Want it delivered daily to your inbox?

-

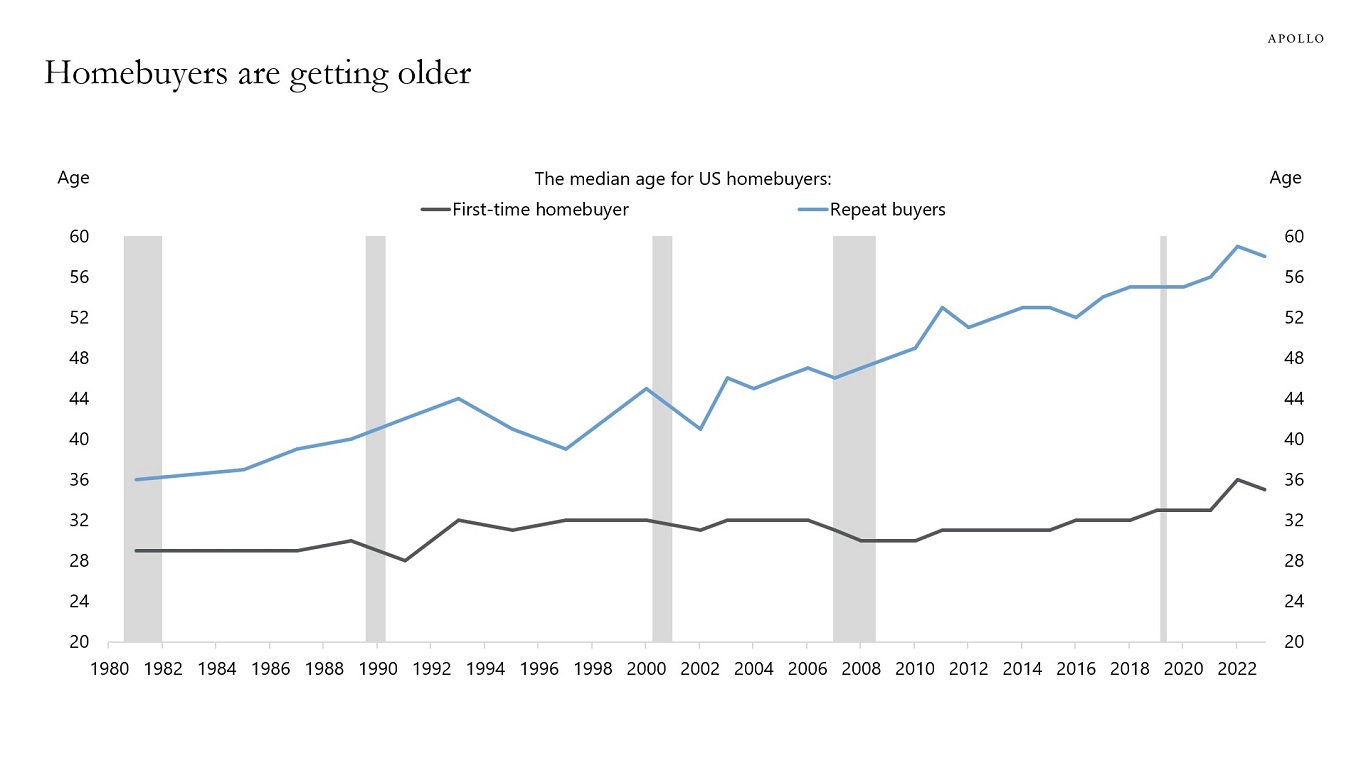

The median age of repeat homebuyers has increased from 36 years old in 1980 to 58 years old in 2023, see chart below.

And the median age of first-time homebuyers has increased from 29 to 35 over the same period.

Source: NAR, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

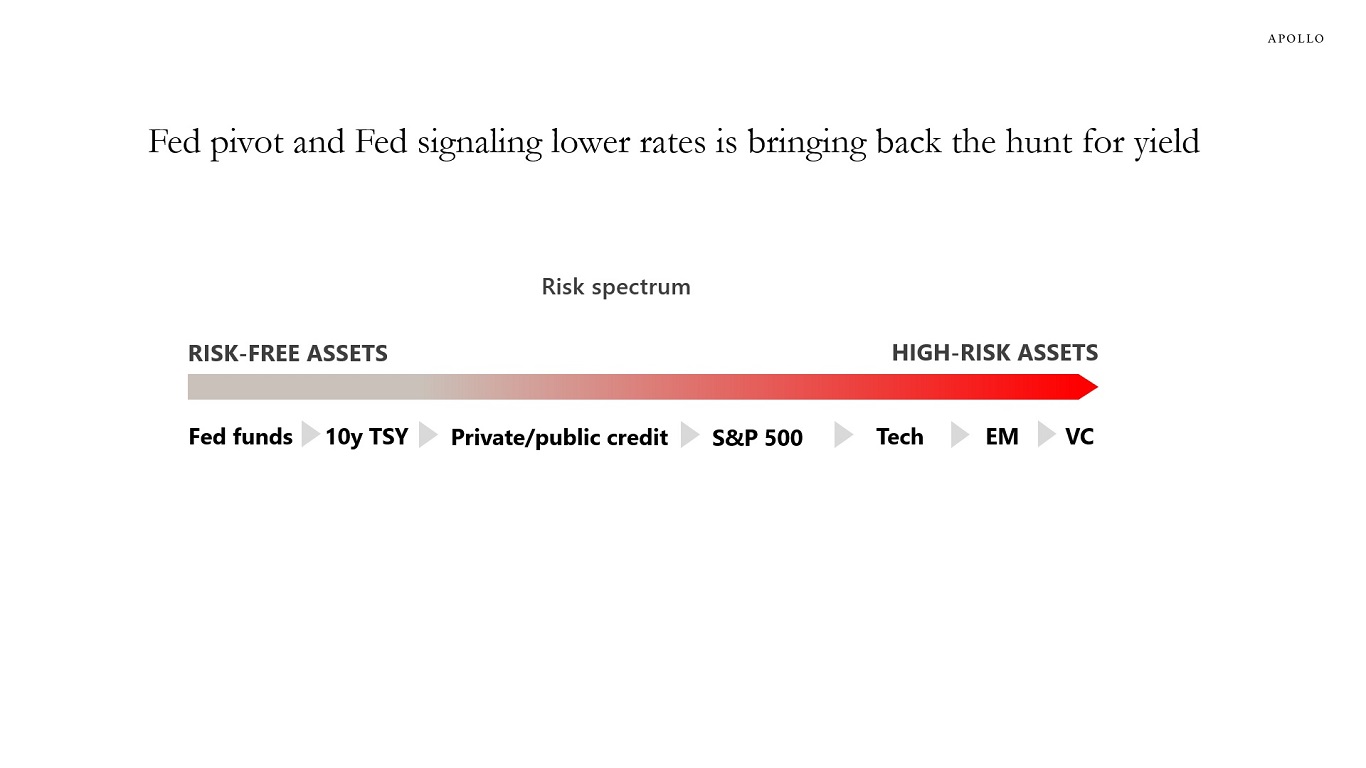

The Fed pivot has restarted the hunt for yield, see chart below. The question for markets is whether the associated rebound in housing, hiring, and capital markets activity will trigger a rebound in inflation.

Source: Apollo Chief Economist See important disclaimers at the bottom of the page.

-

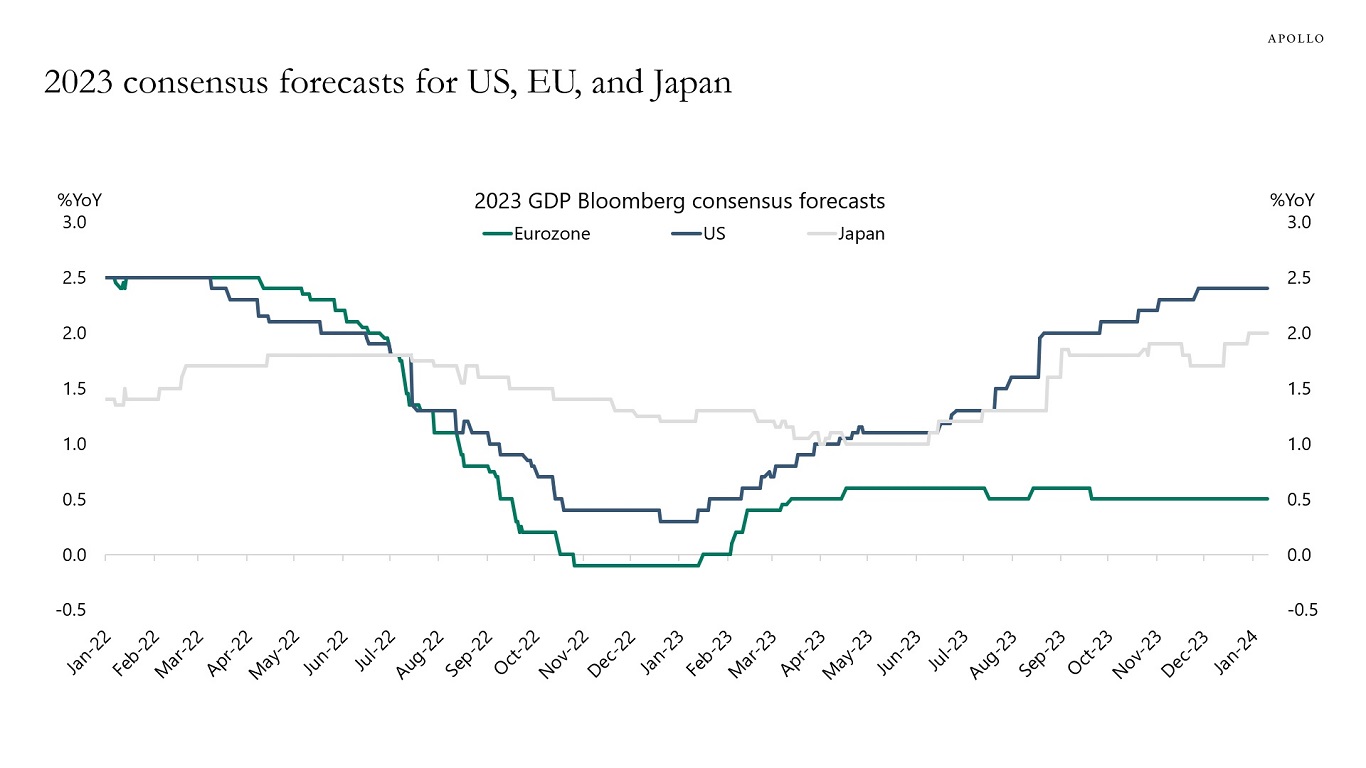

The story in markets in 2023 was that US growth expectations were first revised down and then revised up after the easing in financial conditions following SVB in March, see the first chart below.

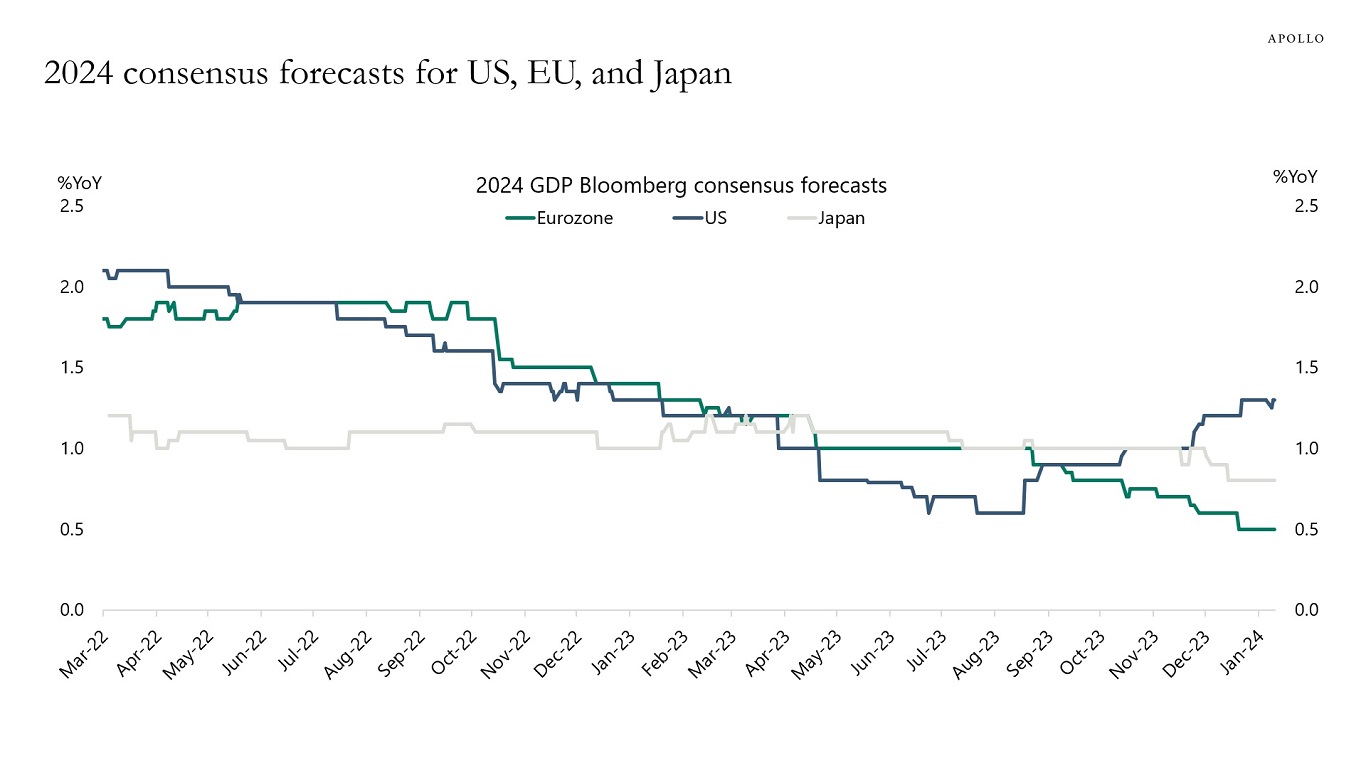

With the significant easing in financial conditions since November, we are beginning to see the same pattern in 2024, see the second chart.

The performance has been different in Japan and Europe, where growth expectations have been steady in Japan and revised significantly lower in Europe.

In other words, the lack of a slowdown in 2023, which surprised the Fed, the consensus, and markets, was only a US story, and we are starting to see the same pattern play out again in 2024.

Source: Bloomberg, Apollo Chief Economist

Source: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

The rally in rates and credit after the Fed pivot has pushed up the share of single-B and BB loans priced above par, see chart below.

Source: Pitchbook LCD, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

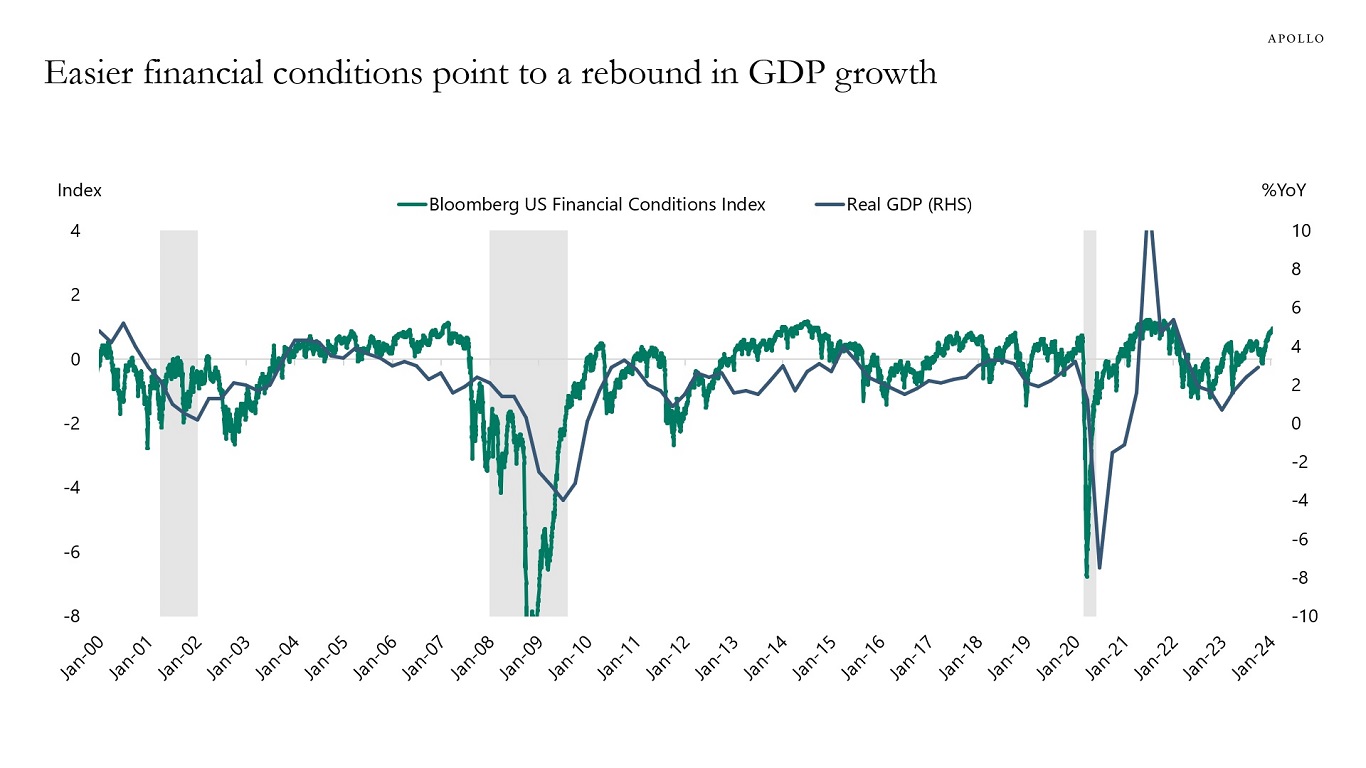

The ongoing easing of financial conditions continues to point to a reacceleration in growth over the coming months, see chart below.

Source: BEA, Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

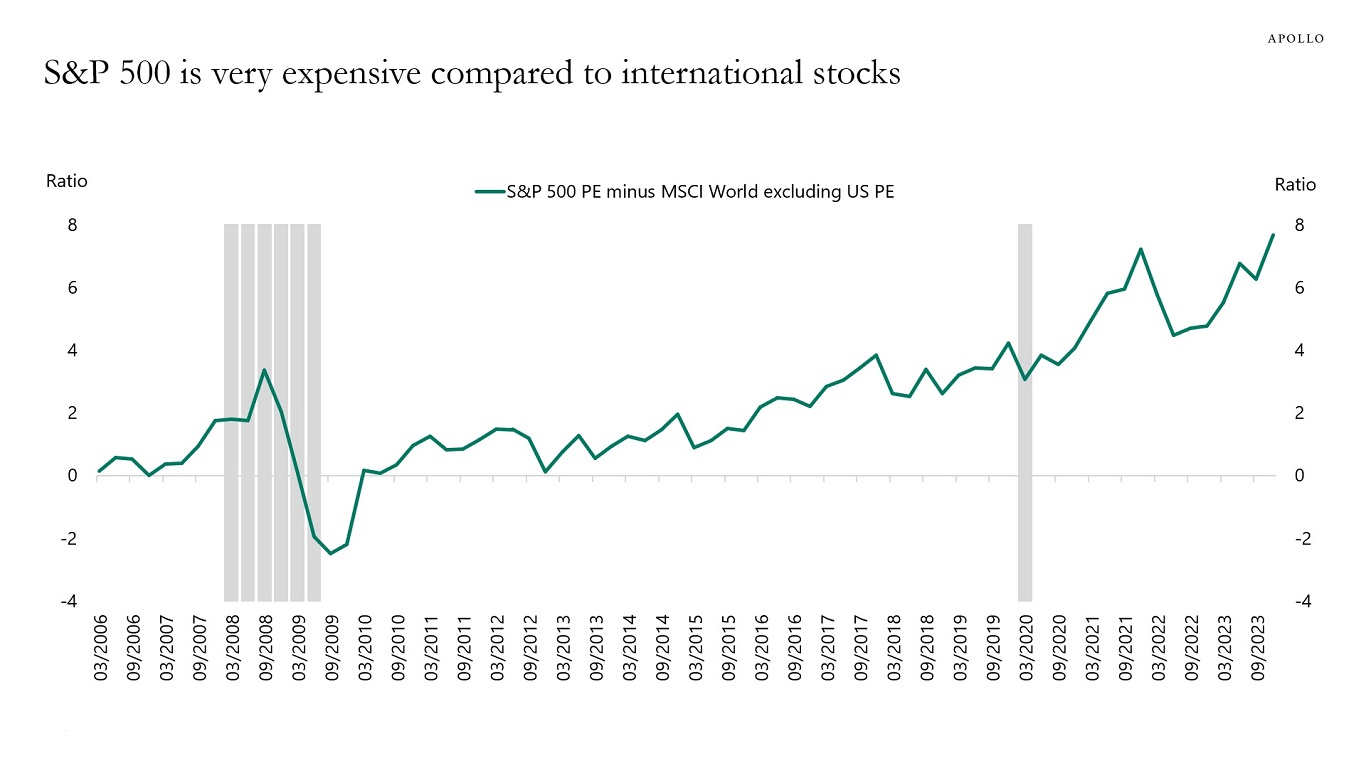

Comparing the P/E ratio of the S&P 500 with the P/E ratio of the rest of the world shows a record difference, see chart below.

In other words, US equities have never been more expensive relative to international equities.

Source: Bloomberg, Apollo Chief Economist (Note: BEst PE ratio using 12-month forward earnings; BEst = Bloomberg estimates) See important disclaimers at the bottom of the page.

-

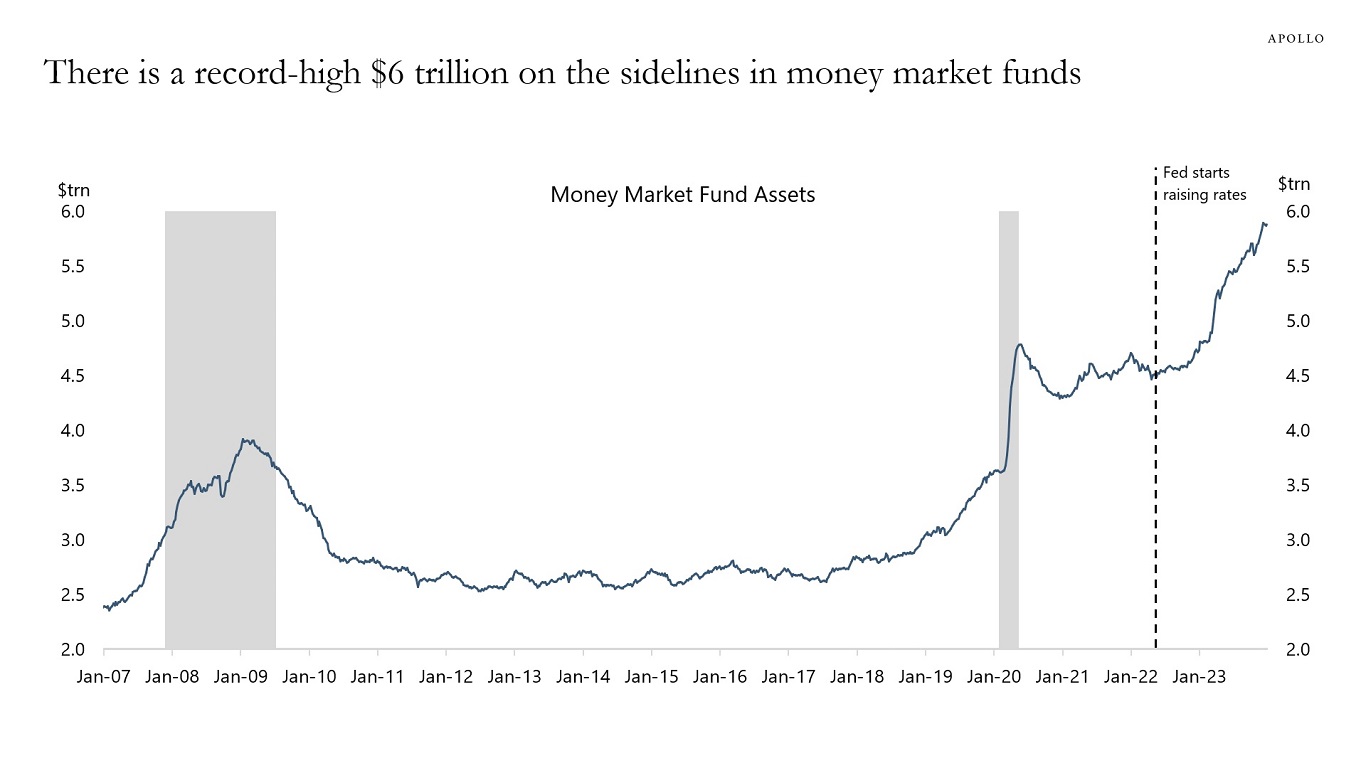

Since the Fed started raising rates in March 2022, the amount of money in money market funds has increased from $4.5 trillion to $6 trillion, see chart below.

With the Fed cutting rates over the coming quarters, we will likely see some of the $6 trillion leave overnight risk-free fixed income and flow into other asset classes such as equities, credit, and duration.

The record-high $6 trillion in money market accounts is likely a tailwind to equities, credit, and rates, and ultimately the economy—in particular hiring, housing, and inflation.

Source: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

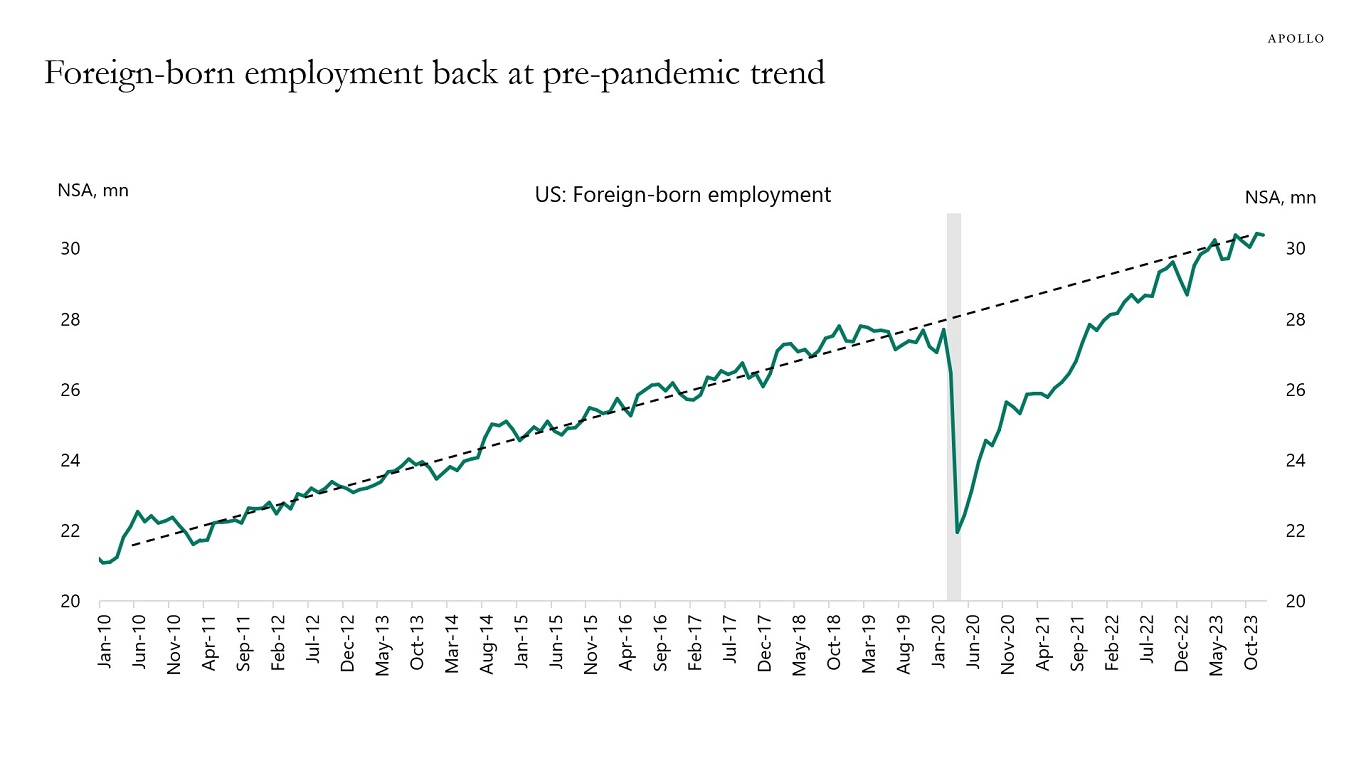

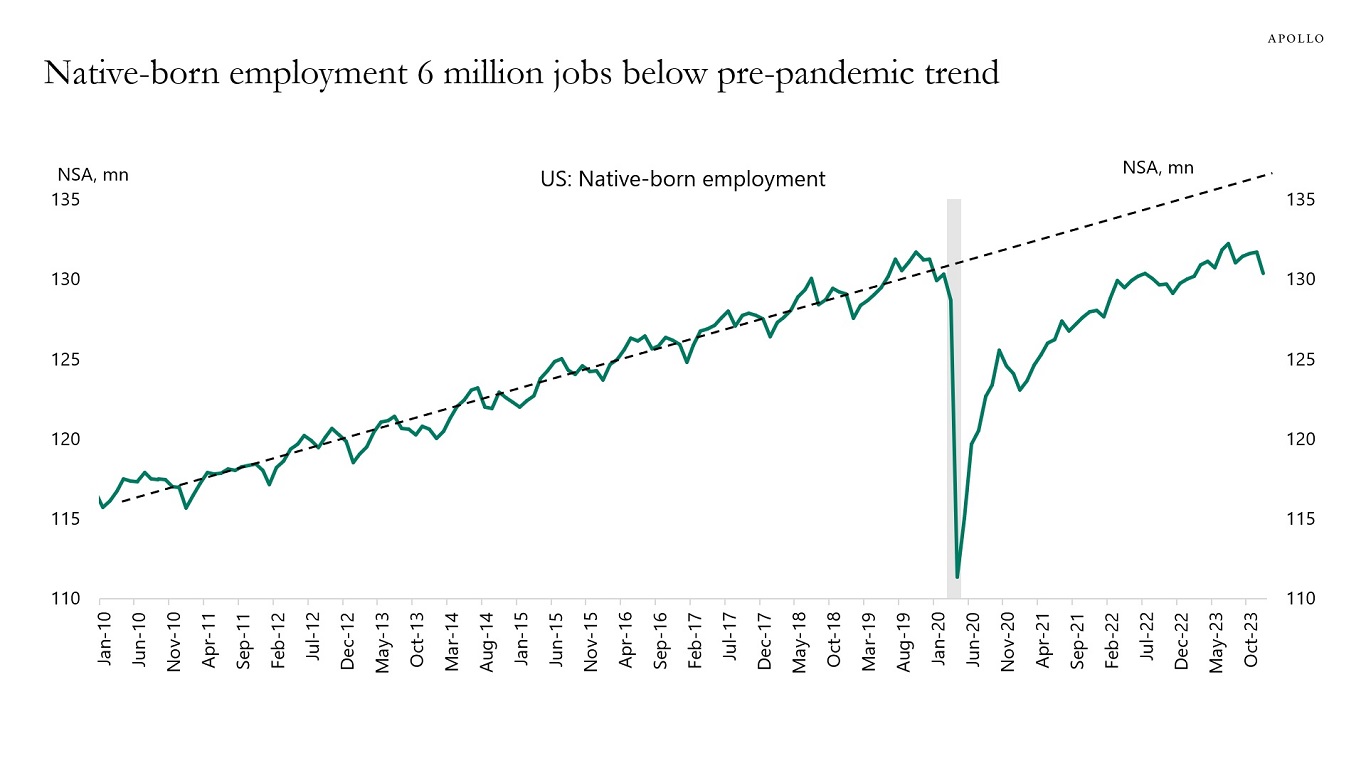

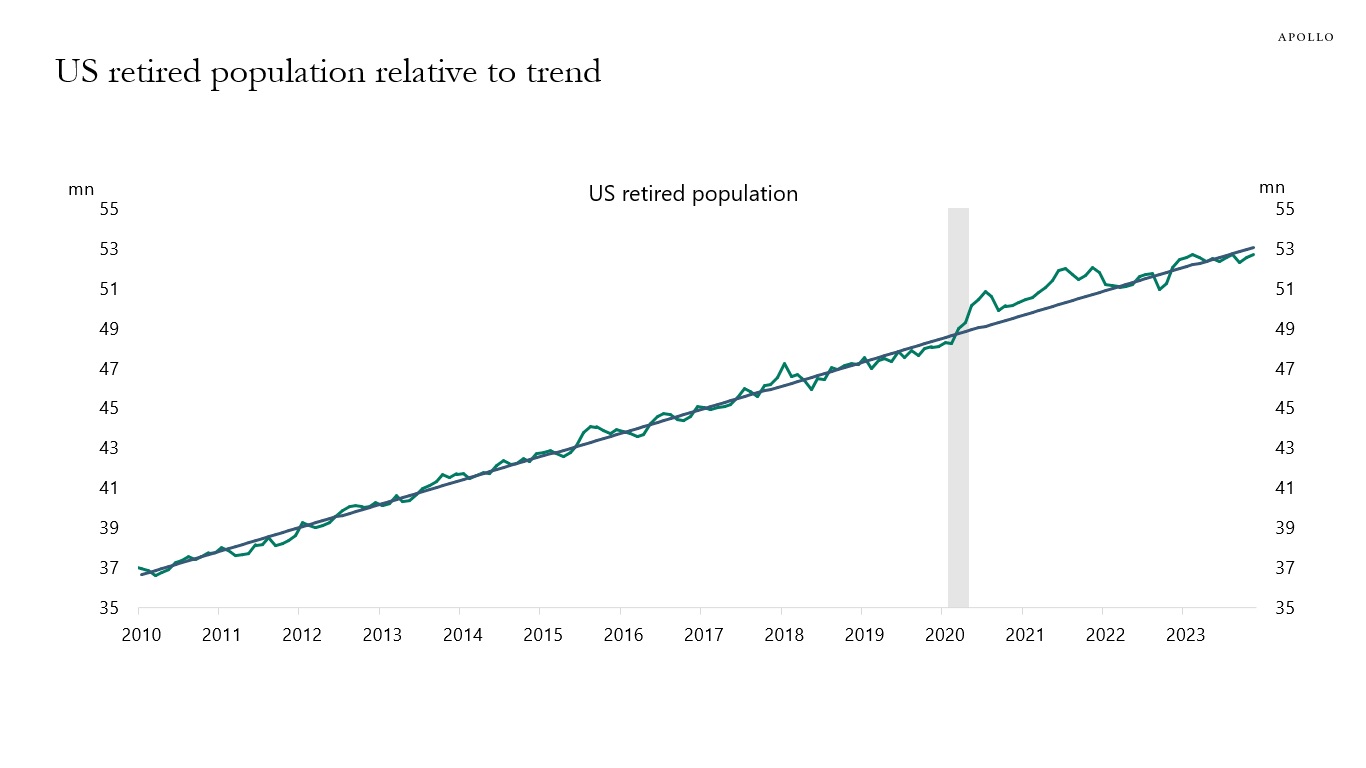

Foreign-born employment in the US is back at the pre-pandemic trend, and native-born employment is still 6 million jobs below the pre-pandemic trend, see the first two charts below.

In other words, the post-Covid normalization in the labor force participation rate has mainly been driven by immigration.

At the same time, the number of retired individuals has remained on trend, see the third chart.

The bottom line is that even taking into account that about 1 million died from Covid, there are still around 5 million native-born workers missing.

These 5 million missing workers are the reason why the labor market is tight and why wage inflation is likely to remain elevated.

Put differently, there is still plenty of room for job growth.

Source: BLS, Haver Analytics, Apollo Chief Economist

Source: BLS, Haver Analytics, Apollo Chief Economist

Source: Kansas City Fed, CPS IPUMS, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

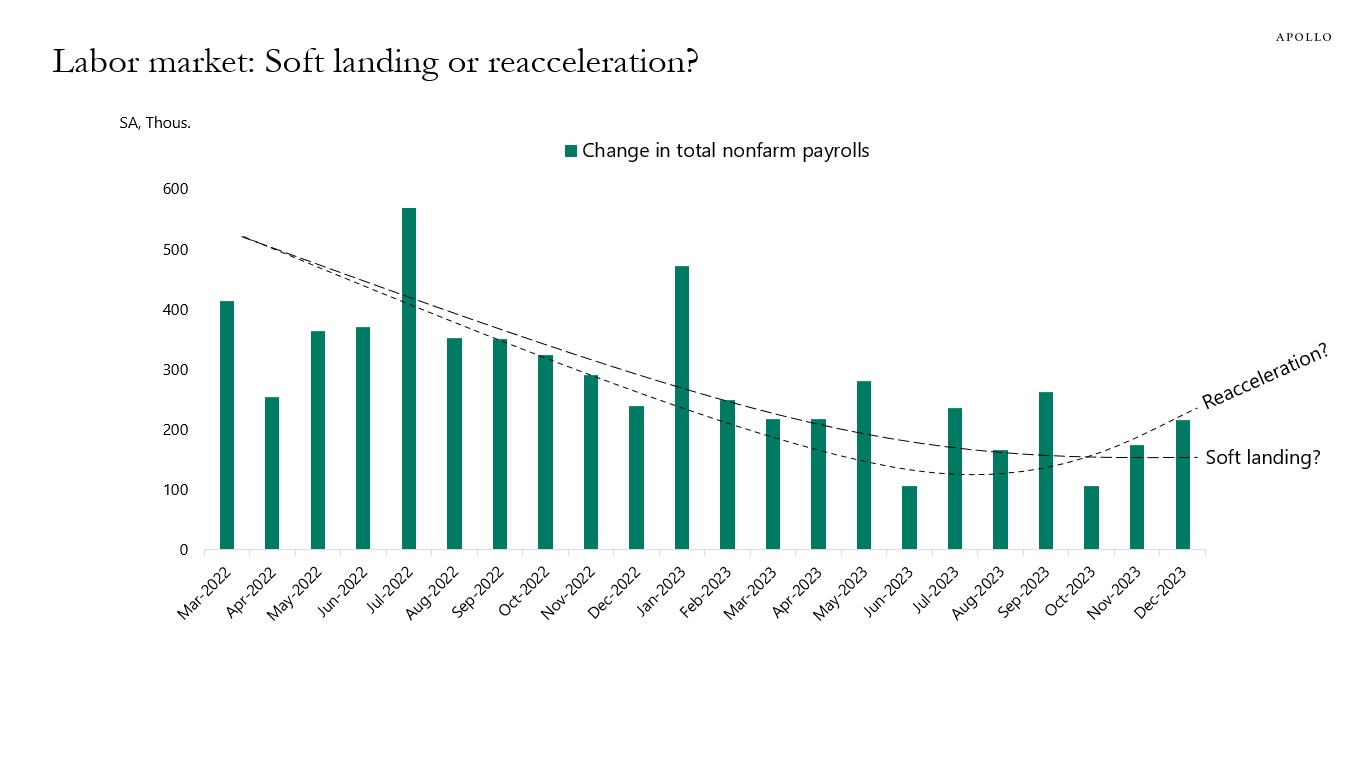

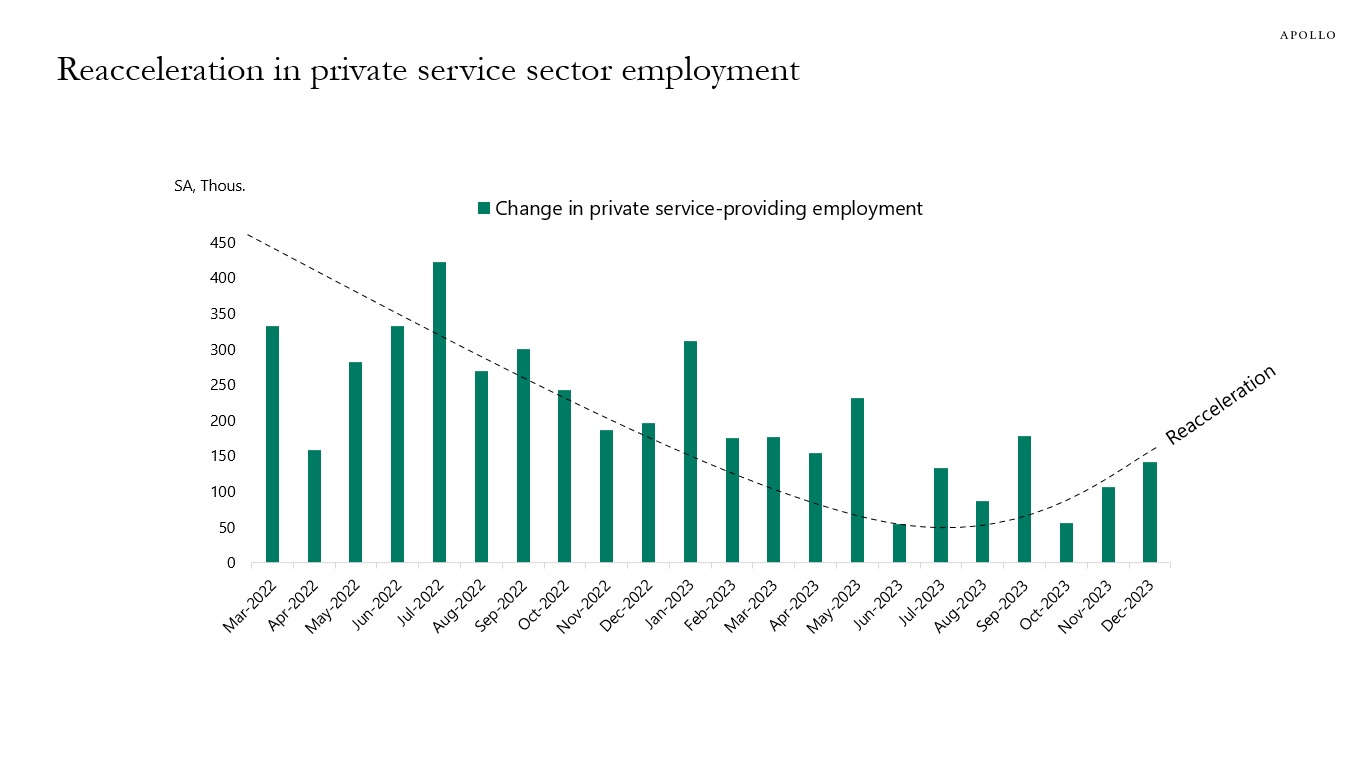

Looking at job growth since the Fed began to hike raises questions about whether the labor market is undergoing a soft landing or reacceleration, see the first chart below.

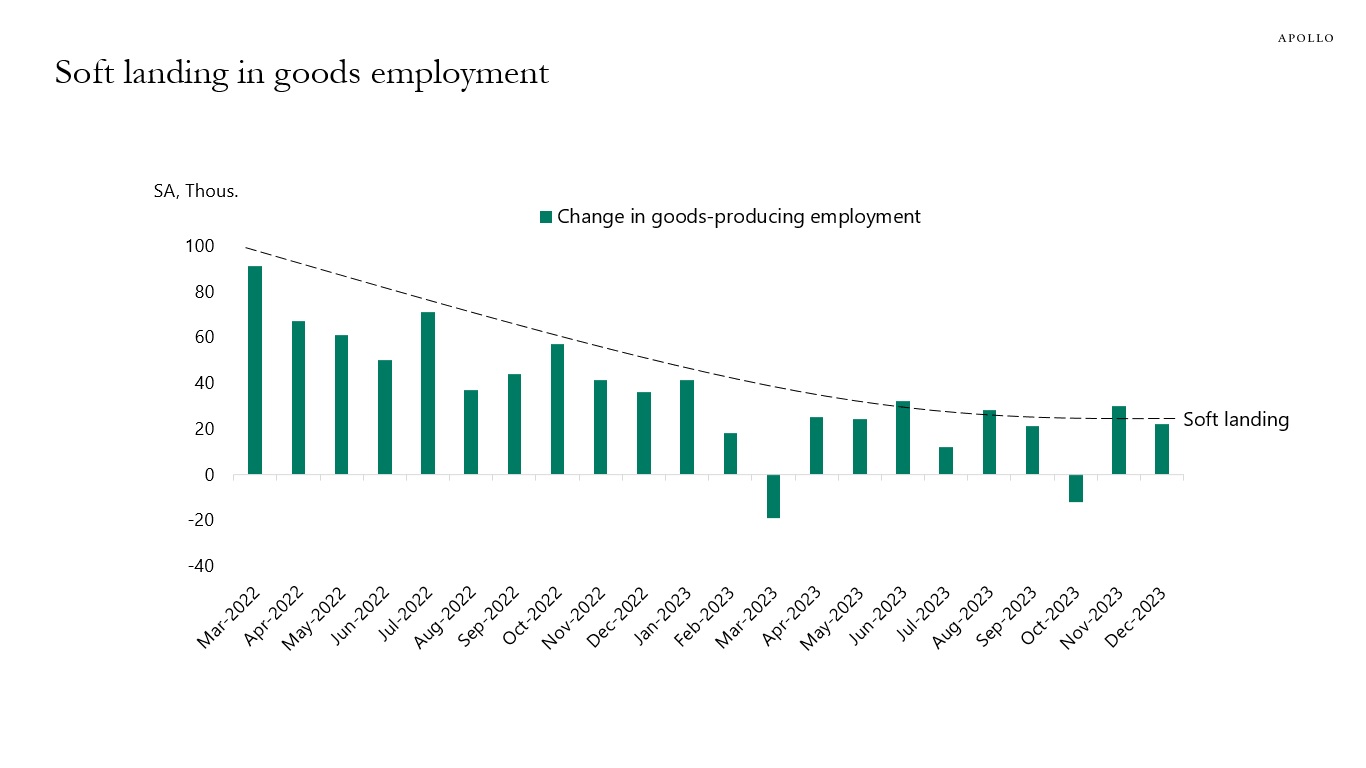

The split between the goods sector and the private service sector shows what looks like a soft landing in the goods sector and a reacceleration in the private service sector, see the second and third charts.

The no landing in services is consistent with ongoing strong demand for airlines, hotels, restaurants, concerts, and sporting events.

With the service sector making up 72% of total employment and generally less sensitive to Fed hikes, and with jobless claims still at very low levels, the upside risks to employment over the coming months are significant.

Source: BLS, Haver Analytics, Apollo Chief Economist

Source: BLS, Haver Analytics, Apollo Chief Economist

Source: BLS, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

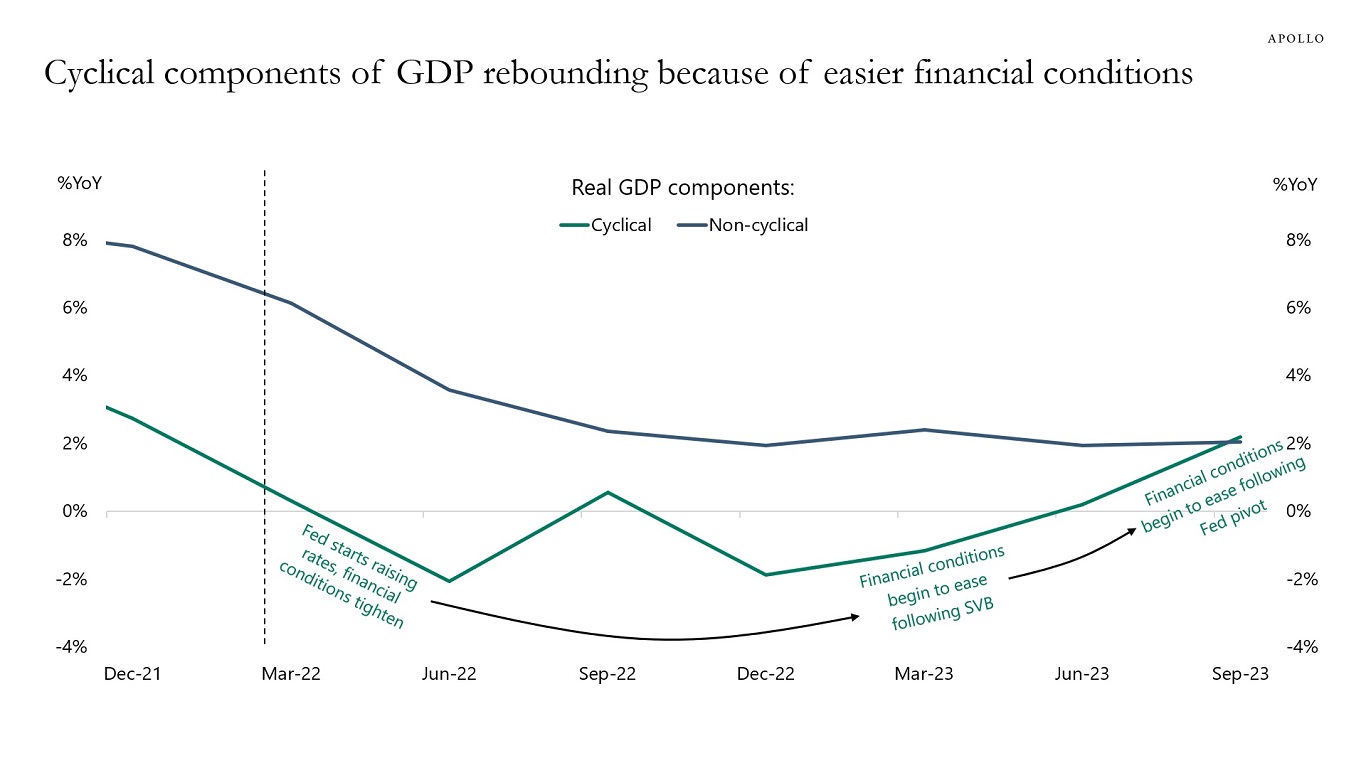

There is an ongoing debate about how core PCE inflation could come down from 5.5% to 3.2% without a slowdown in the economy, but this debate ignores that the cyclical components of GDP, including housing, have slowed sharply as a result of Fed hikes, and the non-cyclical components have continued to see strong growth in particular with strong post-Covid tailwinds to restaurants, hotels, and airlines.

The cyclical components of GDP are the interest rate-sensitive components such as housing, capex, and durable goods, and these parts of the economy slowed significantly when the Fed started raising rates, see chart below.

Put differently, it is misleading to say that Fed hikes have not had any negative impact on the economy. Fed hikes had a very negative effect on the interest rate-sensitive parts of the economy, most notably housing, and the result was a decline in housing inflation. With housing having a 40% weight in the CPI basket, the result was a decline in headline and core inflation for both CPI and PCE.

So why did the economy not slow down more, and why did Fed hikes not result in a rise in unemployment? There are two reasons.

First, the post-Covid economy saw surprising strength in the non-cyclical components of the economy, such as eating at restaurants, staying at hotels, and flying on airplanes, etc. Consumers wanted to travel, go to concerts and sporting events after Covid, and this has kept consumer spending strong.

Second, financial conditions eased significantly following SVB, and this boosted GDP growth to 4.9% in the third quarter of 2023. Similarly, the rally in the stock market, credit markets, and Treasury markets since October and after the Fed pivot in December have also eased financial conditions significantly, likely boosting the cyclical components of GDP over the coming months.

As the chart below shows, the bottom line is that the non-cyclical components continue to grow steadily because of post-Covid strong demand for consumer services, and the cyclical components are rebounding because of easier financial conditions.

The likely scenario is that the economy will reaccelerate over the coming months, which will put renewed upward pressure on inflation and, hence, bring back a more hawkish Fed.

In short, the Fed is not done fighting inflation, and, as a result, it is too early to argue that this is a soft landing because both the cyclical and non-cyclical components of GDP are likely to be solid over the coming months, see again the chart below.

Source: BEA, Haver Analytics, Apollo Chief Economist. Note: Cyclical components include interest-sensitive components, i.e., durable goods consumption, nonresidential structures, equipment investment, and residential investment. Non-cyclical components include non-durable goods consumption, services consumption, and nonresidential investment in intellectual property products. See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.