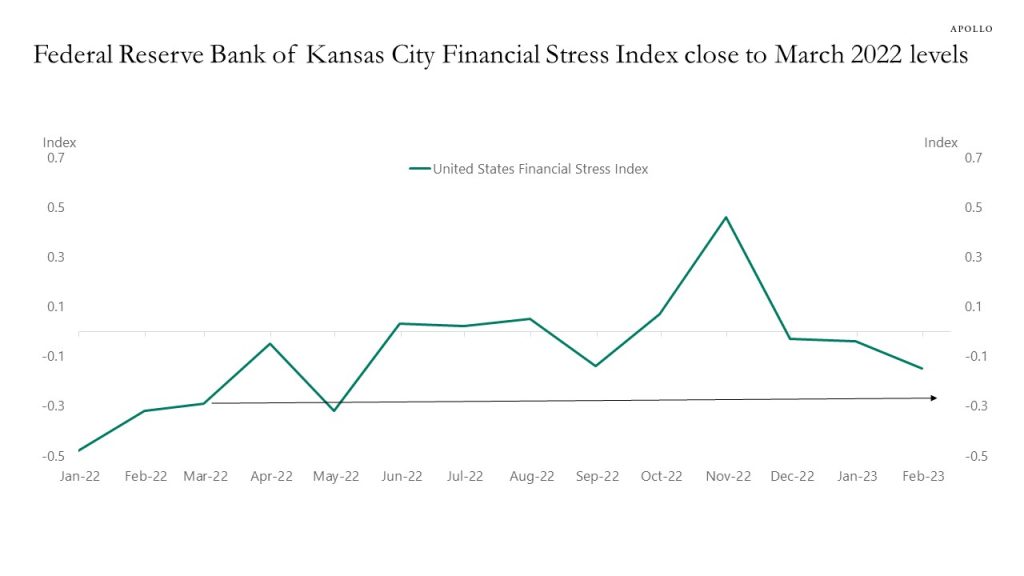

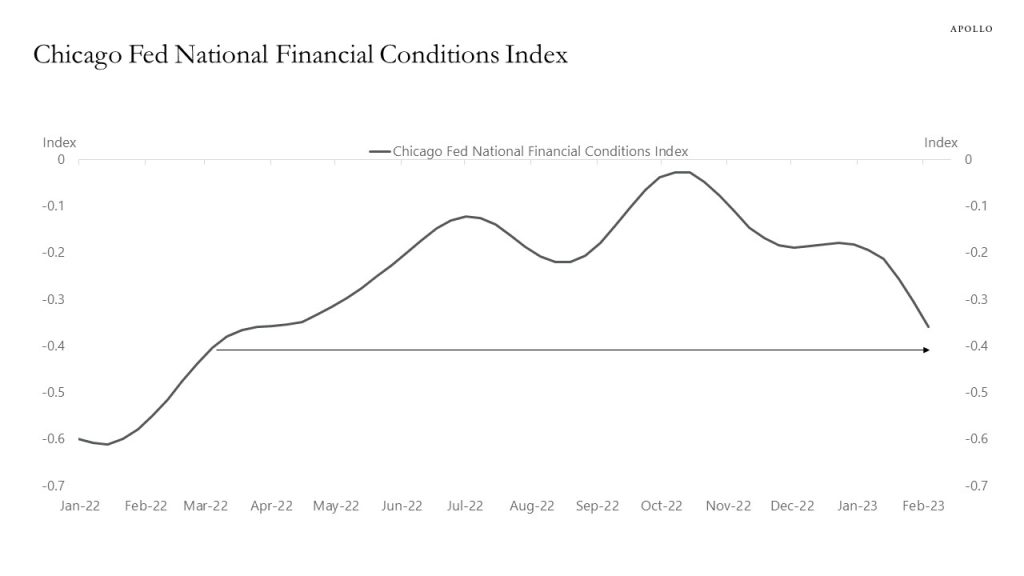

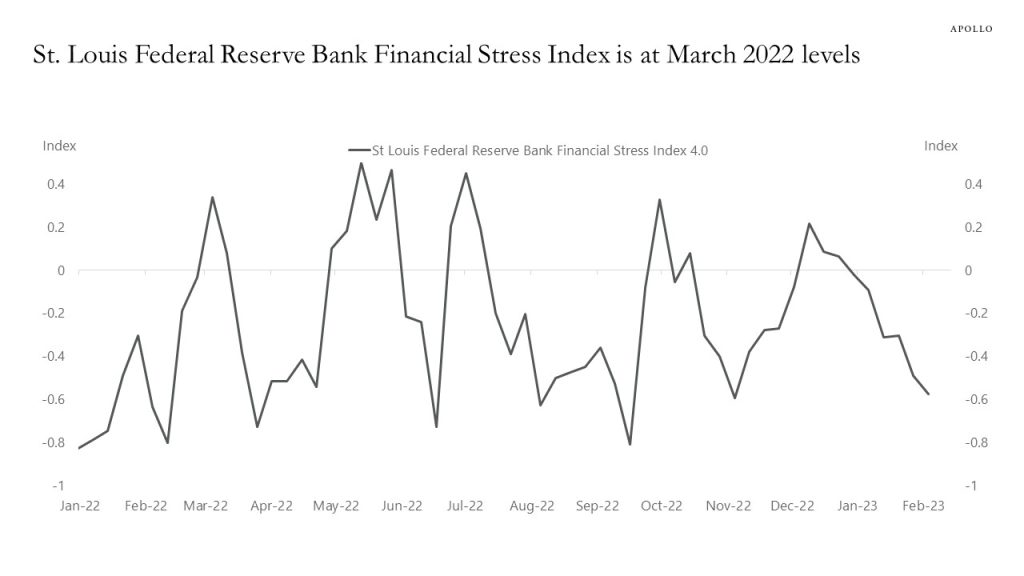

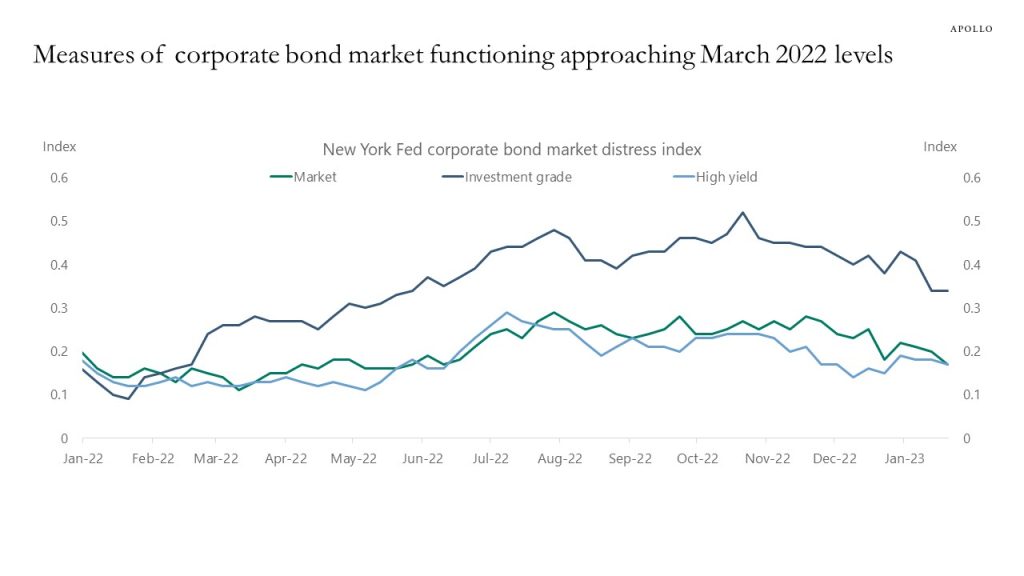

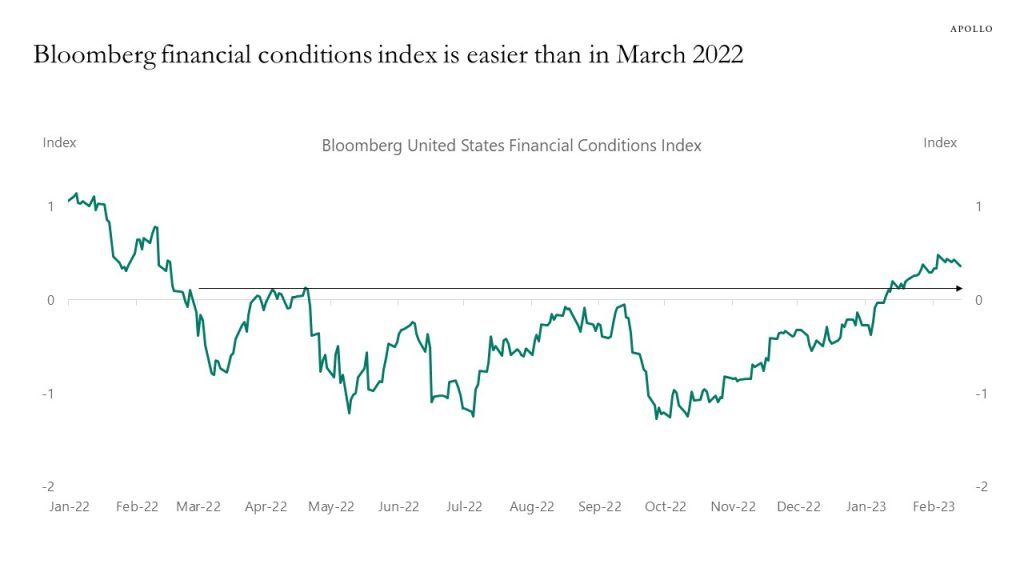

Fed measures of financial conditions show that Fed hikes since March 2022 have been offset by a rising S&P500, tighter IG spreads, and tighter HY spreads, and overall financial conditions are now as easy as they were before the Fed started raising interest rates, see charts below.

With inflation still in the 4% to 6% range, the risks are rising that easy financial conditions will boost consumer spending, capex spending, and ultimately inflation. In other words, it looks like more Fed hikes are needed to get inflation all the way back to the Fed’s 2% inflation target.

Source: Federal Reserve bank of Kansas City, Bloomberg, Apollo Chief Economist. Note: A positive value indicates that financial stress is above the long-run average, while a negative value signifies that financial stress is below the long-run average. Variables included are Treasury REPO Spread (spread between GCF REPO rate and three-month Treasury bill rate), Two-year swap spread (spread between two-year US interest rate swap rate and two-year Treasury yield), Spread between off-the-run 10-year Treasury yield and on-the-run 10-year constant maturity Treasury yield, Spread between Aaa corporate bond yield and 10-year constant maturity Treasury yield, Spread between Baa and Aaa corporate bond yields, Spread between High-yield Bond and Baa spread, Spread between fixed-rate credit card ABS yield and five-year constant maturity Treasury yield, Negative value or correlation between total return on S&P500 and total return on two-year Treasury bonds, Implied volatility of overall stock prices, Idiosyncratic volatility of bank stock prices, Cross-sectional dispersion of bank stock returns.Source: Federal Reserve bank of Chicago, Bloomberg, Apollo Chief Economist. Note: The NFCI provides a comprehensive weekly update on US financial conditions in money markets, debt and equity markets, and the traditional and “shadow” banking systems. The National Financial Conditions Index (NFCI) is a weighted average of a large number of variables (105 measures of financial activity) each expressed relative to their sample averages and scaled by their sample standard deviations.Source: Federal Reserve bank of St. Louis, Bloomberg, Apollo Chief Economist. Note: The index measures the degree of financial stress in the markets and is constructed from 18 weekly data series: seven interest rate series, six yield spreads and five other indicators. Each of these variables captures some aspect of financial stress.Source: FRB of New York, Apollo Chief Economist (Note: Corporate bonds are a key source of funding for US non-financial corporations and a key investment security for insurance companies, pension funds, and mutual funds). Distress in the corporate bond market can thus both impair access to credit for corporate borrowers and reduce investment opportunities for key financial sub-sectors. CMDI offers a single measure to quantify joint dislocations in the primary and secondary corporate bond markets. Ranging from 0 to 1, a higher level of CMDI corresponds with historically extreme levels of dislocation. CMDI links bond market functioning to future economic activity through a new measure.Source: Bloomberg, Apollo Chief Economist. Note: The Bloomberg Financial Conditions Index includes Ted Spread, Commercial Paper/T-Bill Spread, Libor-OIS Spread, Baa Corporate/Treasury Spread, Muni/Treasury Spread, High Yield/Treasury Spread, Swaption Volatility Index, S&P500 Share Prices, VIX Index.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.