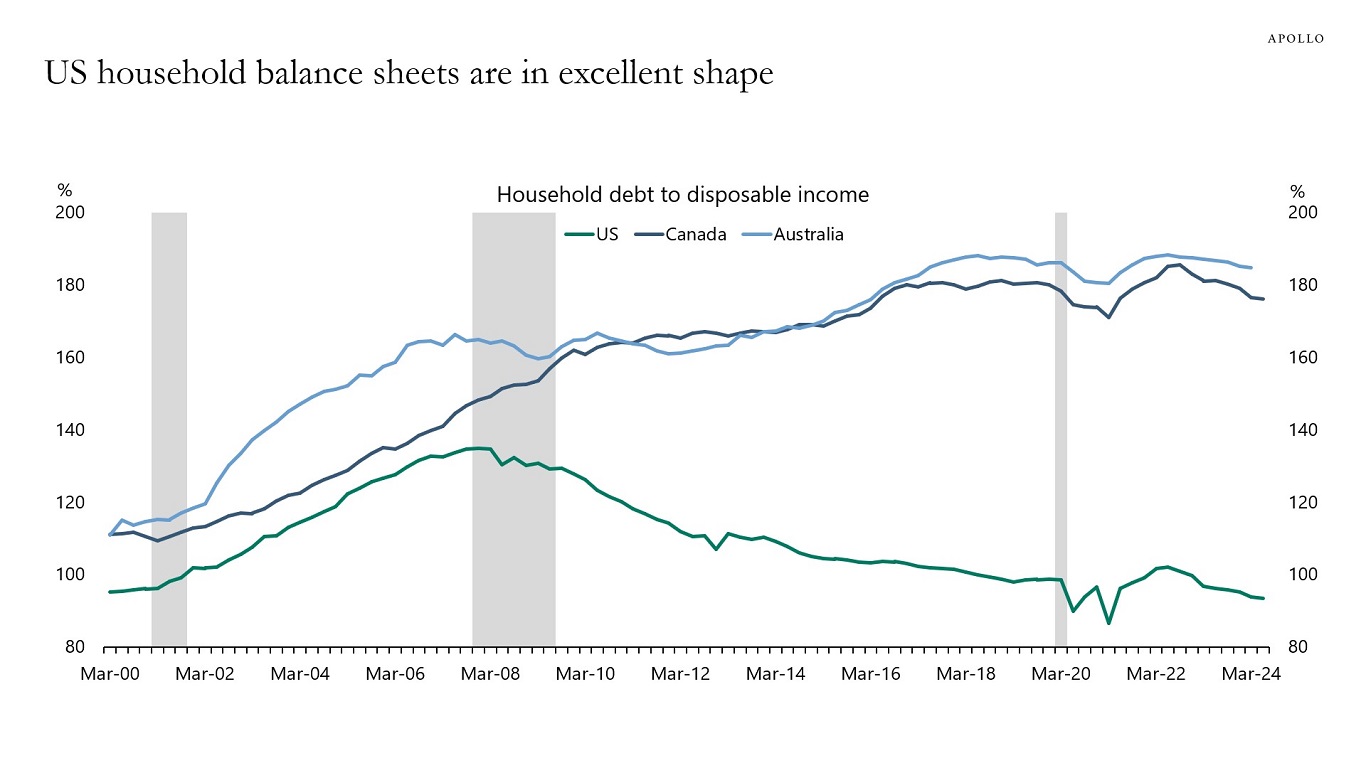

In addition, default rates continue to decline, corporate profits are at all-time highs, weekly forward profit margins are at record highs, and US household balance sheets are in excellent shape, see charts below.

In short, the US economy remains incredibly strong.

Combined with tailwinds to growth from record-high stock prices, tight credit spreads, M&A/issuance markets rebounding, the AI/data center boom, the Chips Act, the IRA, the Infrastructure Act, and lower taxes for domestic manufacturers and deregulation likely coming, the bottom line is that we could see a dramatic increase in job growth in November, including a reversal of the weather and strike effects that were pushing down nonfarm payrolls in October.

Our chart book with daily and weekly indicators for the US economy is available here.

Source: PitchBook LCD, Apollo Chief EconomistSource: BEA, Haver Analytics, Apollo Chief EconomistNote: The 12-month forward profit margins are calculated by using the weighted average of 1FY (current year estimate) and 2FY (next year estimate) to smooth out fiscal year transitions. Source: Bloomberg, Apollo Chief EconomistSource: Statistics Canada, Reserve Bank of Australia, Bloomberg, Apollo Chief Economist

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.