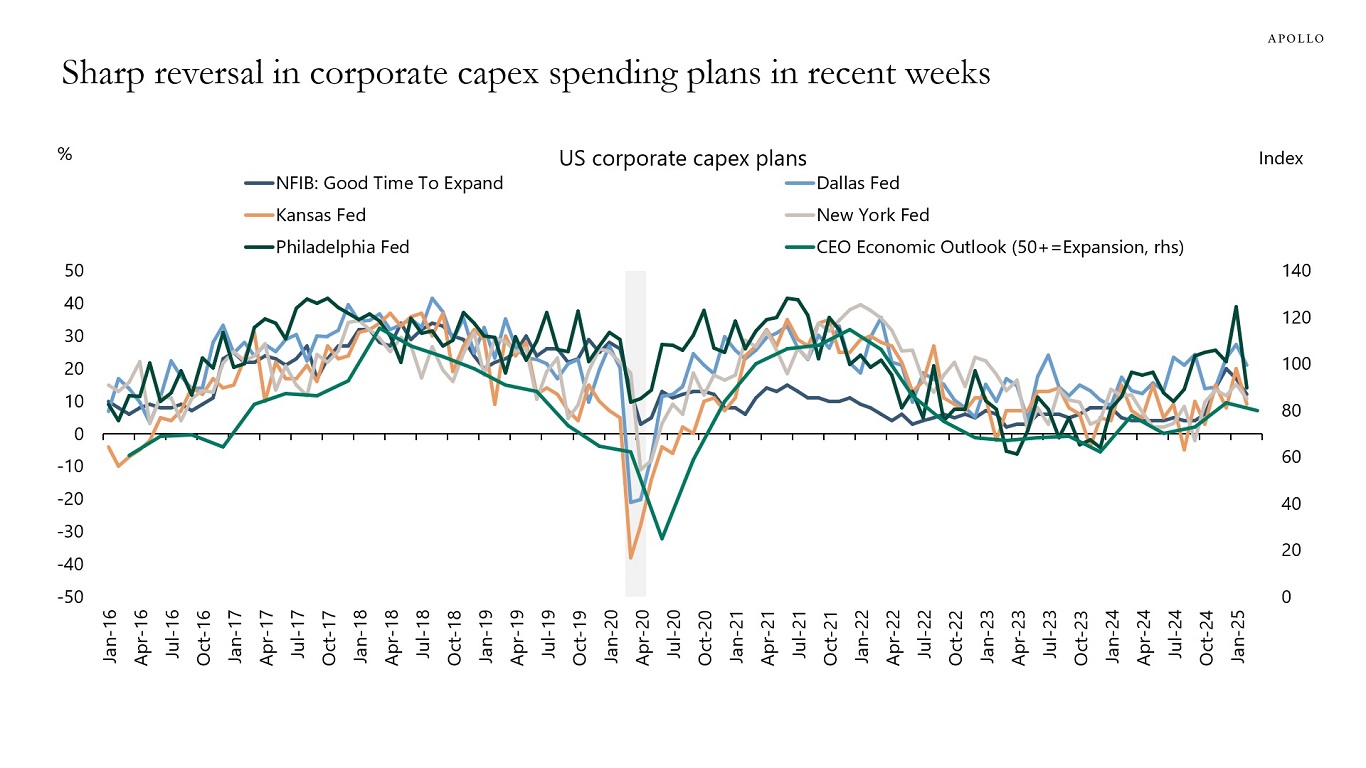

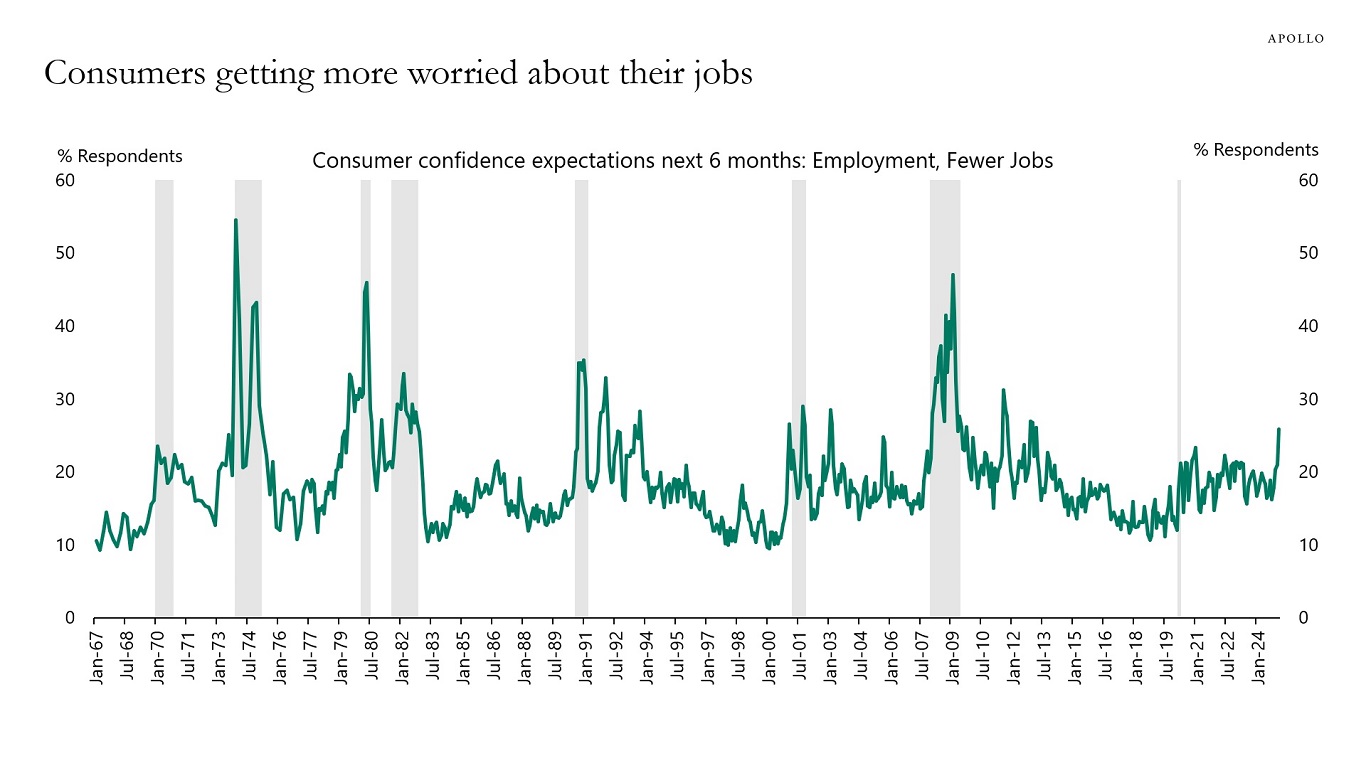

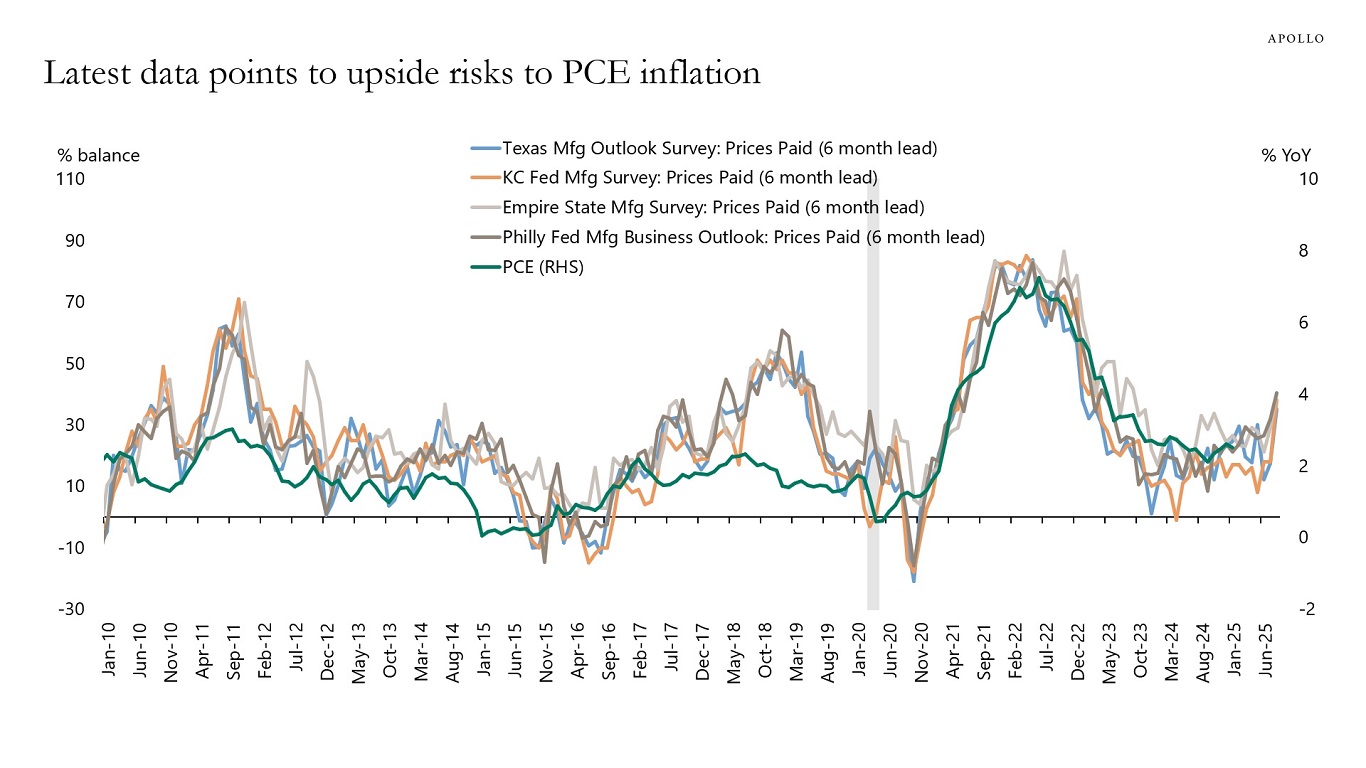

Surveys of firms show that companies have in recent weeks started to pull back capex plans, and consumers are getting more worried about their jobs, see the first two charts below. At the same time, leading indicators point to higher inflation ahead, see the third chart.

Furthermore, airlines this week reported a slowdown in bookings, and the latest credit card data points to broad-based weakness across all categories except online sales.

The bottom line is that the soft data points to weakness coming in the hard data.In addition, this past week was the survey week for the March employment report, and with uncertainty elevated, the downside risks to March nonfarm payrolls—when it is released on Friday, April 4—are significant.

Our updated chart book with daily and weekly indicators for the US economy is available here.

Sources: Apollo Chief Economist, Business Roundtable, NFIB, Federal Reserve Banks of Dallas, Kansas, New York, Philadelphia, and RichmondSources: Apollo Chief Economist, Conference Board, Haver AnalyticsSources: Apollo Chief Economist, BEA, FRBNY, Haver Analytics, Federal Reserve Banks of Dallas, Kansas City, New York, Philadelphia, and Richmond

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.