Want it delivered daily to your inbox?

-

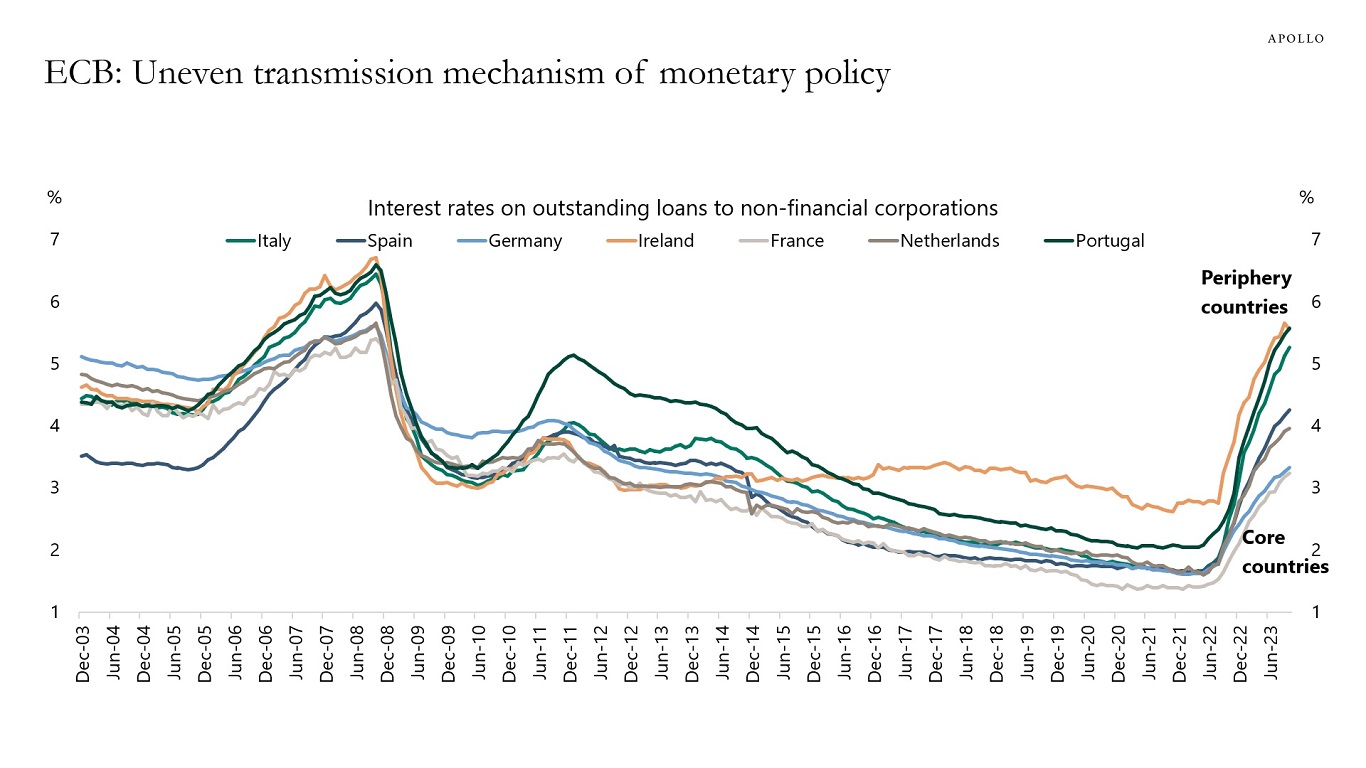

Data from the ECB shows that ECB rate hikes have had a very uneven impact on euro area countries with interest rates for firms increasing much more in periphery countries than in core countries.

For example, interest rates on outstanding loans to non-financial corporations in Ireland and Portugal are currently around 5.6% versus 3.3% in Germany and France, see chart below.

The bottom line is that ECB rate hikes negatively impact the periphery more than the core.

Source: ECB, Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

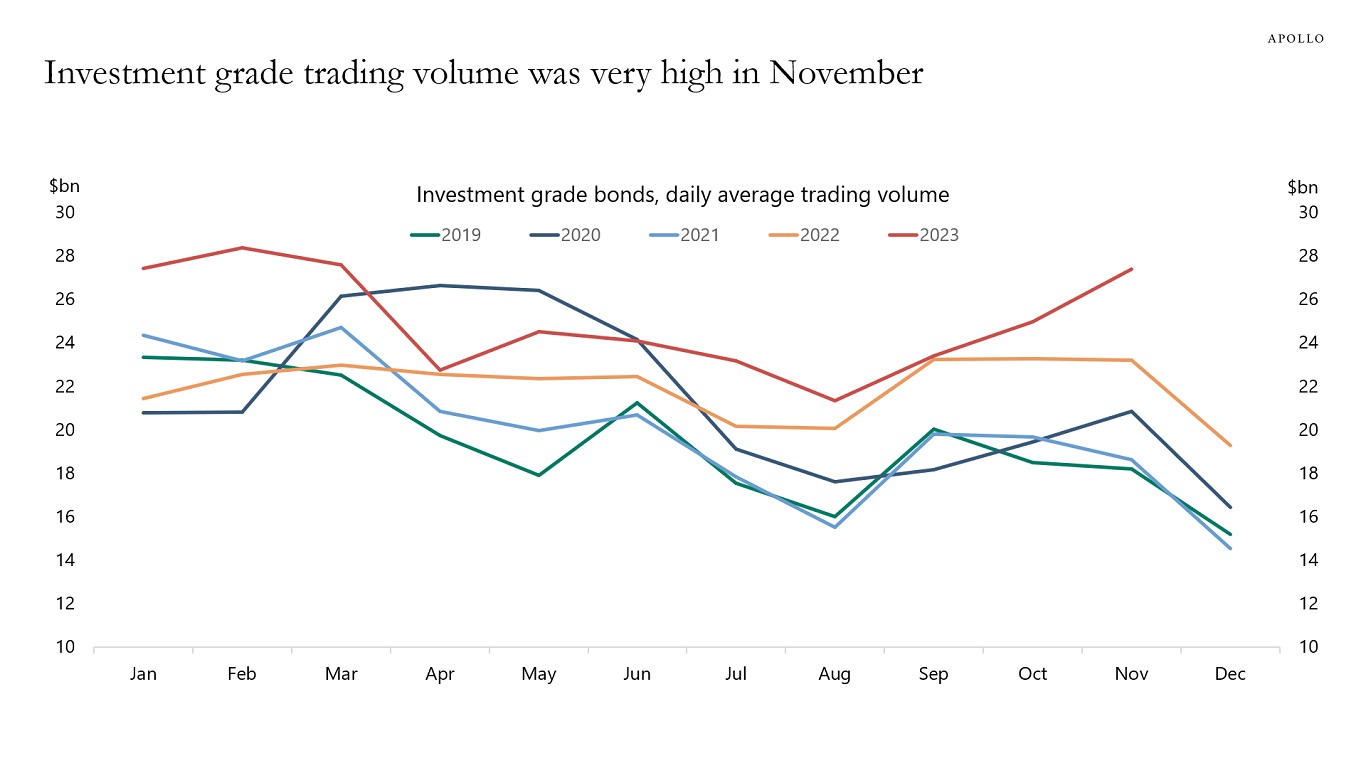

Trading volume in investment grade bonds was at post-Covid highs in November and significantly above 2019 levels, see chart below.

Source: FINRA TRACE, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

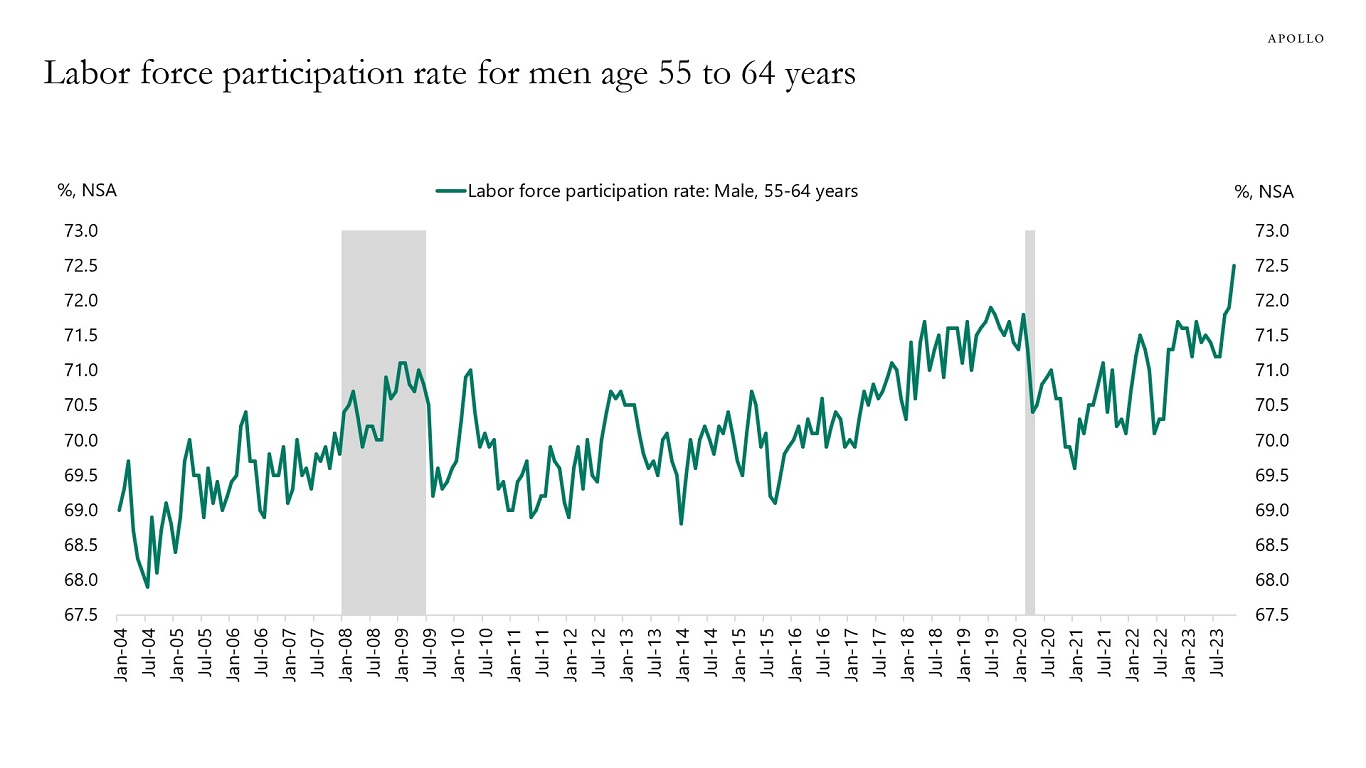

In recent months, we have seen a significant increase in the number of men age 55 to 64 joining the workforce, see chart below.

Source: BLS, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

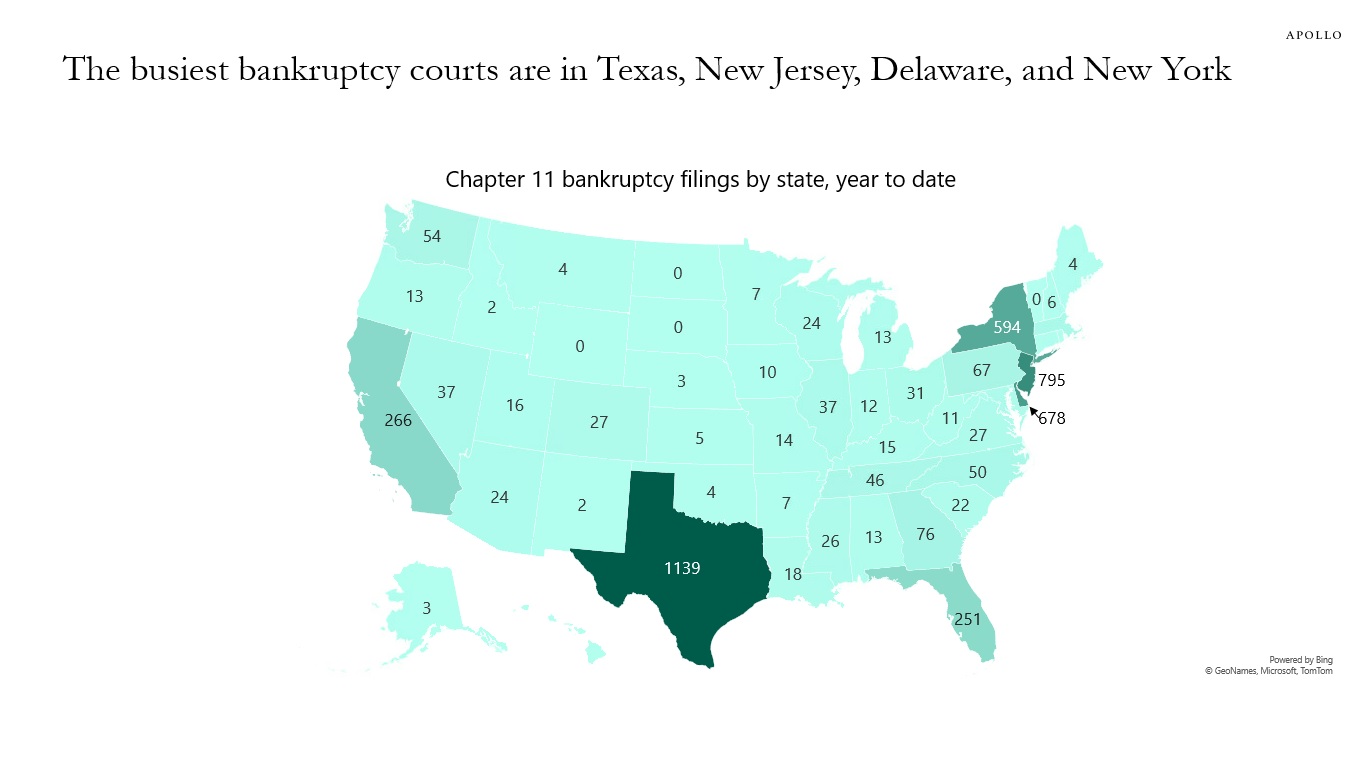

There are more Chapter 11 bankruptcy filings in Texas, New Jersey, Delaware, and New York than in other states, see map below.

Source: Epiq bankruptcy, Apollo Chief Economist. Data from January 1, 2023 to December 8, 2023. See important disclaimers at the bottom of the page.

-

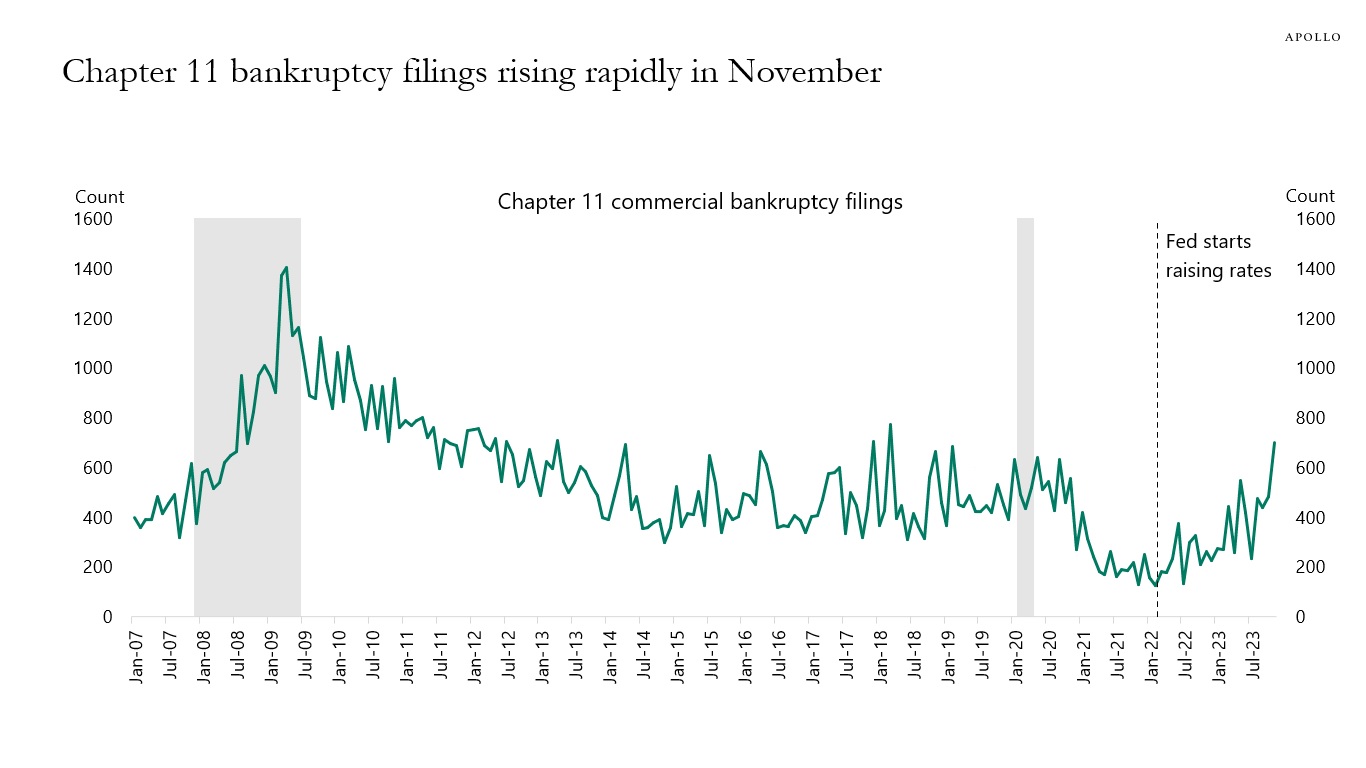

Data for November shows that Chapter 11 bankruptcy filings are trending higher, and Fed hikes continue to bite harder and harder on highly leveraged firms with little or no cash flows in tech, growth, and venture capital, see chart below.

Source: Epiq bankruptcy, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

This chart book looks at recent developments in private equity, PE deal activity, private credit, real assets, secondaries, middle markets, and venture capital.

See important disclaimers at the bottom of the page.

-

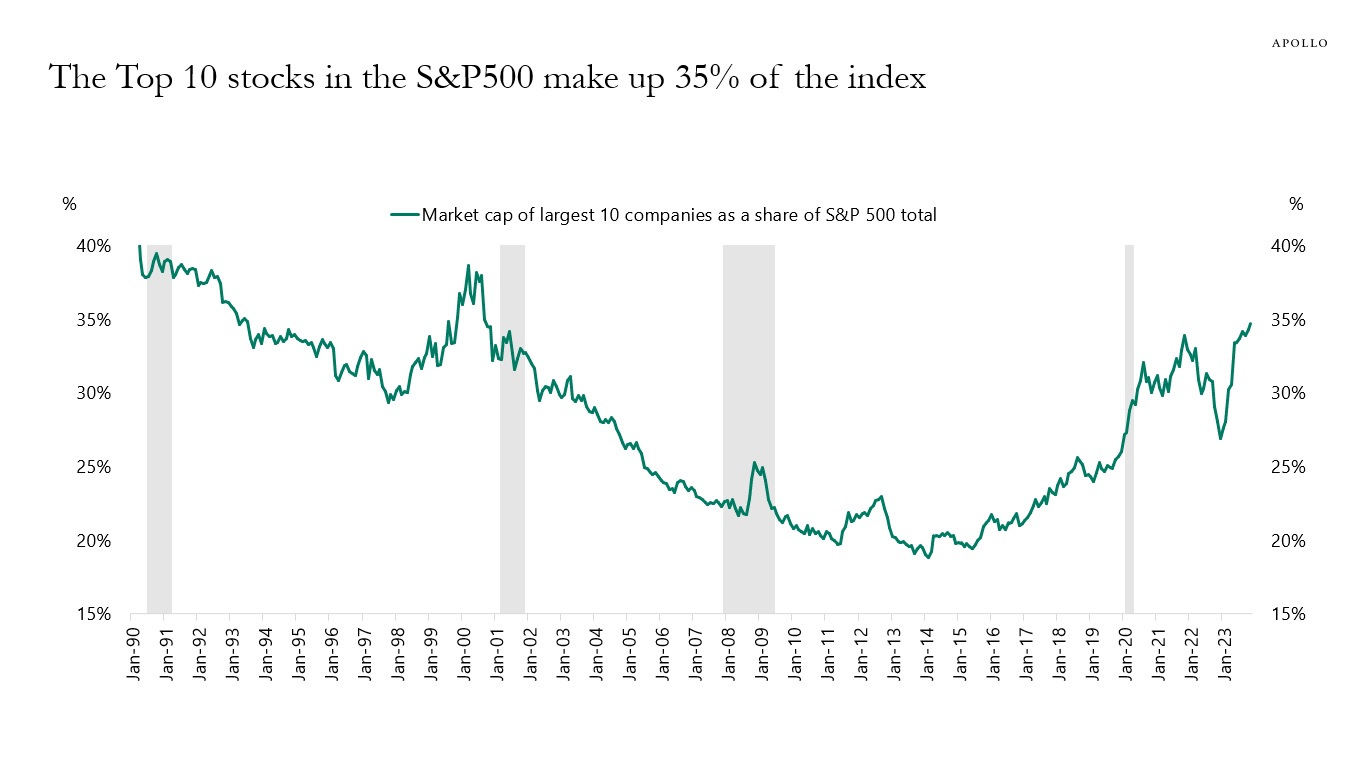

The concentration in the S&P500 continues to increase, and the ten largest stocks now make up 35% of the index, the highest level since the last tech bubble in 2000, see chart below.

Source: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

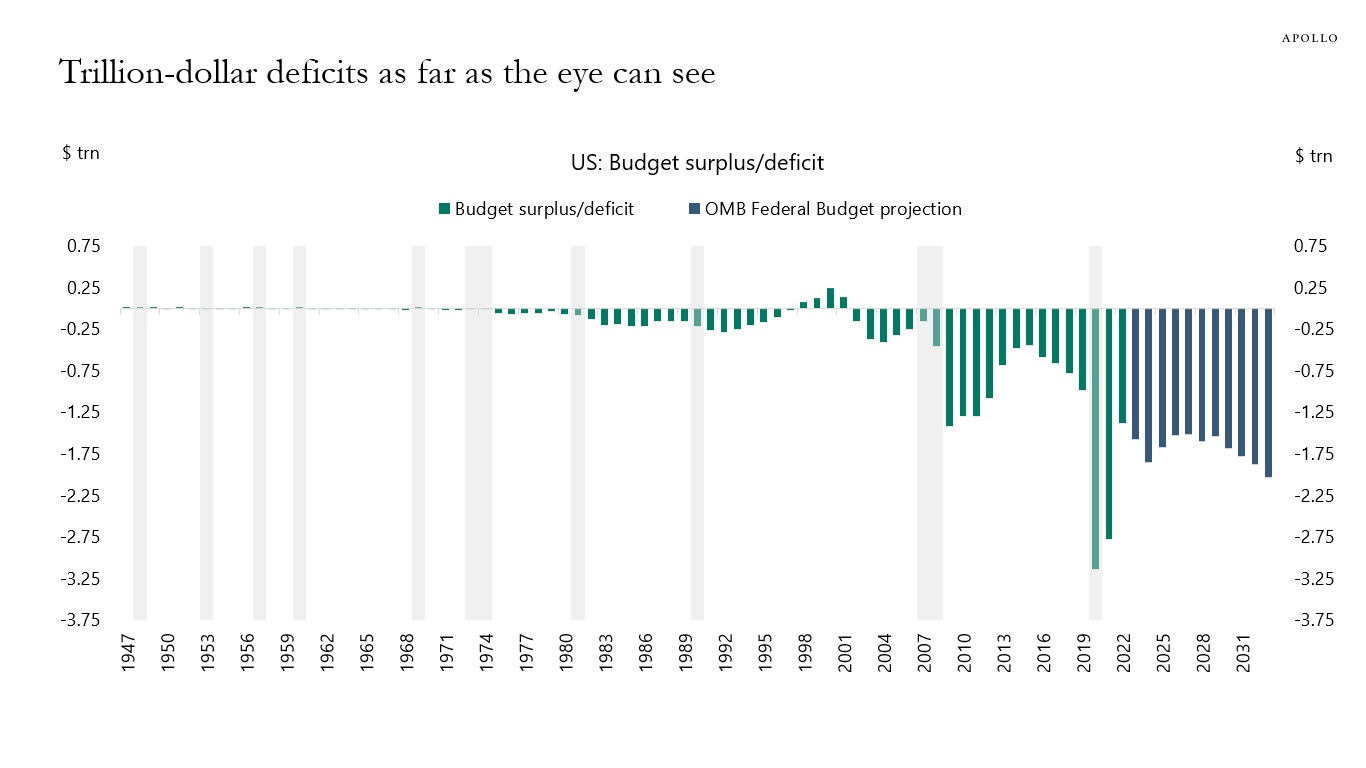

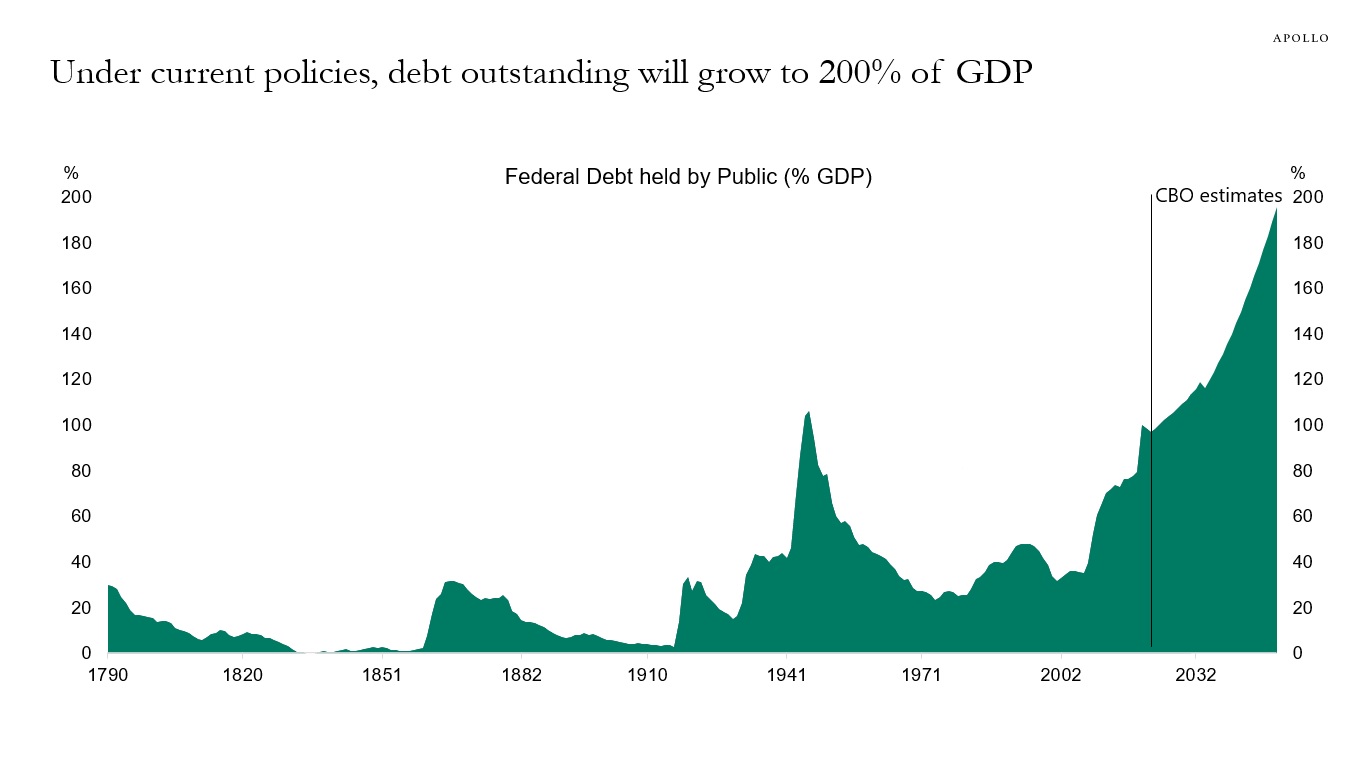

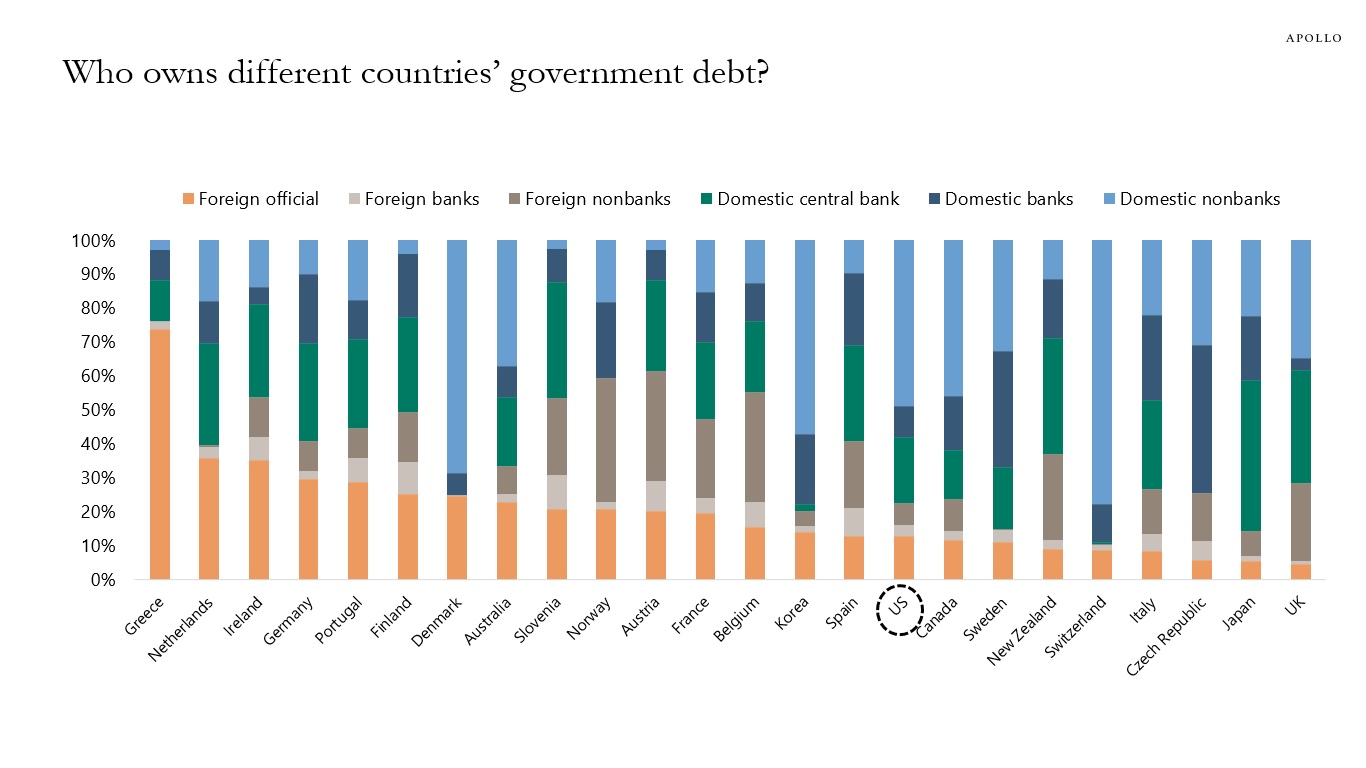

With long rates falling in recent weeks, Treasury supply has seemingly become less important as a driver of long rates.

But the fiscal challenges have not disappeared.

Next week, we have a 10-year auction on Monday and a 30-year auction on Tuesday. And looking into 2024, Treasury auction sizes will be, on average, 23% higher than in 2023.

Because of the constant rise in government debt levels, investors need to monitor not only Treasury auctions but also rating agencies and the term premium.

In this short presentation is a collection of relevant data for thinking about the US fiscal situation and the likely transmission channels to financial markets.

Source: OMB, Haver Analytics, Apollo Chief Economist

Source: CBO, Haver Analytics, Apollo Chief Economist

Source: The IMF, Apollo Chief Economist. Note: Data as of year-end 2022. See important disclaimers at the bottom of the page.

-

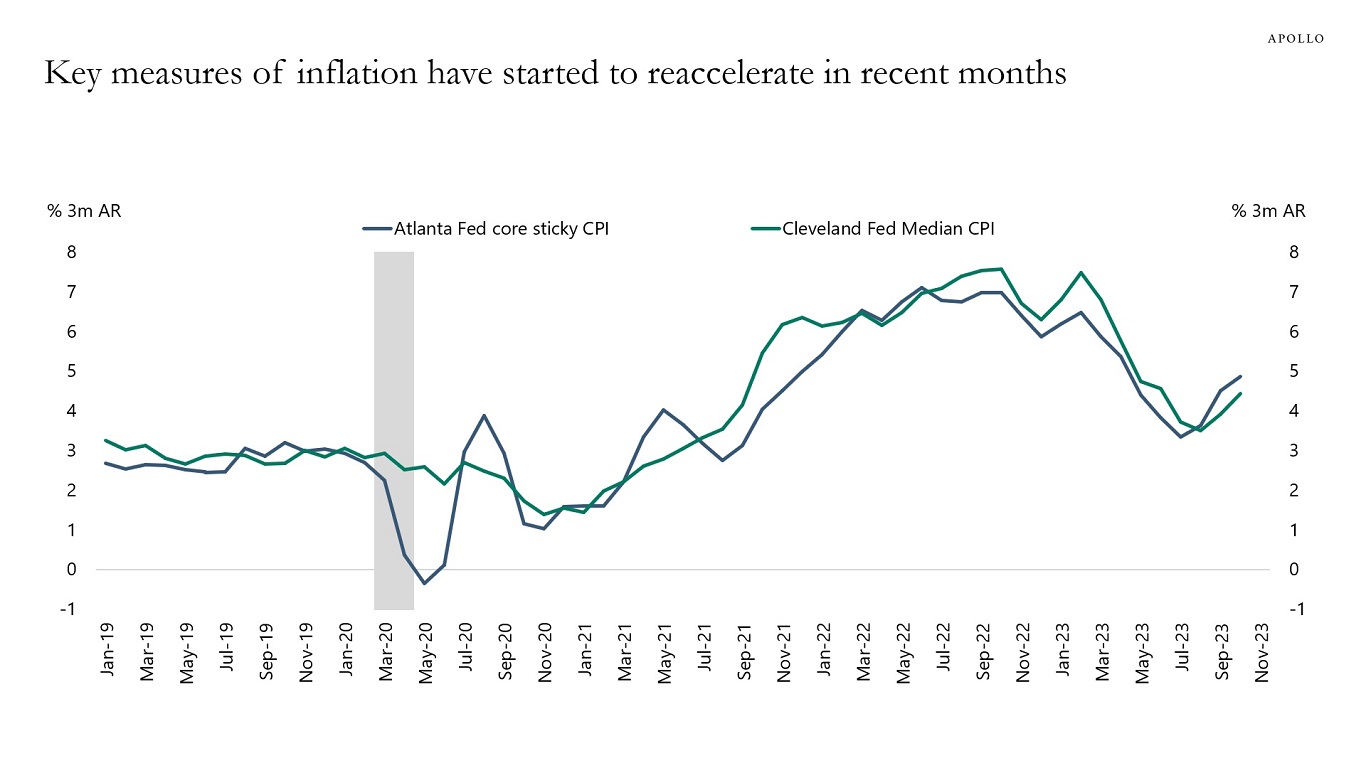

Measures of underlying inflation have started to reaccelerate in recent months, and this is a problem for the Fed, see chart below.

The Fed cannot and will not turn dovish as long as inflation remains significantly above the FOMC’s 2% inflation target, particularly when underlying inflation is trending higher.

The consequences are that delinquency rates on credit cards and auto loans will continue to increase, corporate default rates will continue to move higher, and bank lending will continue to trend lower.

In other words, we are entering a period with weaker economic data where the Fed will stay on hold.

Source: FRB of Atlanta, FRB of Cleveland, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

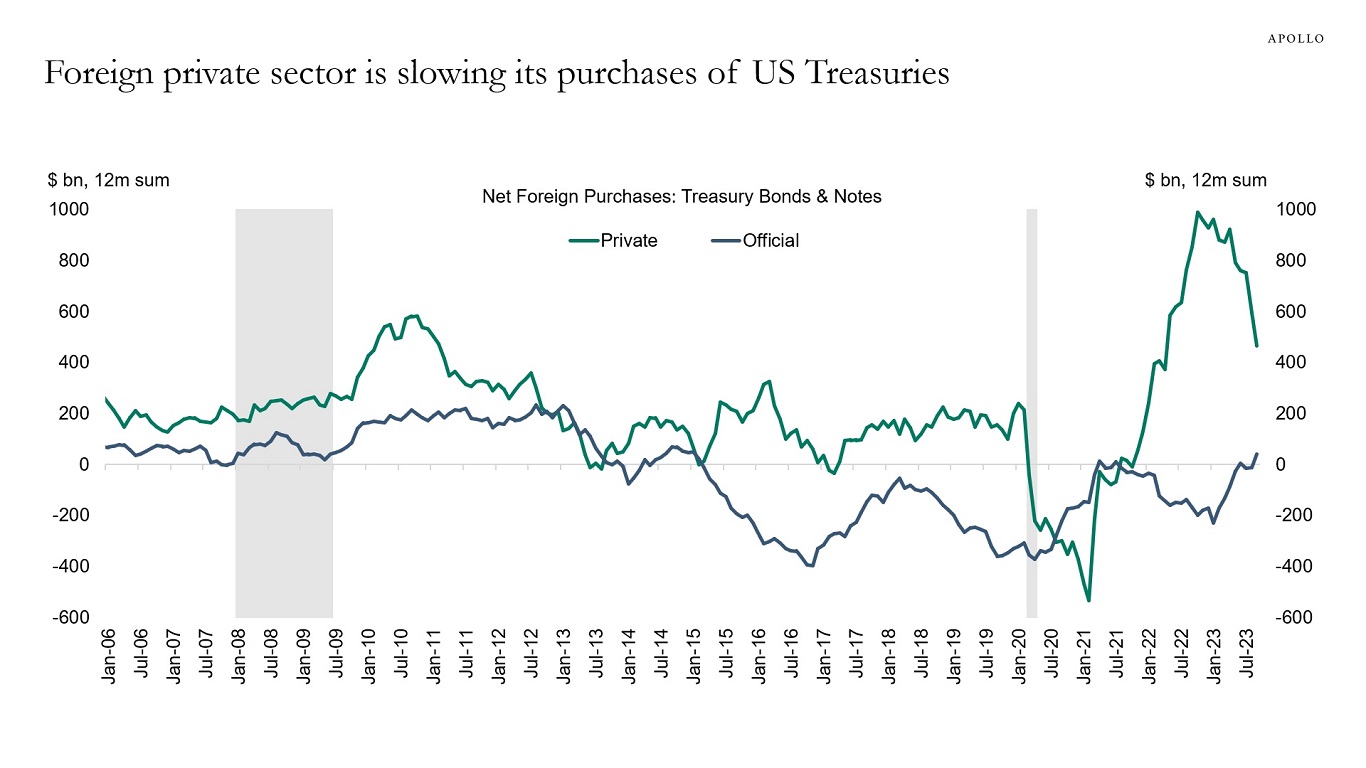

Since the Fed started raising rates, the biggest foreign buyer of US Treasury bonds has been the yield-sensitive private sector, see the first chart below.

But with rates peaking, the foreign private sector has been slowing purchases, see chart below.

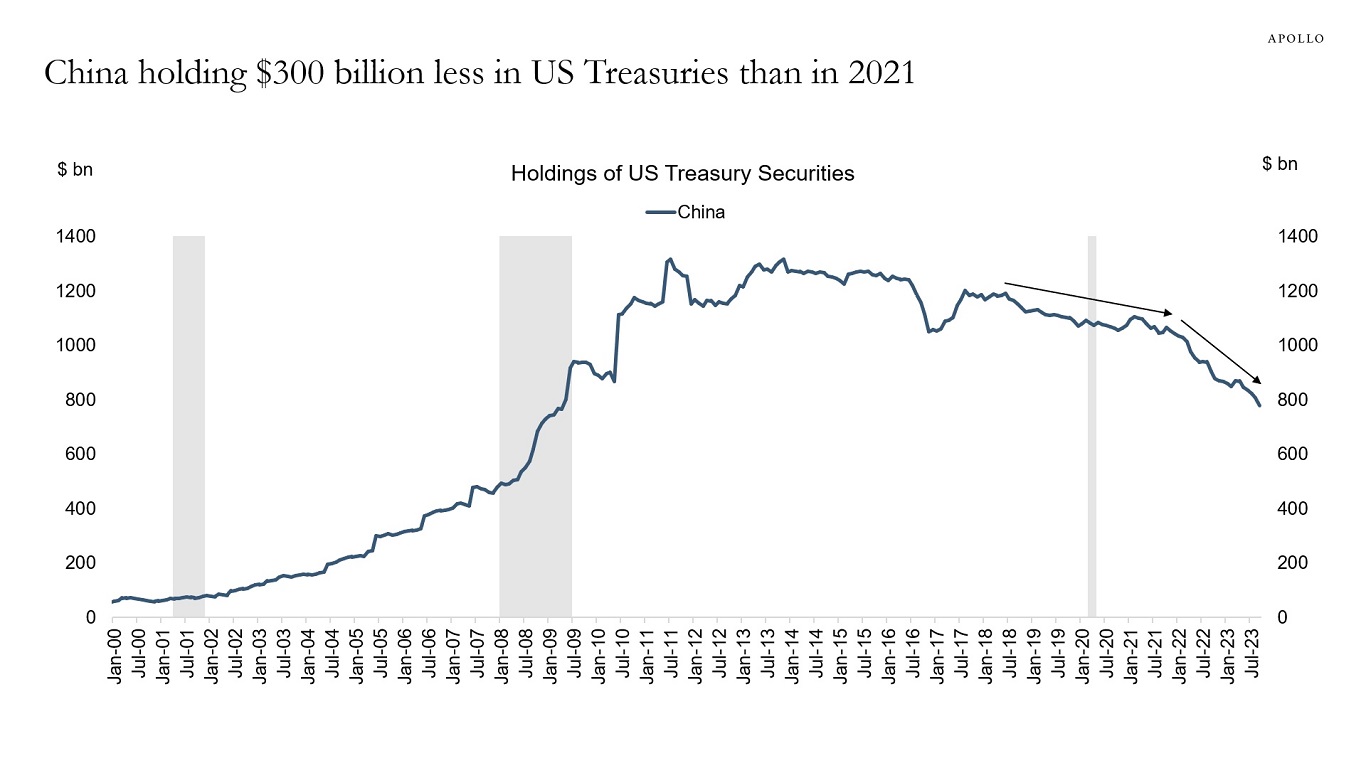

The foreign official sector has been a net seller during this rate cycle. This is also the case for China, where holdings of US Treasuries have declined by $300 billion since 2021, see the second chart below.

With growth slowing in China due to demographic headwinds, slowing exports, and a deflating housing market, demand for US Treasuries from the foreign official sector will likely remain weak.

Our 2024 outlook for China is available here.

Source: Treasury, Haver Analytics, Apollo Chief Economist

Source: Bloomberg, Apollo Chief Economist

See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.