Want it delivered daily to your inbox?

-

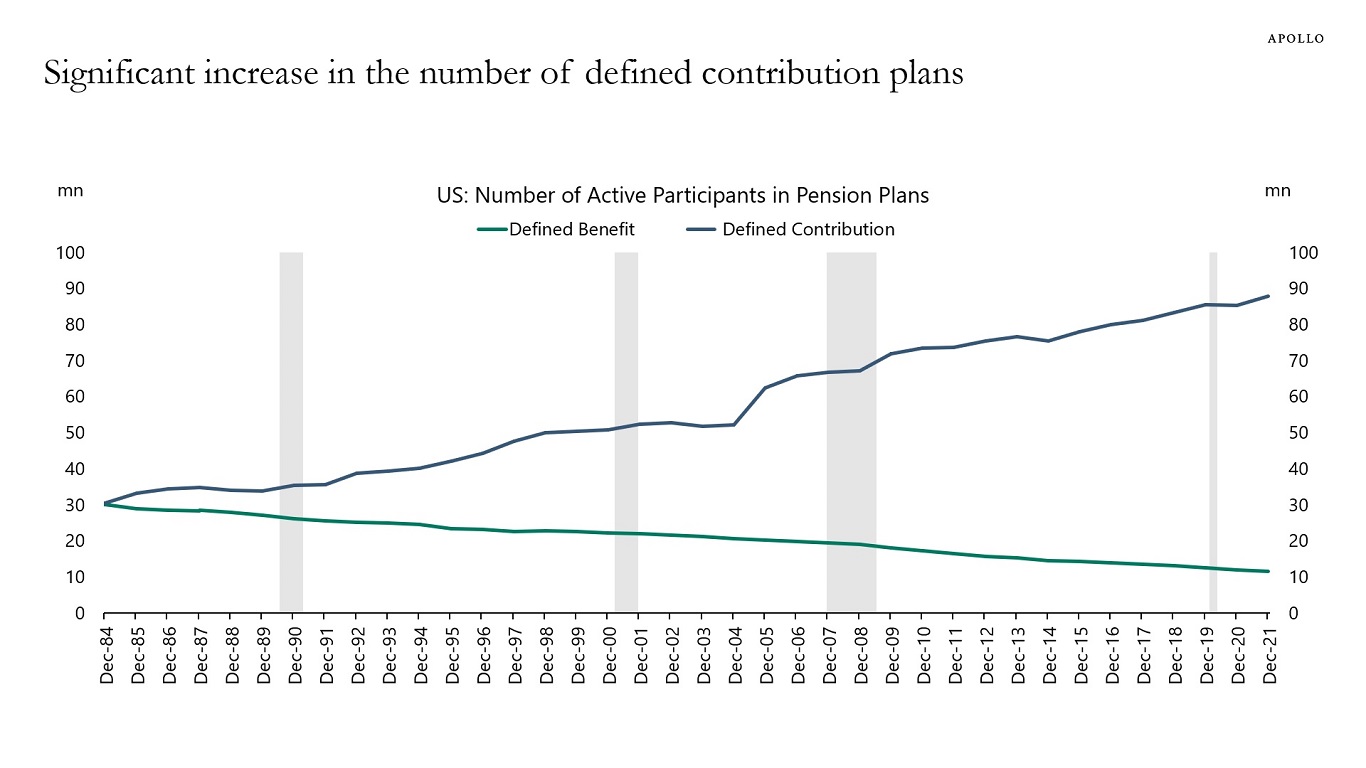

There are 10 million participants in defined benefit plans and 90 million in defined contribution plans such as the 401(k), see chart below.

Source: Department of Labor, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

Many FOMC members argue that the Fed funds rate at 5.5% is very restrictive because the Fed’s r-star model says that neutral monetary policy would mean a Fed funds rate at 3%.

But maybe this r-star estimate of the terminal Fed funds rate is wrong. At least that is what the incoming data suggests.

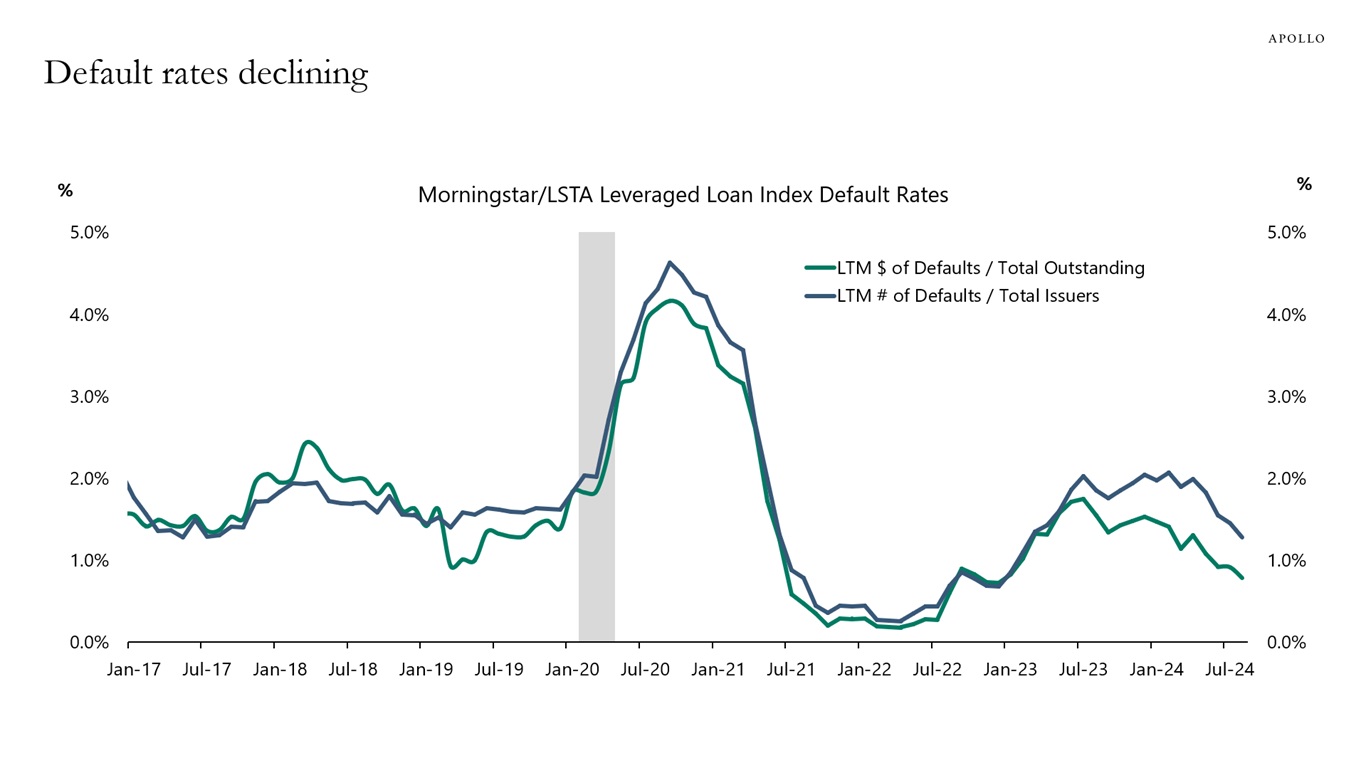

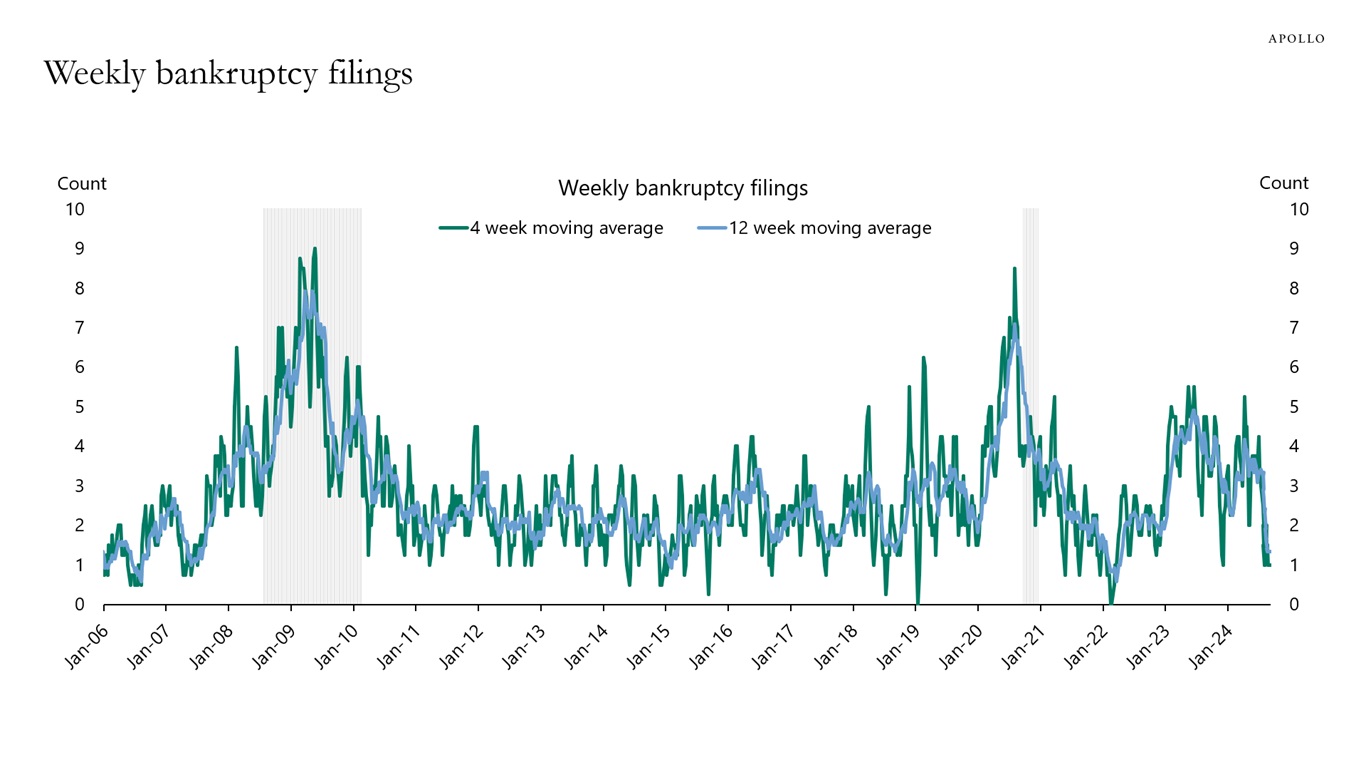

If monetary policy is very restrictive, why are default rates going down, see the first chart?

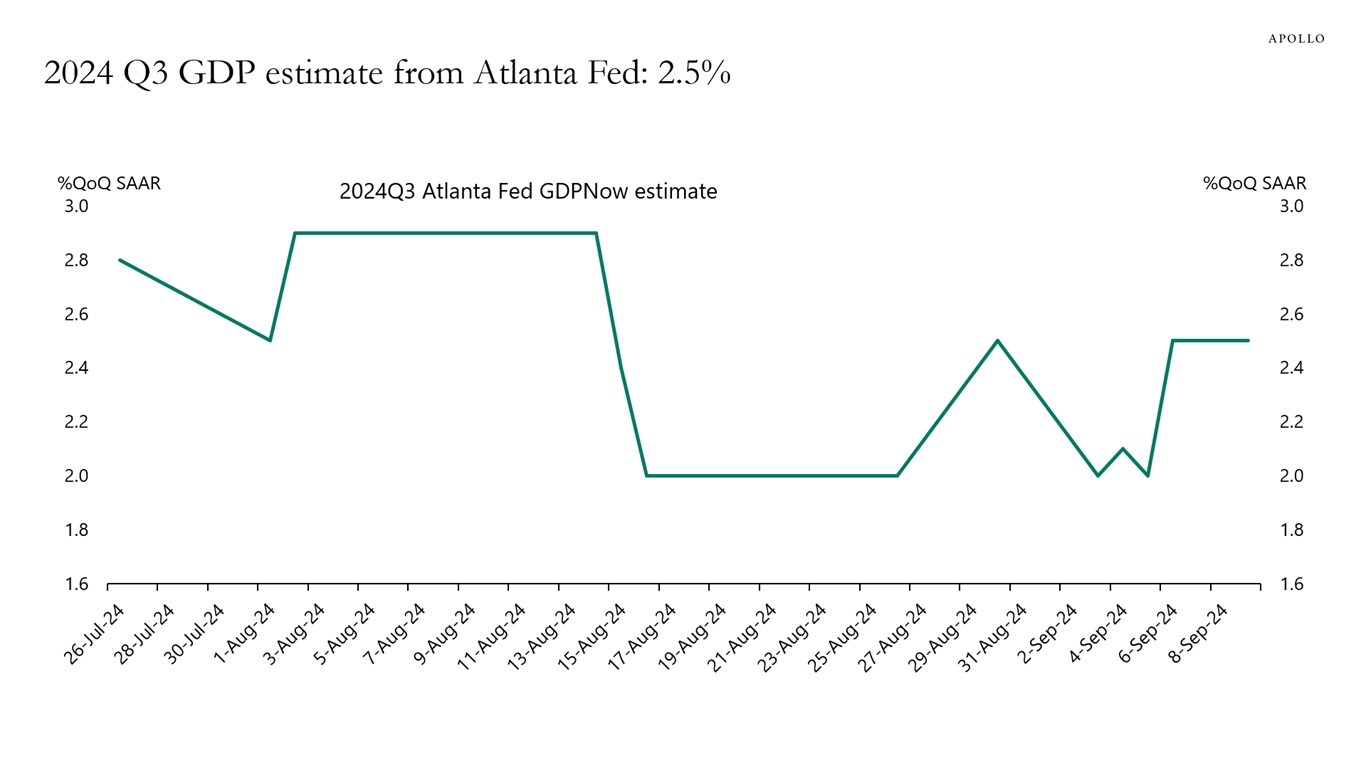

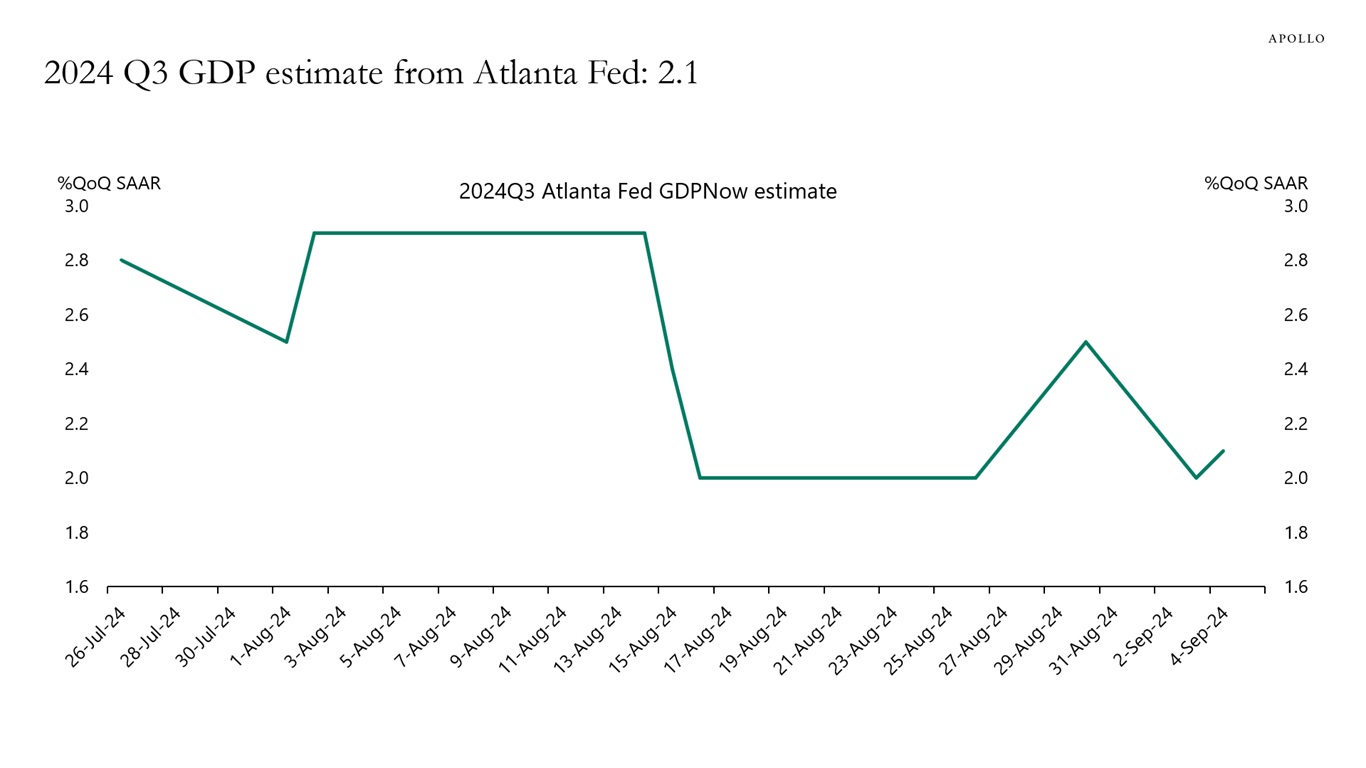

If monetary policy is very restrictive, why is the Atlanta Fed GDP Now estimate for third quarter GDP at 2.5%, well above the CBO’s estimate of long-run growth at 2%, see the second chart?

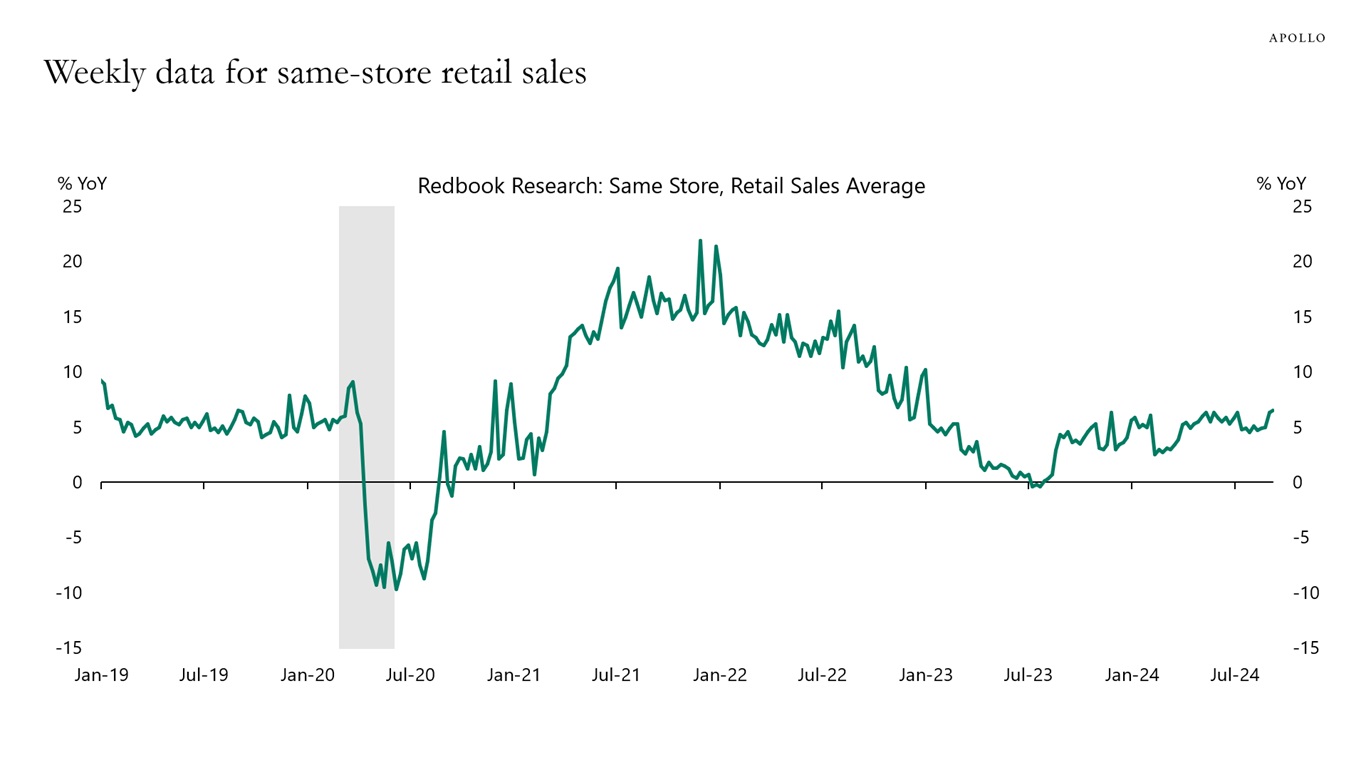

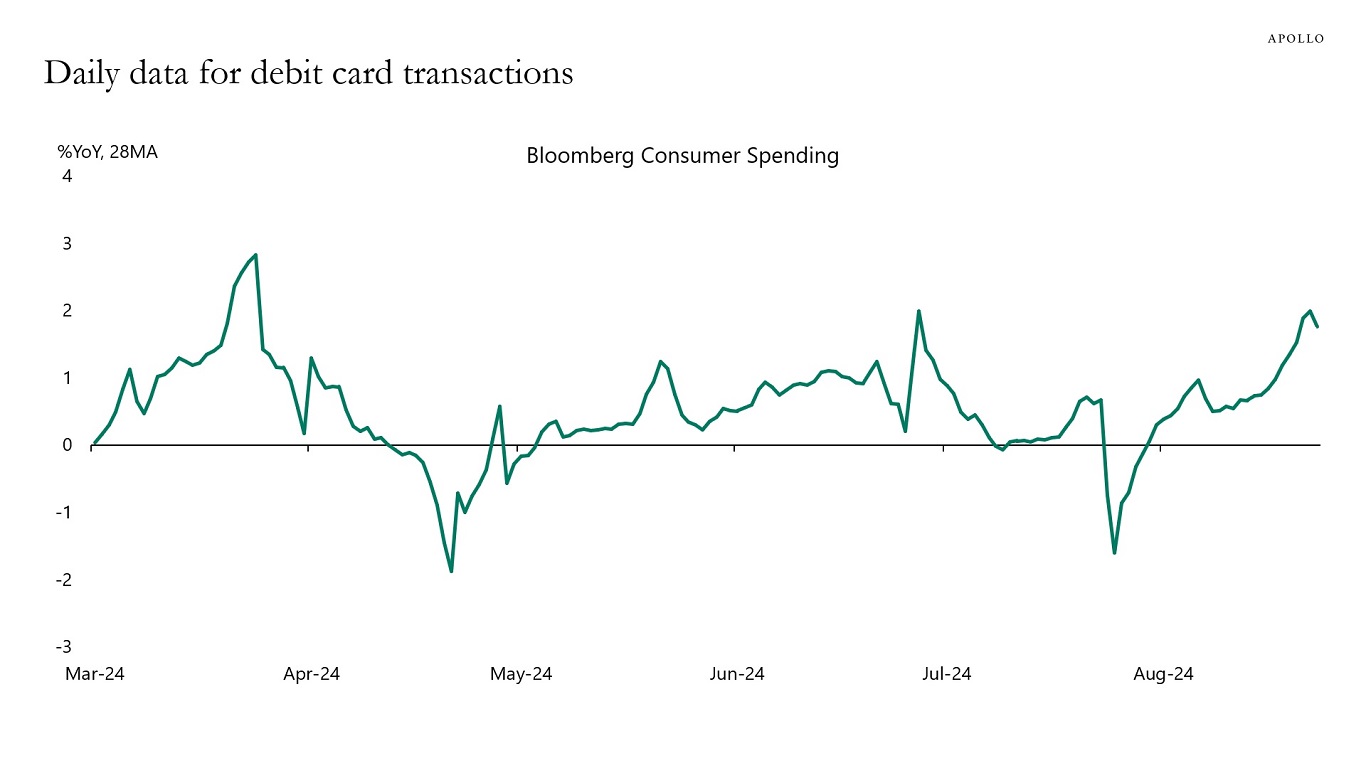

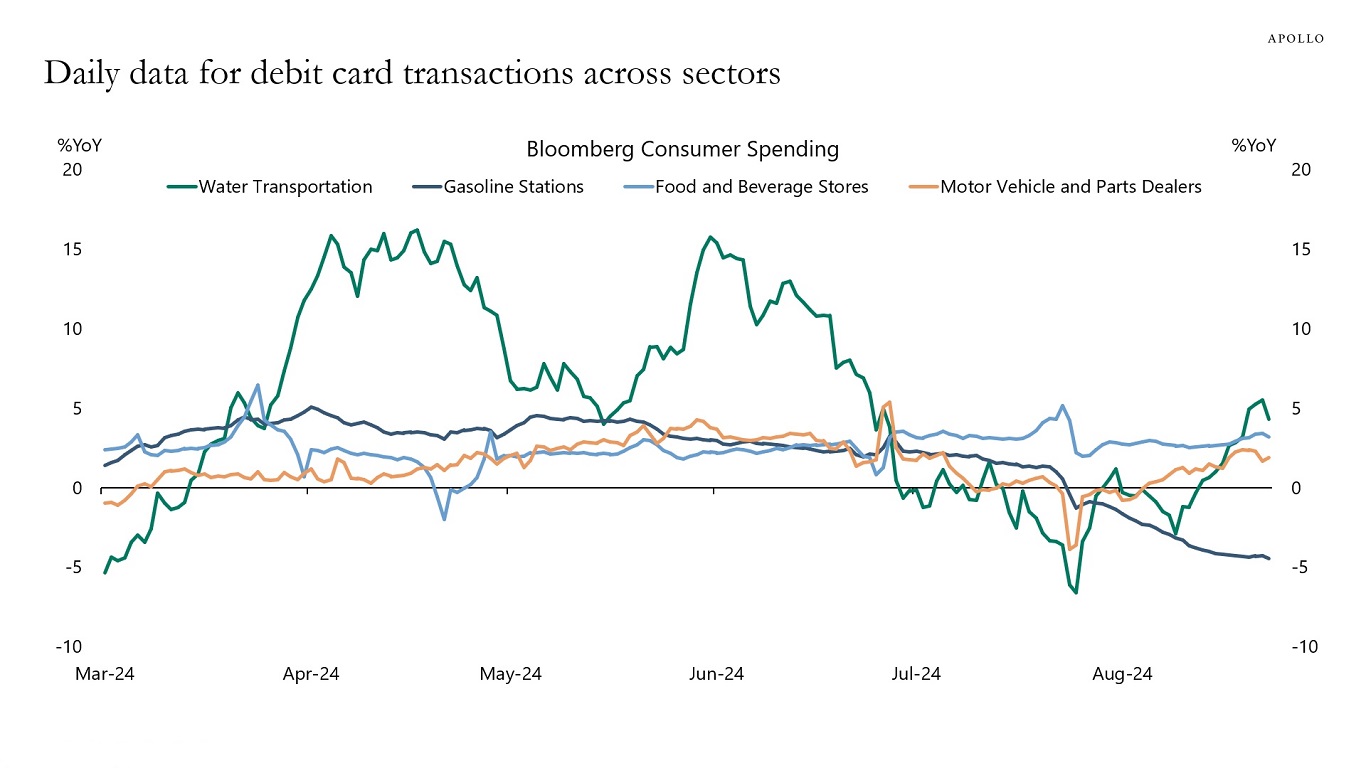

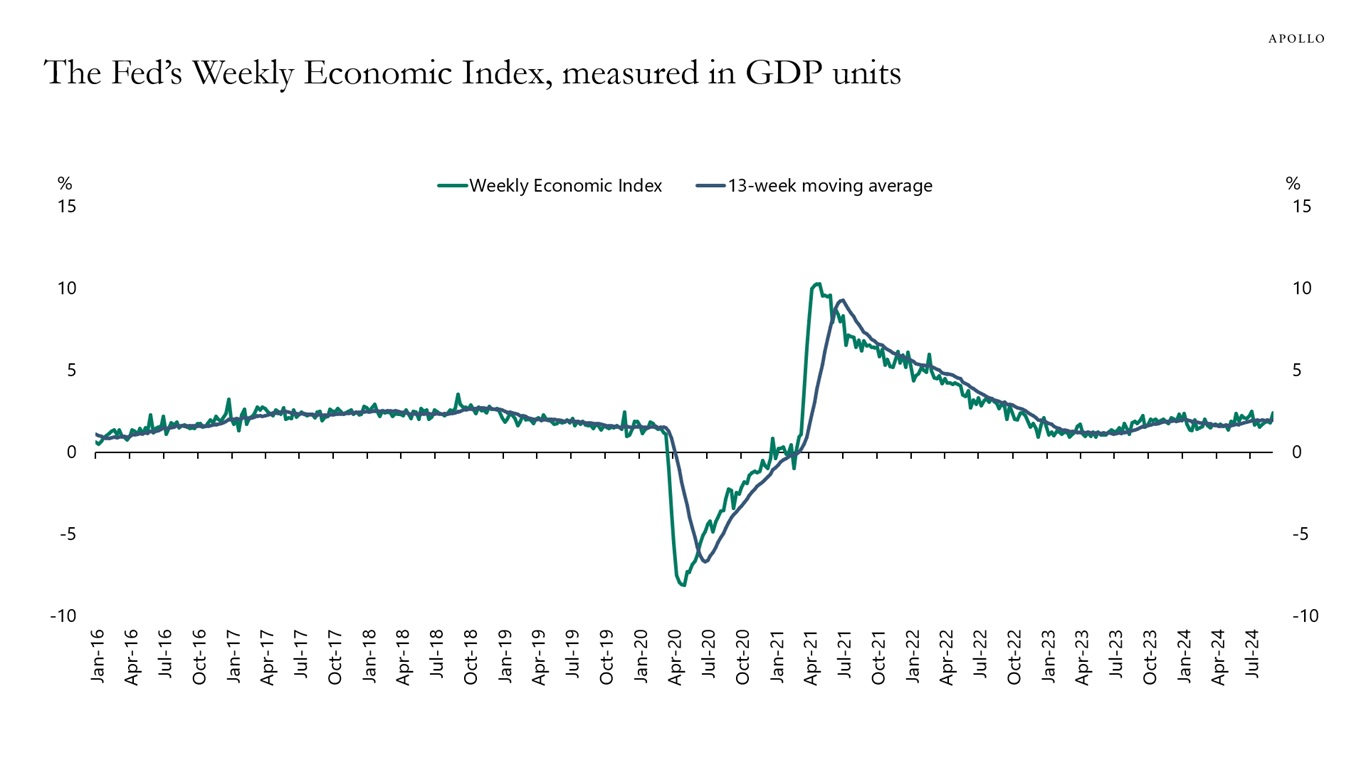

If monetary policy is very restrictive, why is weekly data for consumer spending still strong, see the third chart?

The bottom line is that the Fed funds rate at 5.5% does not seem very restrictive.

Our latest chart book with daily and weekly indicators is available here.

Source: PitchBook LCD, Apollo Chief Economist

Source: Federal Reserve Bank of Atlanta, Haver Analytics, Apollo Chief Economist

Source: Redbook, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

Foreign demand for US credit is near all-time highs, see chart below.

Source: US Treasury, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

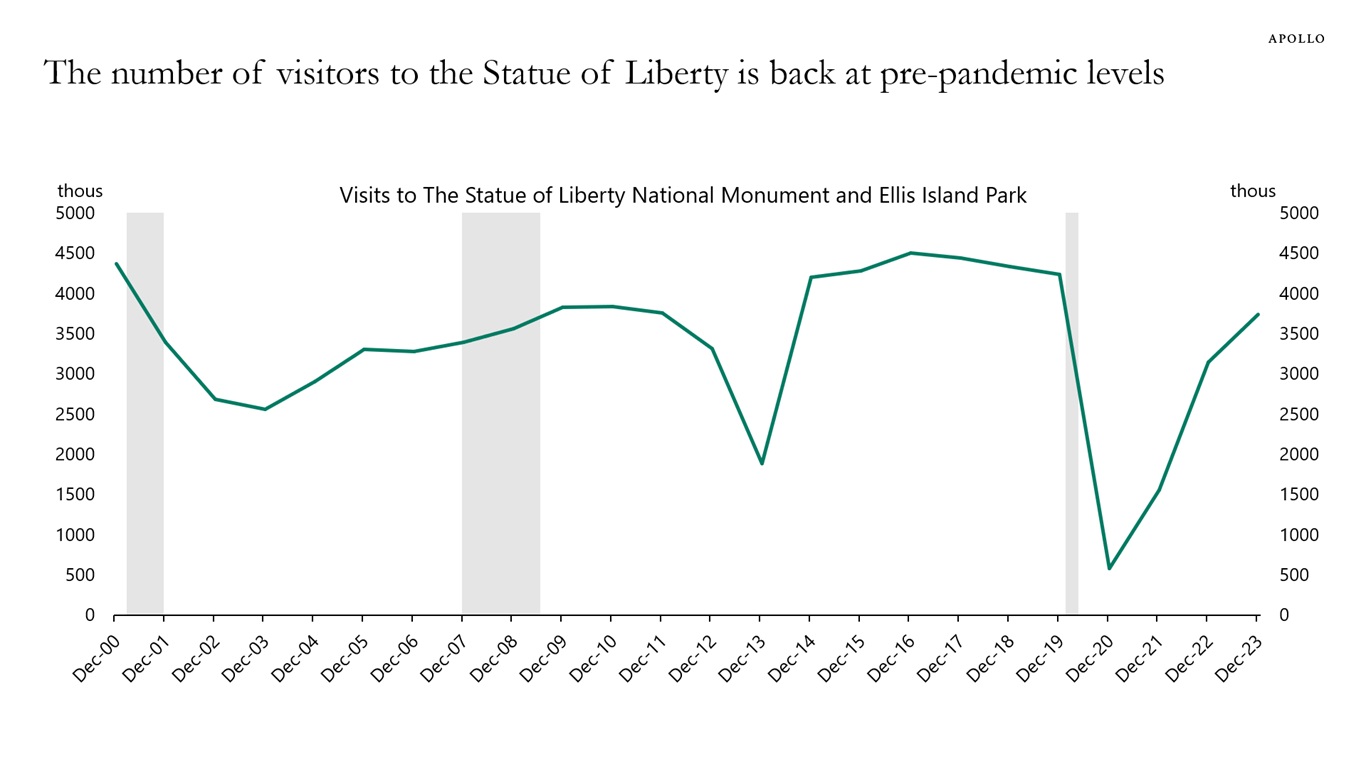

Visits to the Statue of Liberty and Ellis Island are back at pre-pandemic levels, see chart below and here.

Source: National Park Service, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

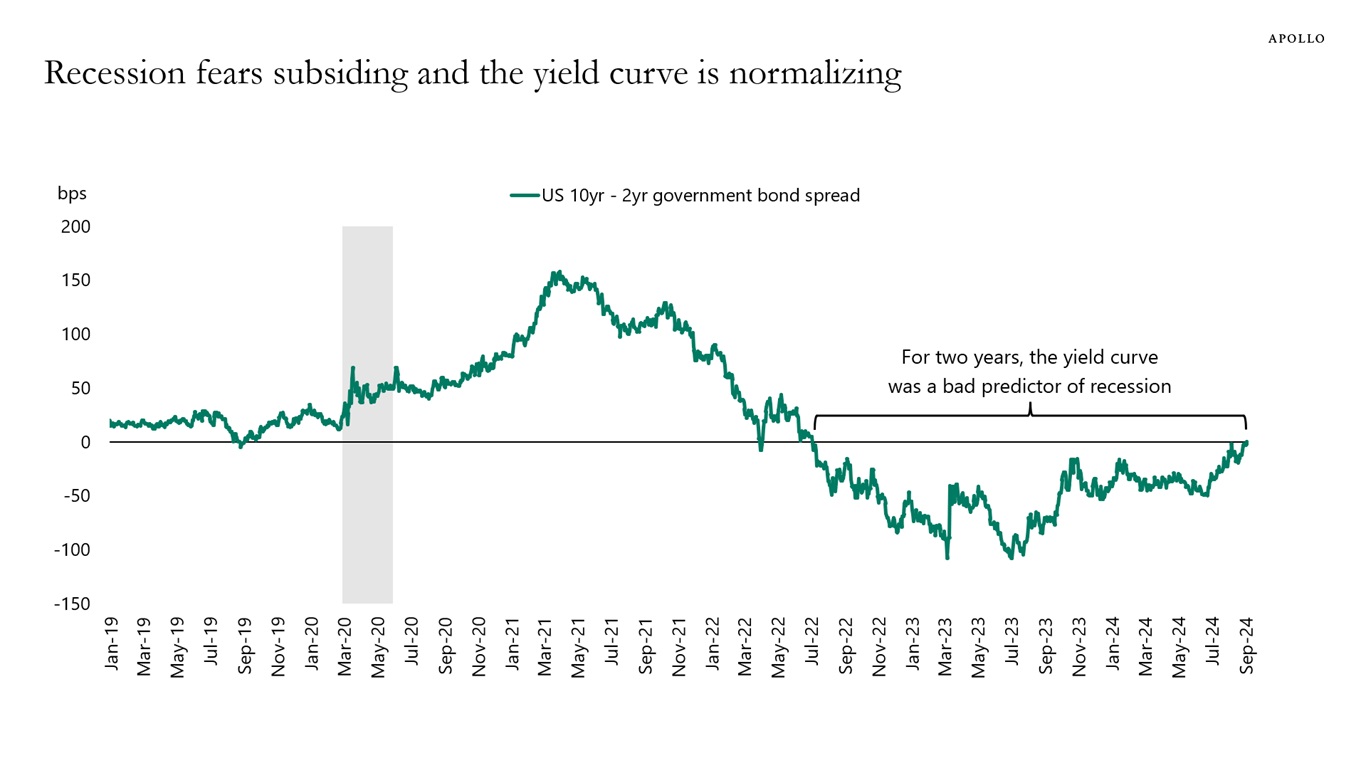

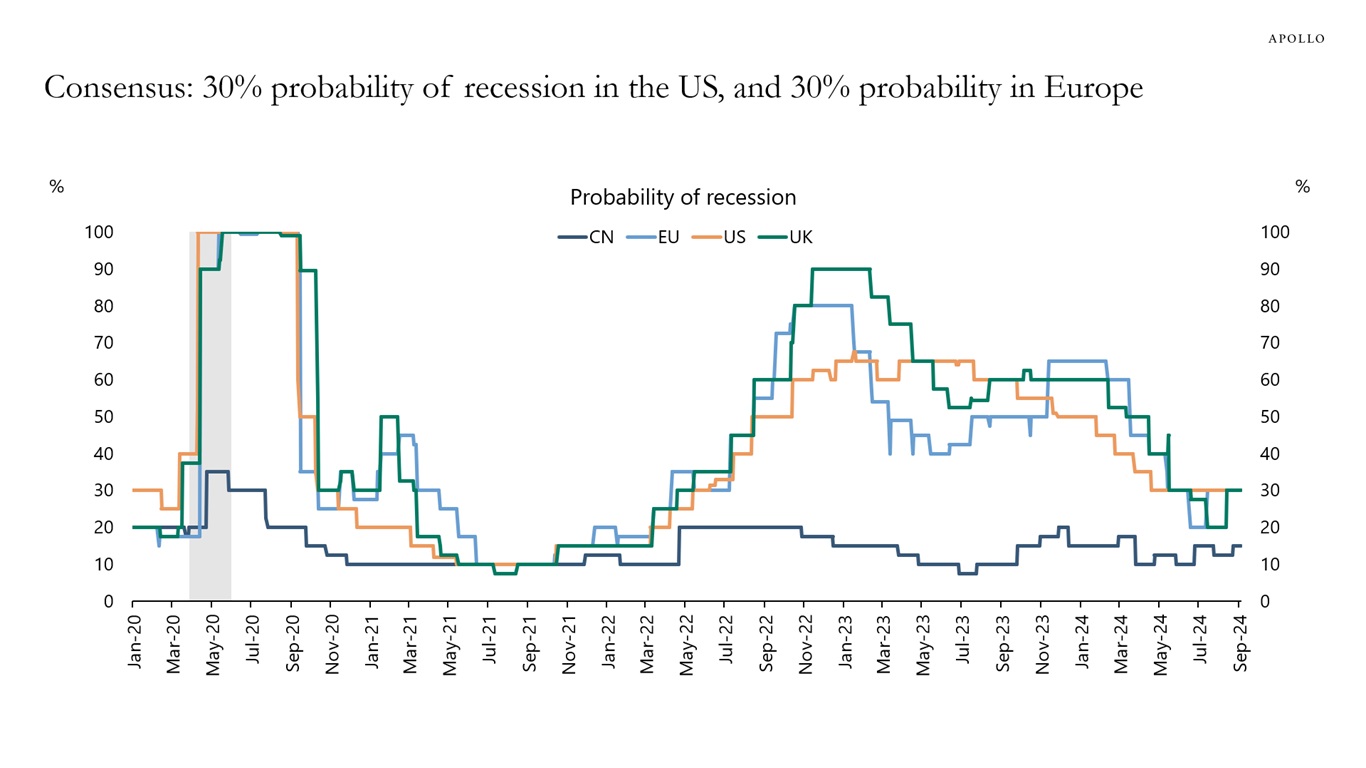

The yield curve is no longer inverted, and the recession probability is declining, see charts below.

To understand if a recession is coming, it is a better idea to look at the incoming data than to look at the yield curve because long rates are not only a reflection of the business cycle but also foreign demand, fiscal policy, and the term premium. And the incoming data continues to look just fine, see also here.

Source: Board of Governors of the Federal Reserve System, Bloomberg, Apollo Chief Economist

Source: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

Our latest US housing outlook is available here, and we remain constructive.

Why?

Because we only get a recession when the economy experiences a big shock such as Covid, Lehman, the IT bubble bursting, and the commercial real estate crisis in the early 1990s.

Today is not such a shock.

Today, we are experiencing a gradual slowdown engineered by the Fed. The Fed raised interest rates to slow down the economy to slow down inflation.

Inflation has now come down, and the Fed can begin to focus on other parts of the economy, particularly the labor market but also the housing market. If the Fed doesn’t like what they see, they will lower interest rates faster.

The bottom line is that the ongoing soft landing in the economy also implies a soft landing in the housing market.

See important disclaimers at the bottom of the page.

-

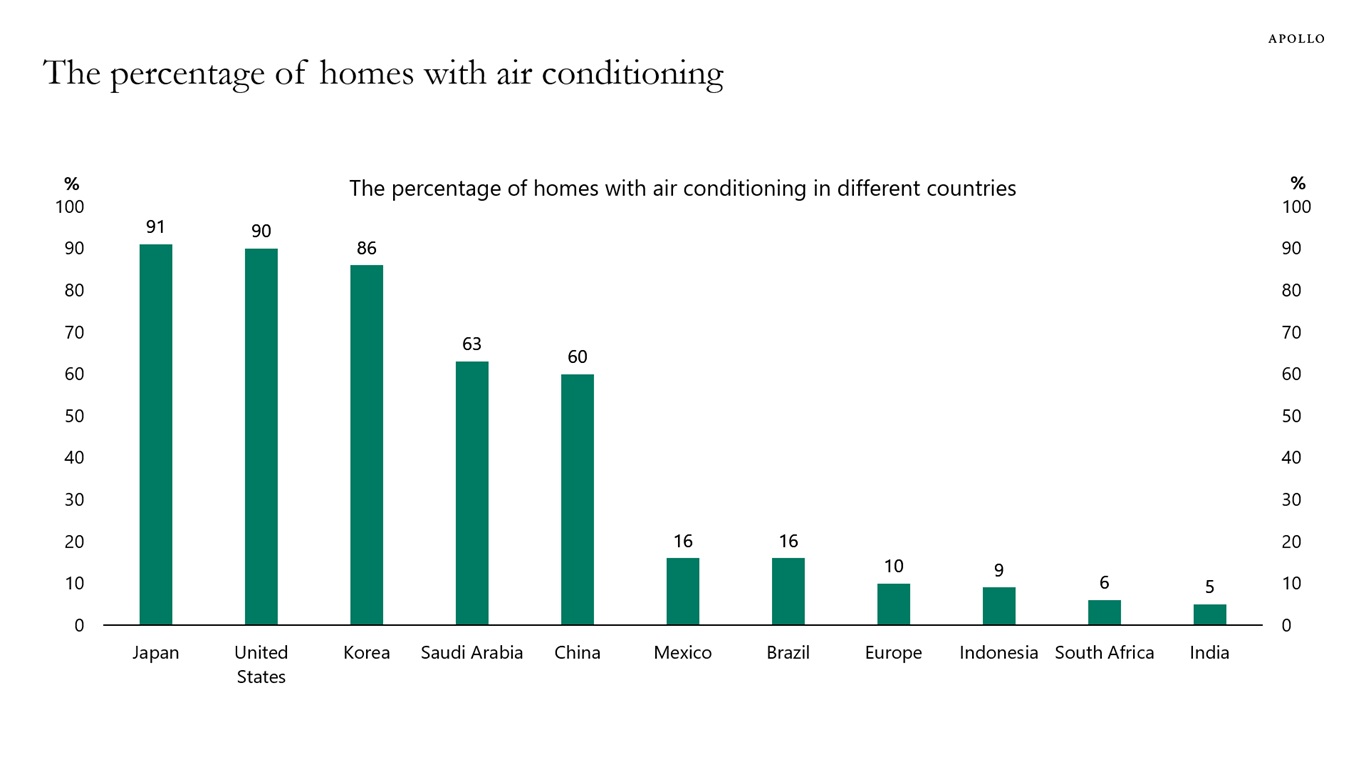

According to data from the International Energy Agency, 90% of homes in the US have air conditioning, but only 10% of homes in Europe and 5% of homes in India, see chart below. For China, the number is 60%.

Source: The Future of Cooling Report (2018) – International Energy Agency, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

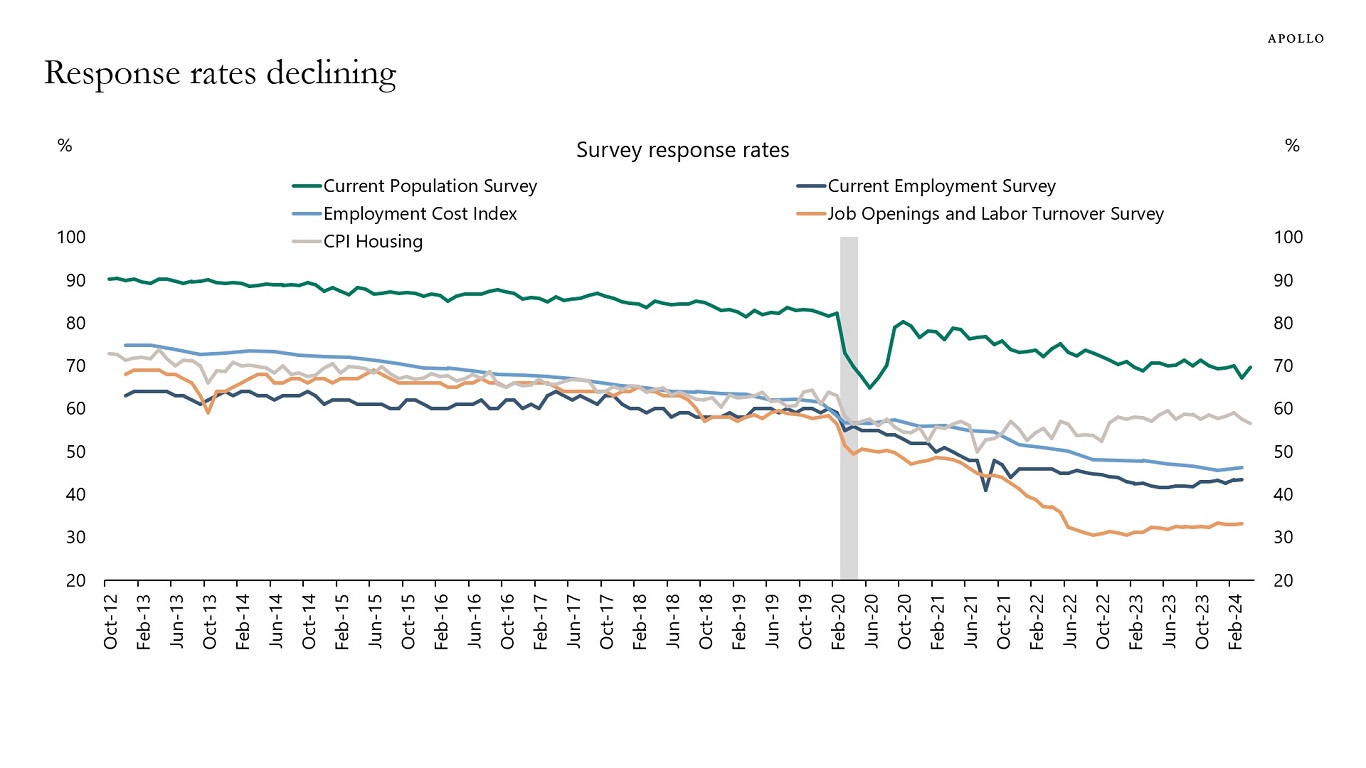

The unemployment rate is calculated based on the Current Population Survey, and the response rate for the Current Population Survey was 90% in 2012, and now it is around 70%.

Similarly, the response rate has declined across other important economic indicators, see chart below, and there is a new group of “survey professionals” that make multiple entries into the same survey, which may play a role in private surveys, see also here.

The bottom line is that the incoming data is more unreliable and creates extra uncertainty for investors and policymakers.

Source: BLS, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

Looking at the incoming data, the facts are the following:

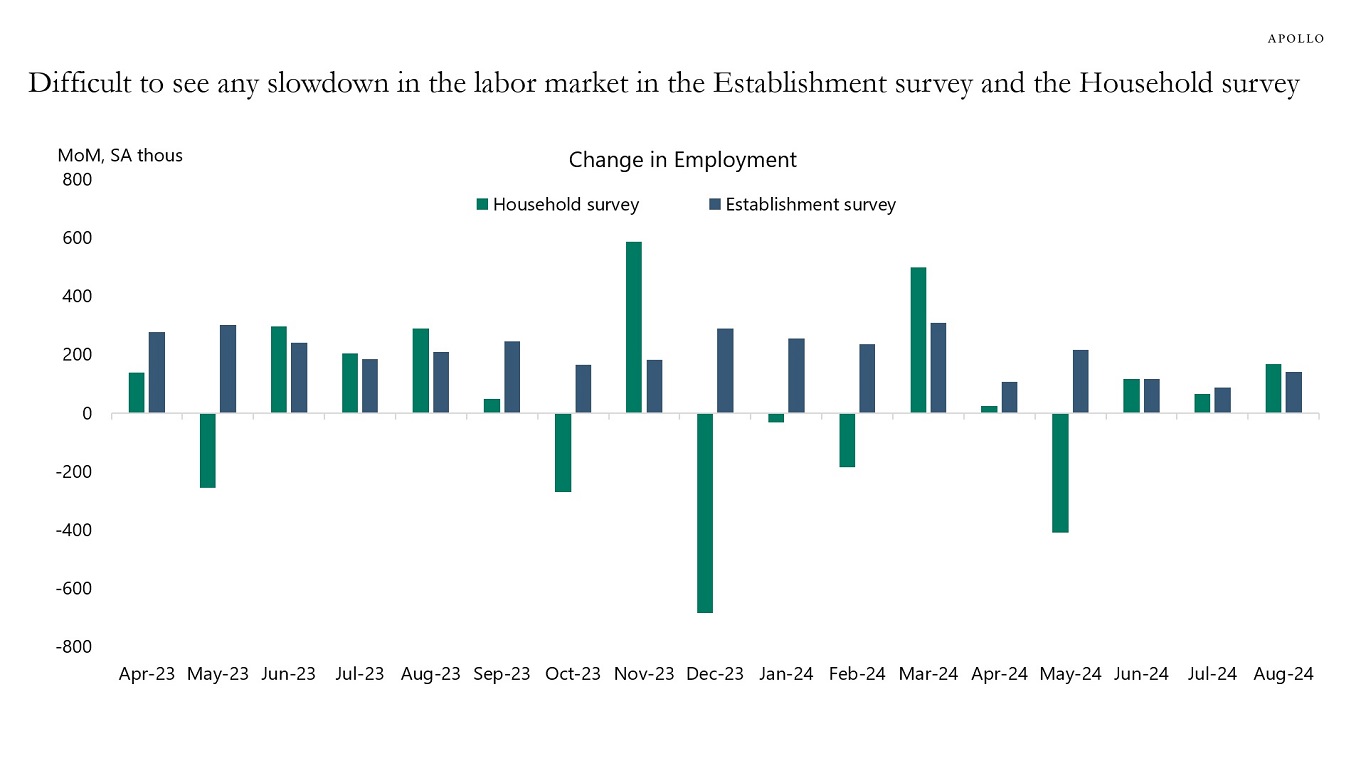

1. The unemployment rate declined in August, and looking at the establishment survey and the household survey, it is difficult to see strong signs of a slowdown in job creation, see chart 1.

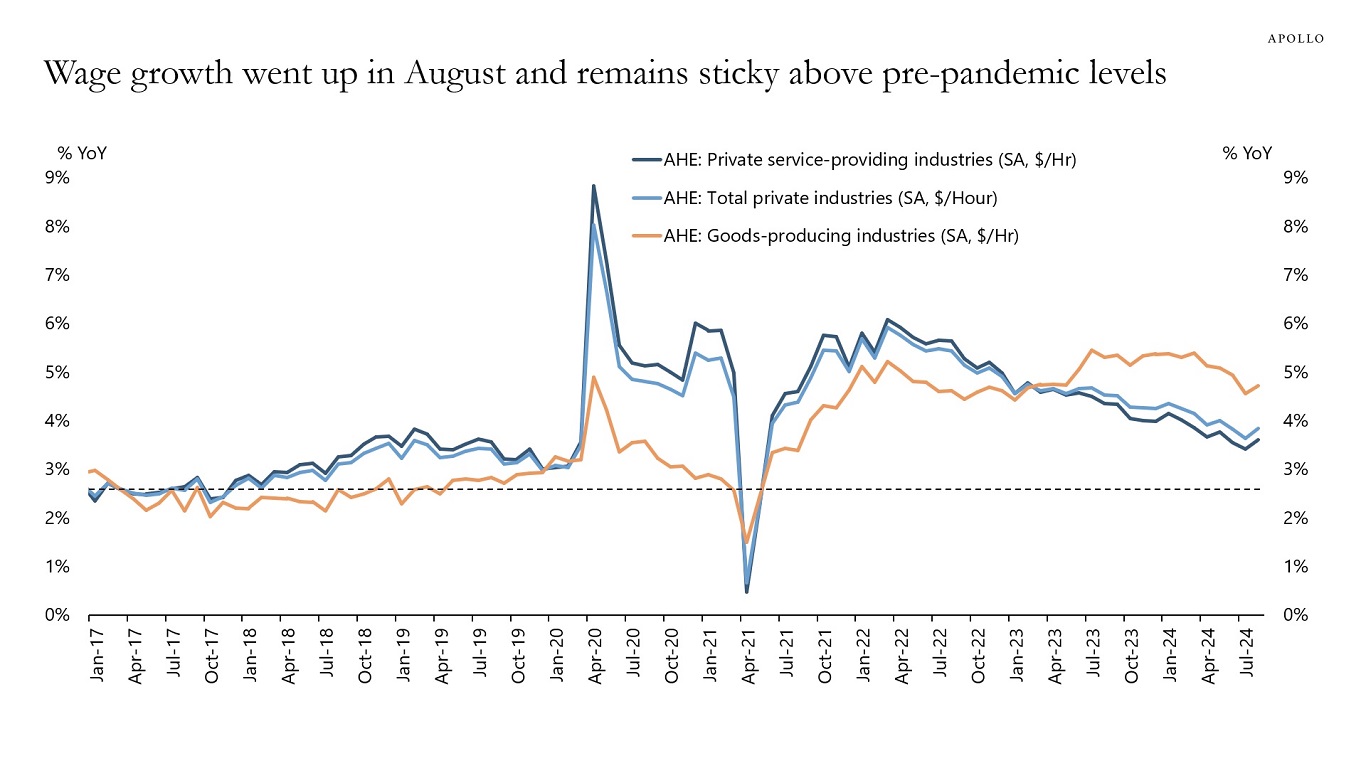

2. Wage growth accelerated to 3.8% in August and wage growth remains sticky well above pre-pandemic levels, see chart 2.

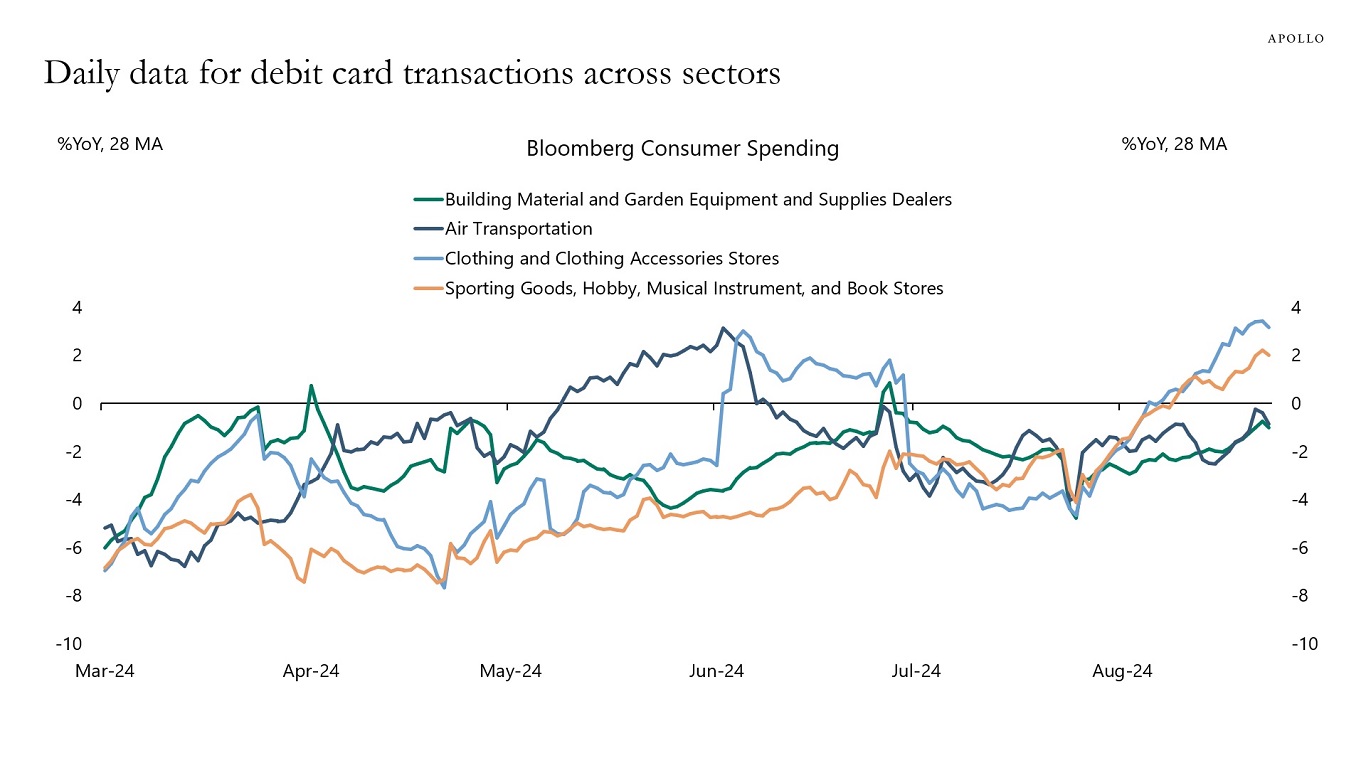

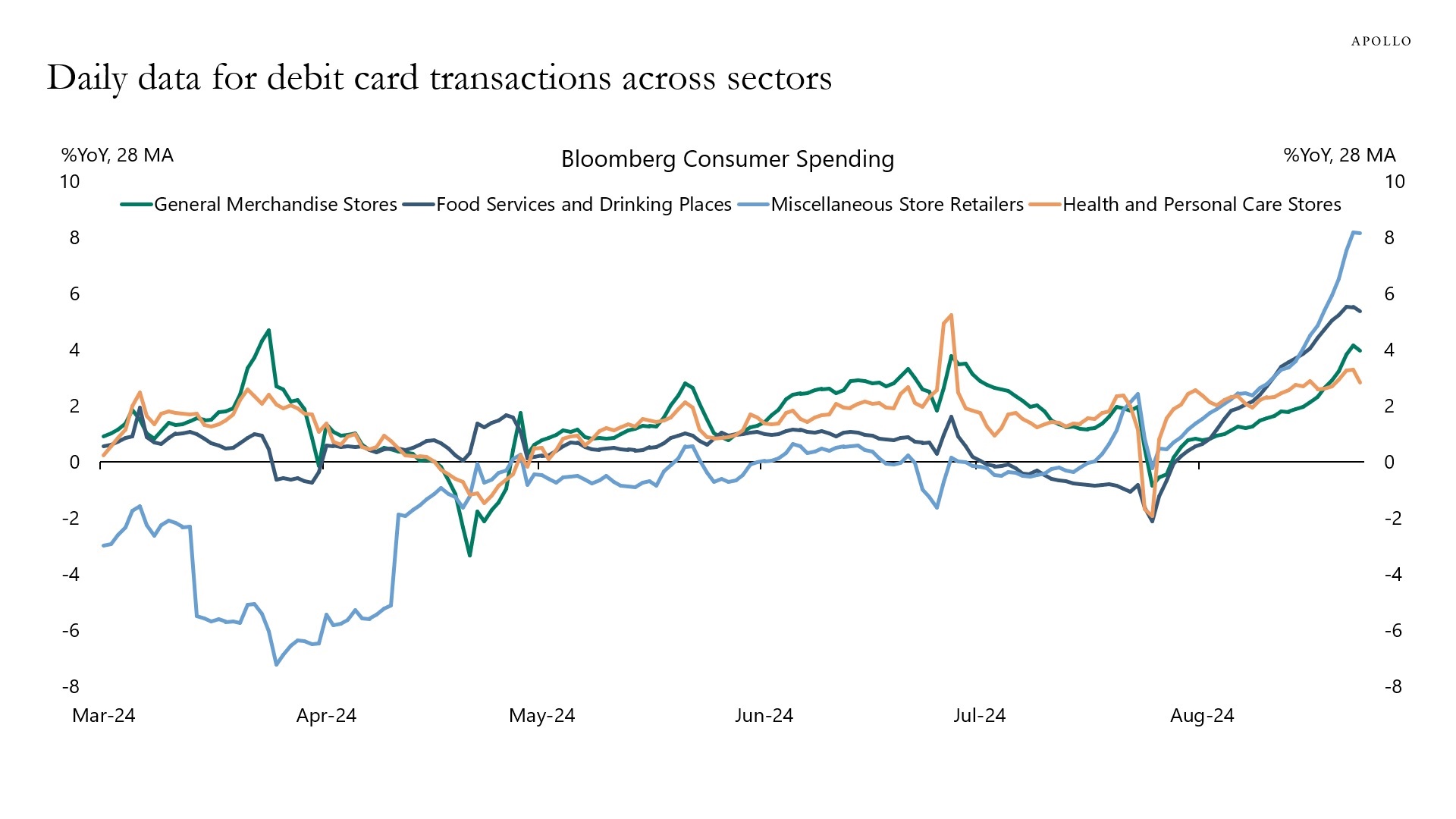

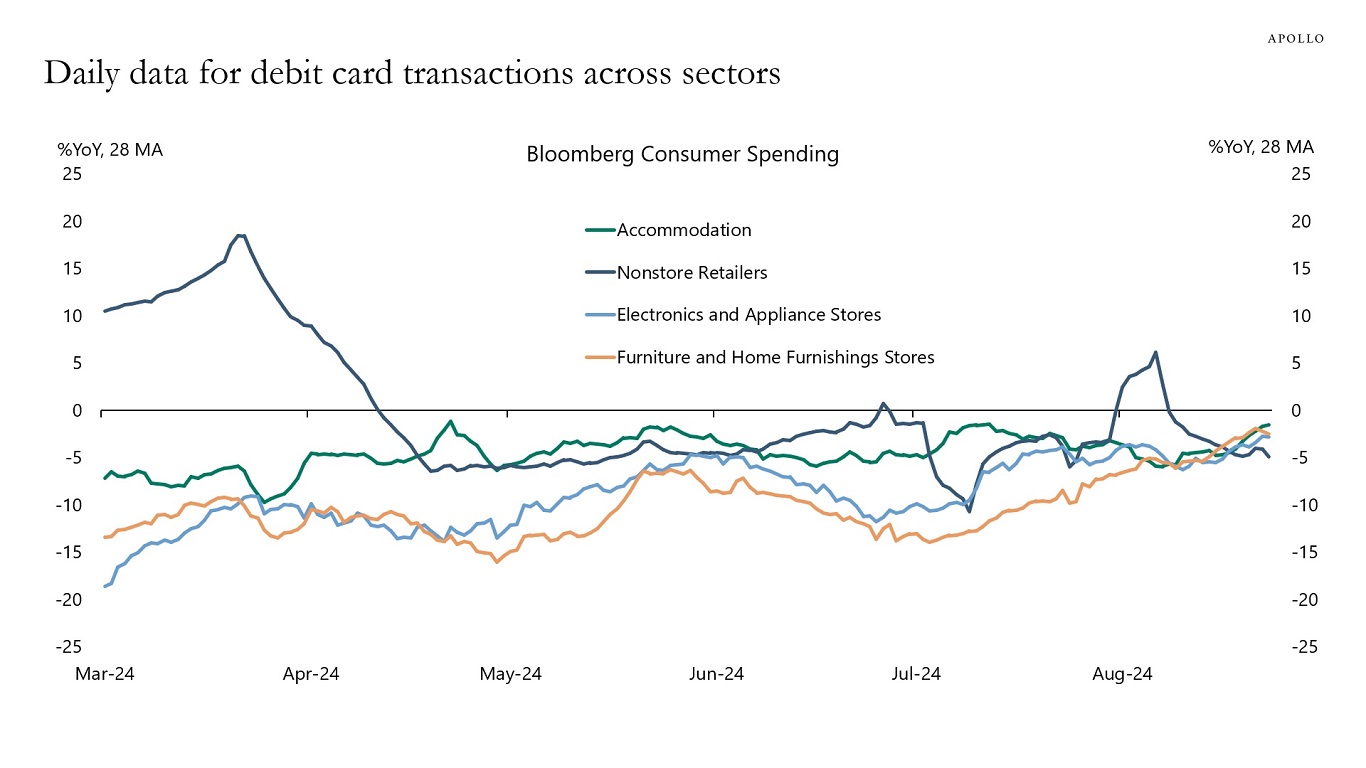

3. Daily data for debit card transactions shows that consumer spending has been accelerating in recent weeks, driven by spending on clothing, food services and drinking places, sporting goods, and motor vehicle and parts dealers, see the following five charts.

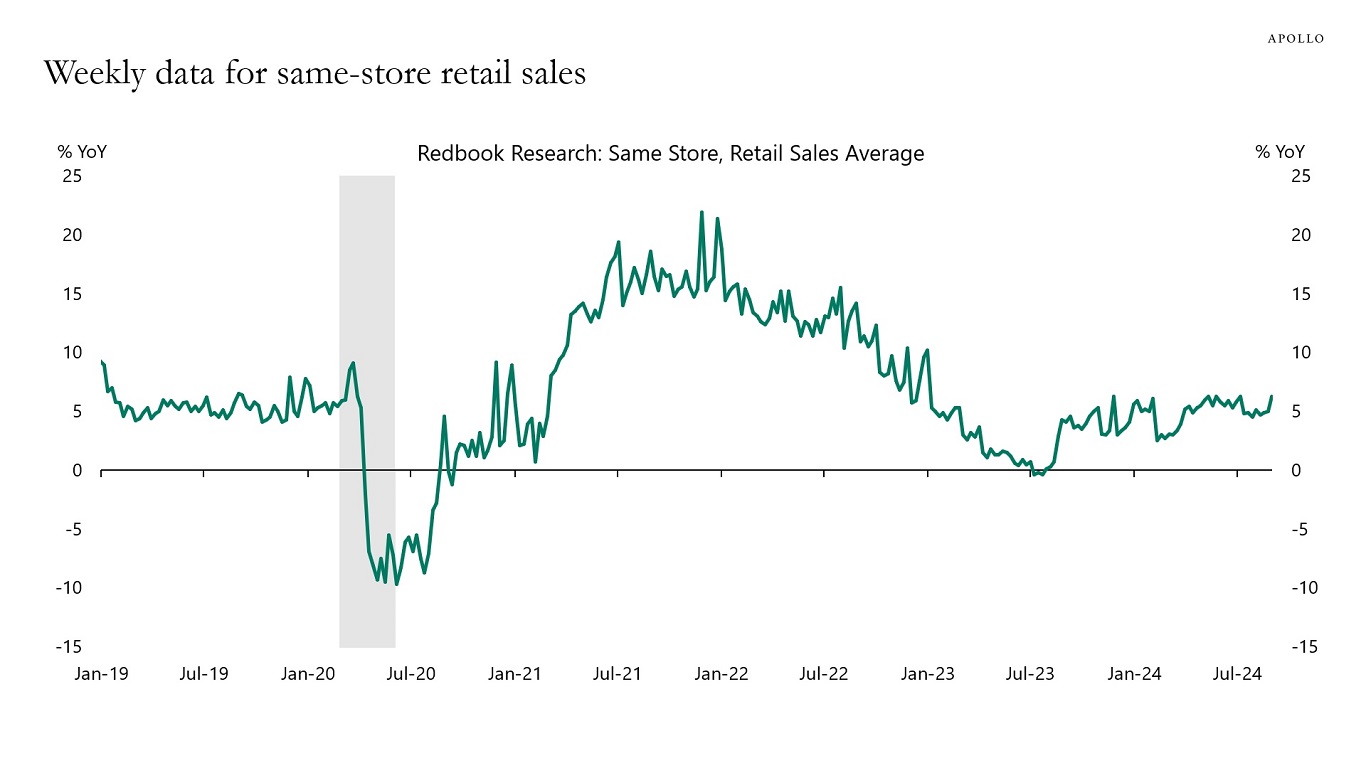

4. Weekly data for retail sales went up last week and remains solid, see chart 8.

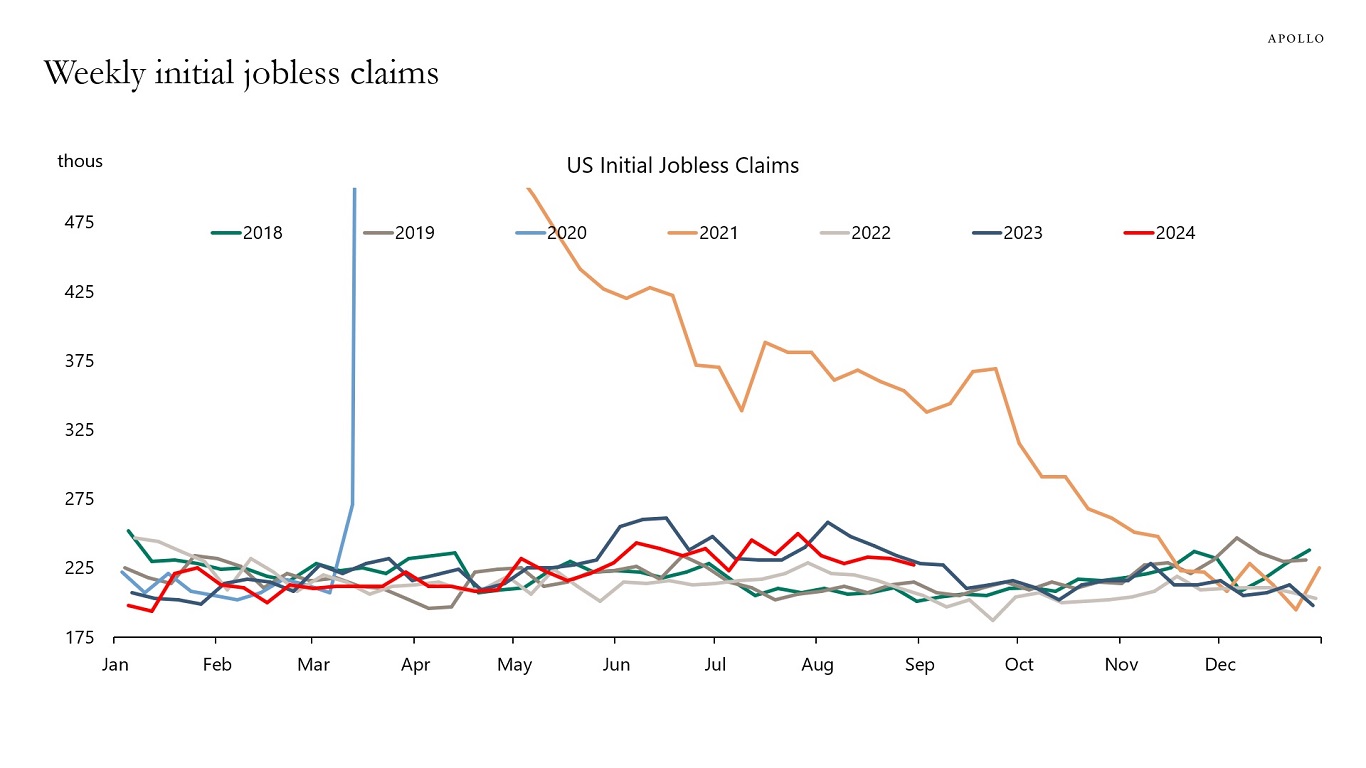

5. Jobless claims have declined for several weeks, see chart 9.

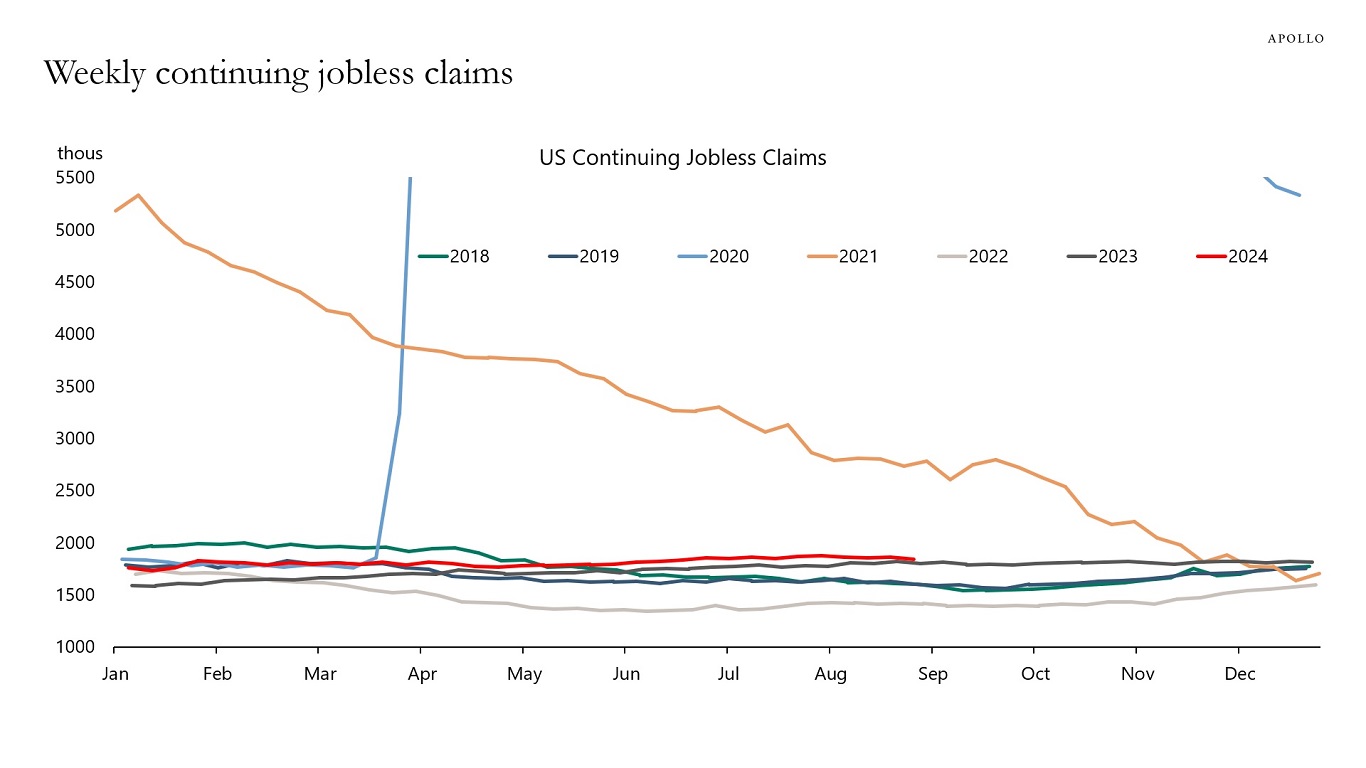

6. Continuing claims have declined for several weeks, see chart 10.

7. Default rates and weekly bankruptcy filings are trending down, see chart 11.

8. The Fed’s weekly GDP model suggests GDP is 2.4% and the Atlanta Fed GDP Now says GDP this quarter will be 2.1%, see charts 12 and 13.

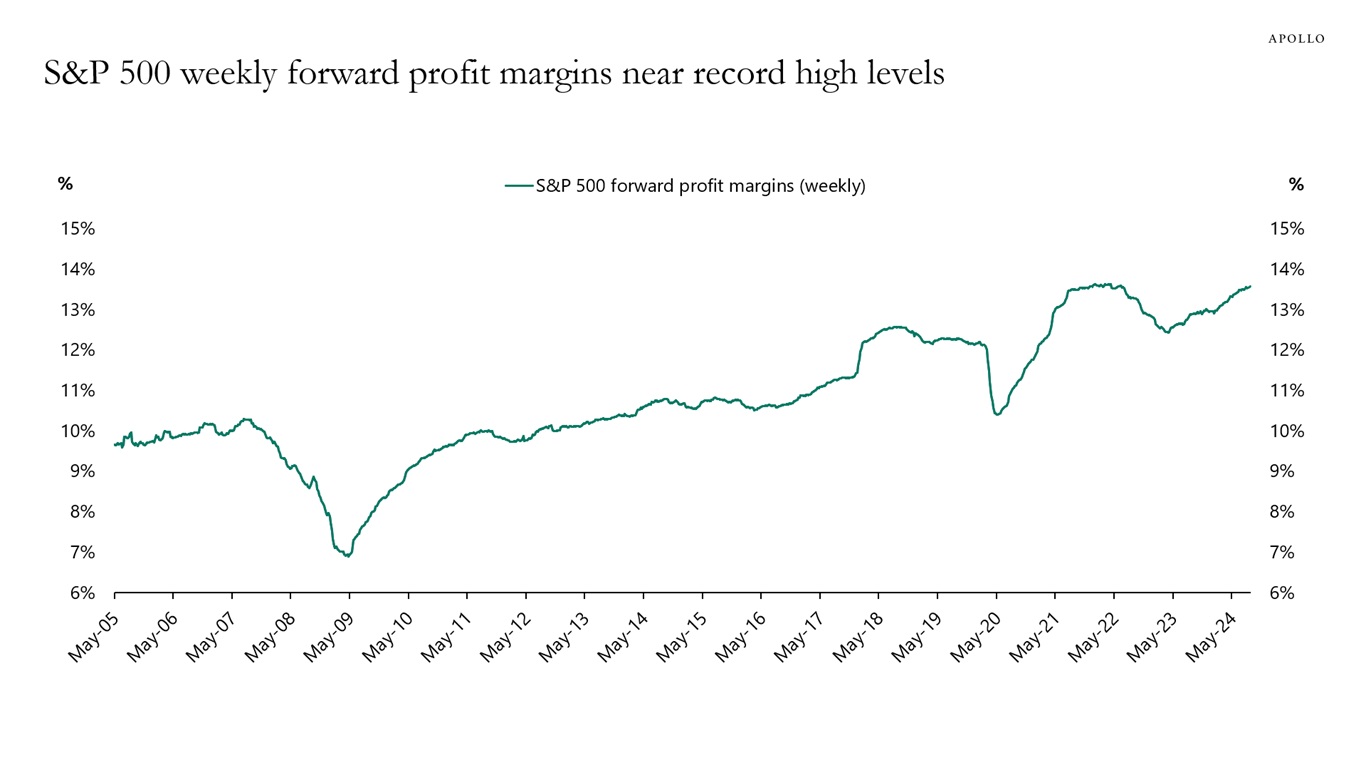

9. Weekly data for S&P 500 forward profit margins shows that profit margins are near all-time high levels, see chart 14.

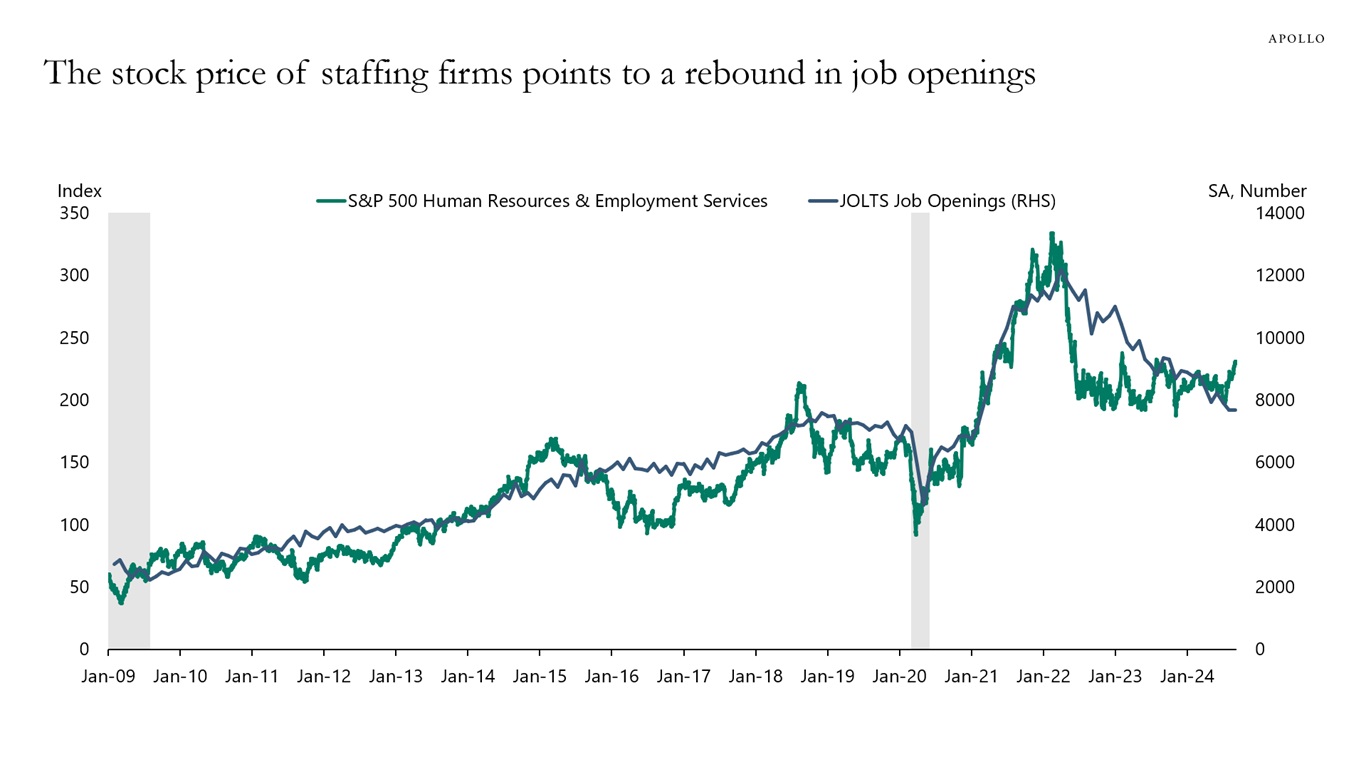

10. The stock price of staffing firms is rebounding, which suggests that we could get a rebound in job openings, see chart 15.

The bottom line is that the US economy is not in a recession, and there are no signs of a recession on the horizon. Our chart book with daily and weekly data is available here.

Source: BLS, Haver Analytics, Apollo Chief Economist

Source: BLS, Haver Analytics, Apollo Chief Economist

Note: Consists largely of debit card transactions. Source: Bloomberg, Apollo Chief Economist

Note: Consists largely of debit card transactions. Source: Bloomberg, Apollo Chief Economist

Note: Consists largely of debit card transactions. Source: Bloomberg, Apollo Chief Economist

Note: Consists largely of debit card transactions. Source: Bloomberg, Apollo Chief Economist

Note: Consists largely of debit card transactions. Source: Bloomberg, Apollo Chief Economist

Source: Redbook, Haver Analytics, Apollo Chief Economist

Source: US Department of Labor, Apollo Chief Economist

Source: US Department of Labor, Apollo Chief Economist

Note: Filings are for companies with more than $50mn in liabilities. For week ending on September 5, 2024. Source: Bloomberg, Apollo Chief Economist

Source: Federal Reserve Bank of Dallas, Bureau of Economic Analysis, Apollo Chief Economist

Source: Federal Reserve Bank of Atlanta, Haver Analytics Apollo Chief Economist

Note: The 12 months forward profit margins are calculated by using the weighted average of 1FY (current year estimate) and 2FY (next year estimate) to smooth out fiscal year transitions. Source: Bloomberg, Apollo Chief Economist

Source: Bloomberg, BLS, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

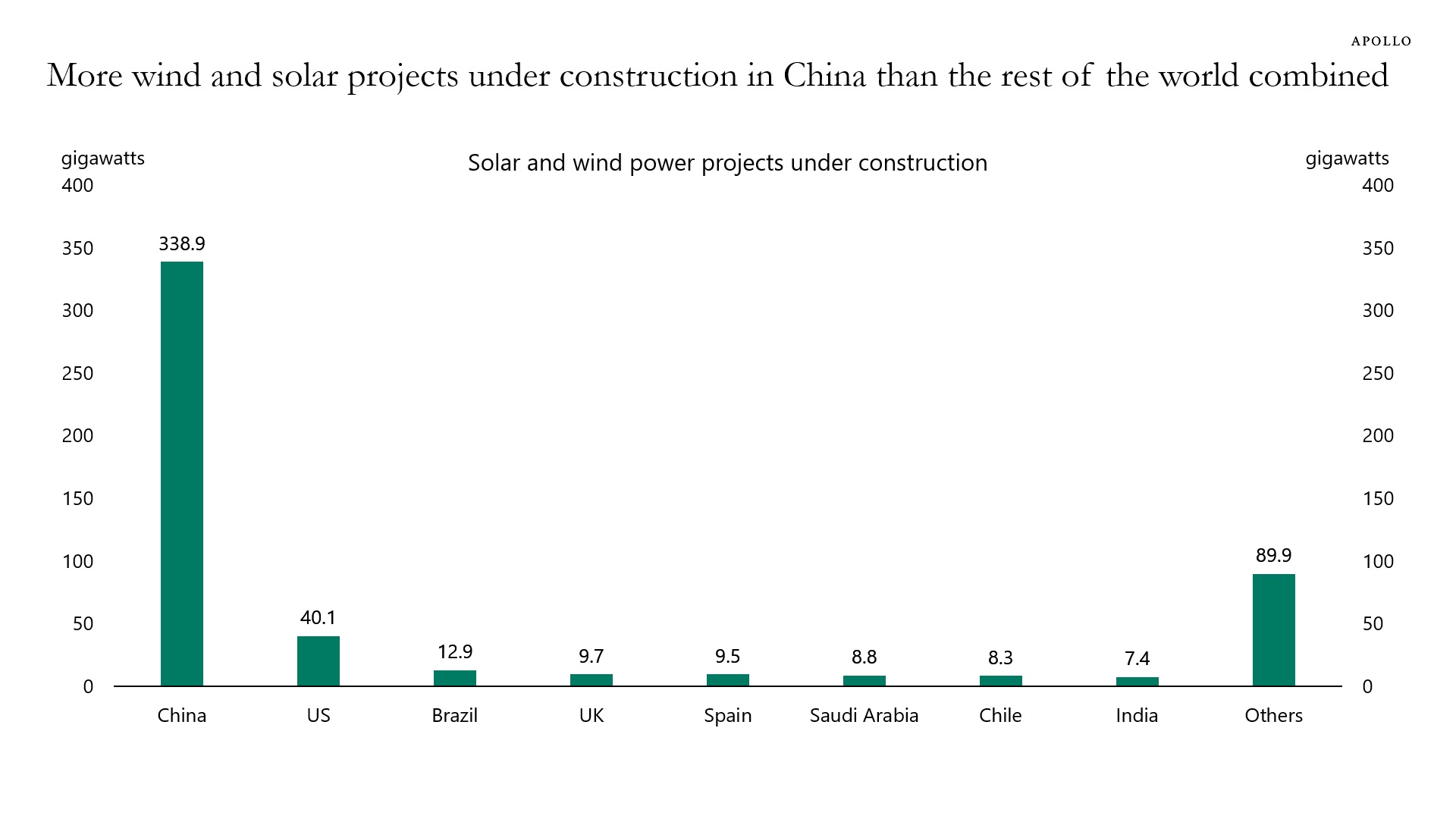

There are more solar and wind power projects under construction in China than in all other countries combined, see chart below.

Data for China and European countries to June 2024. All other countries to December 2023. Source: Global Energy Monitor, Apollo Chief Economist See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.