Want it delivered daily to your inbox?

-

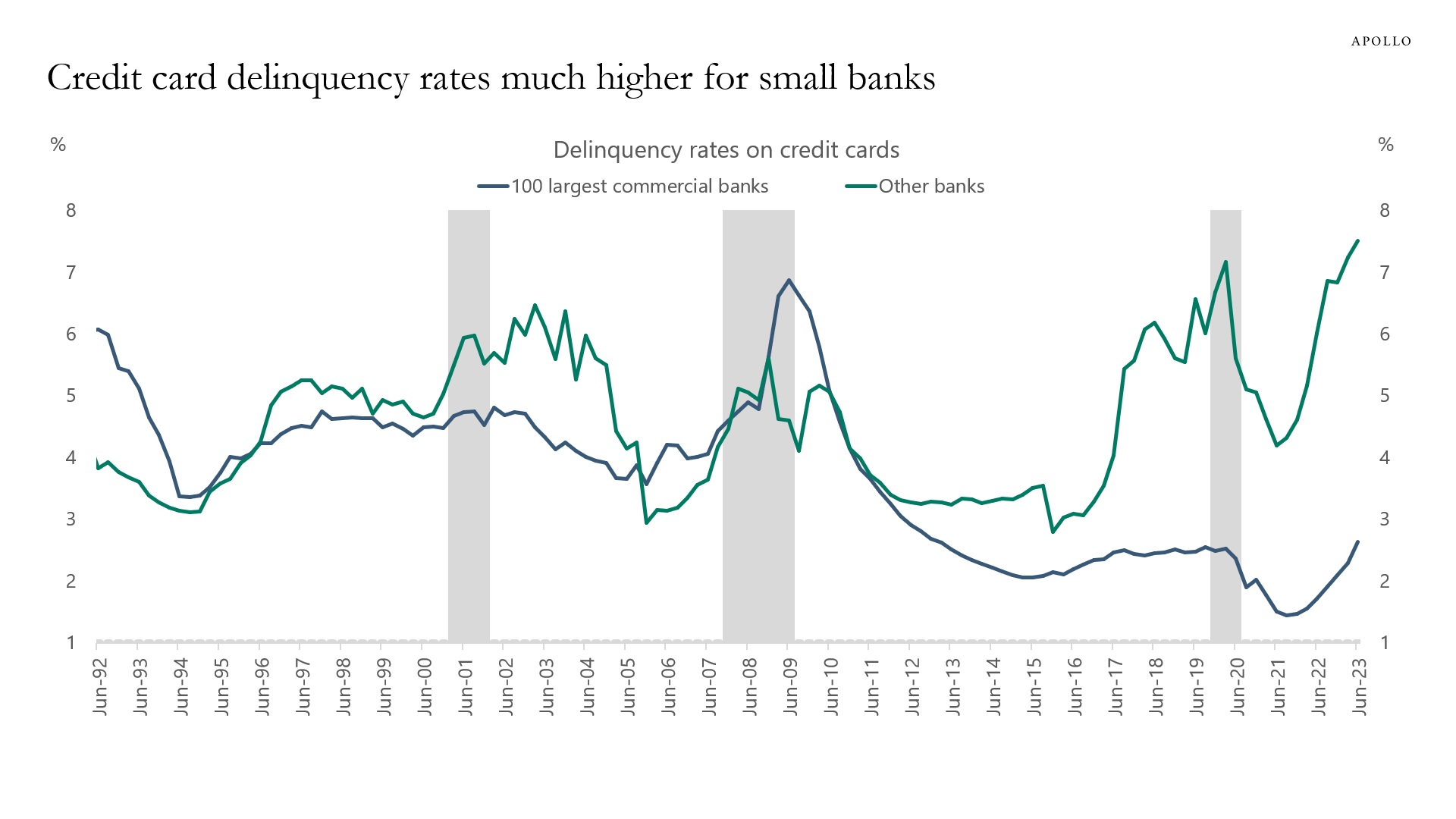

Despite the unemployment rate being at the lowest level in 50 years, credit card delinquency rates at small banks are at the highest level on record, see chart below. Imagine where these lines will be once the labor market finally begins to soften.

Source: FRB, Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

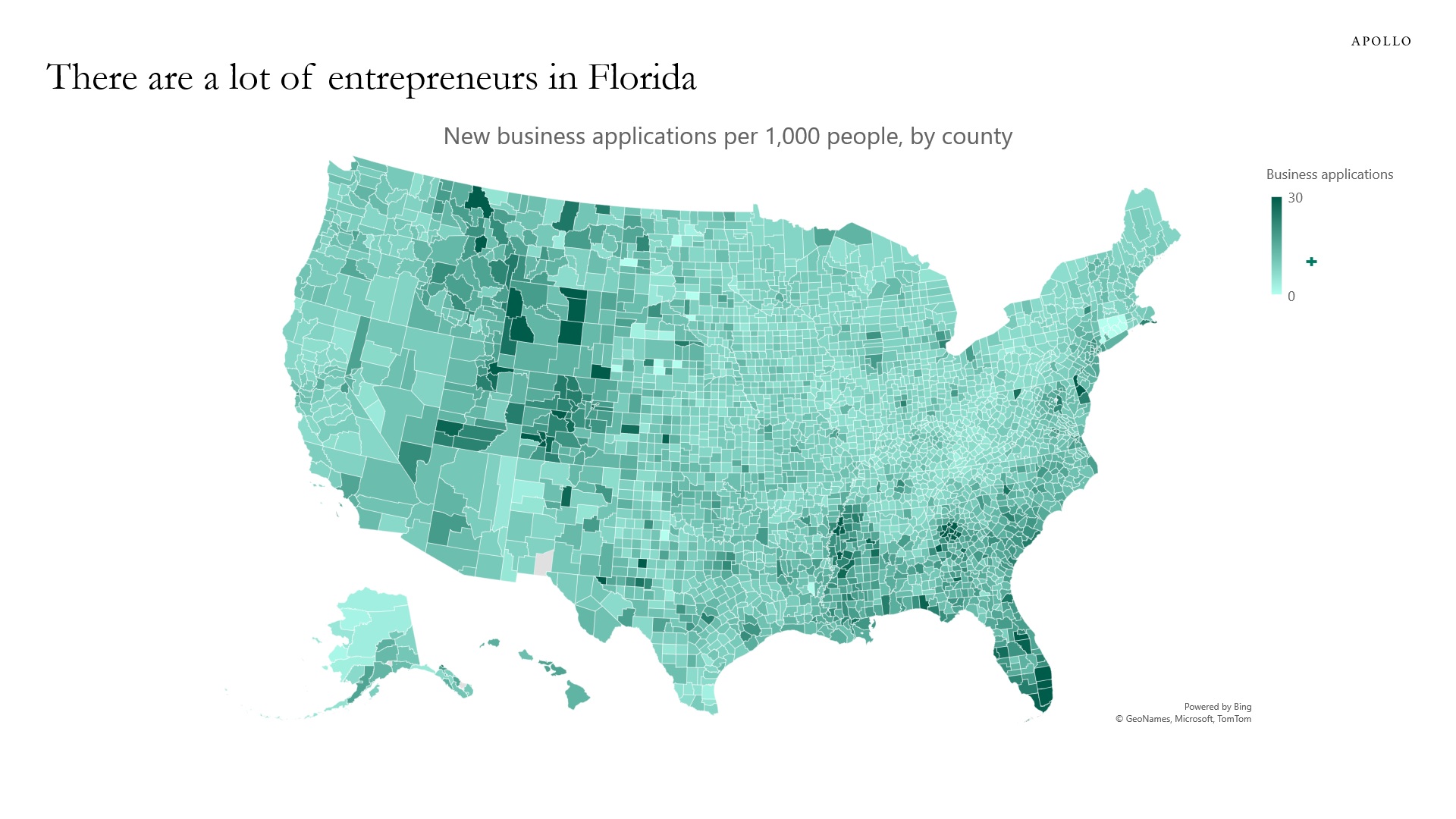

The map below shows the number of new business applications per 1,000 residents, and there are a lot of entrepreneurs in the Southeast, in particular in Florida.

Source: Census Bureau, Apollo Chief Economist. Note: Data for 2022. See important disclaimers at the bottom of the page.

-

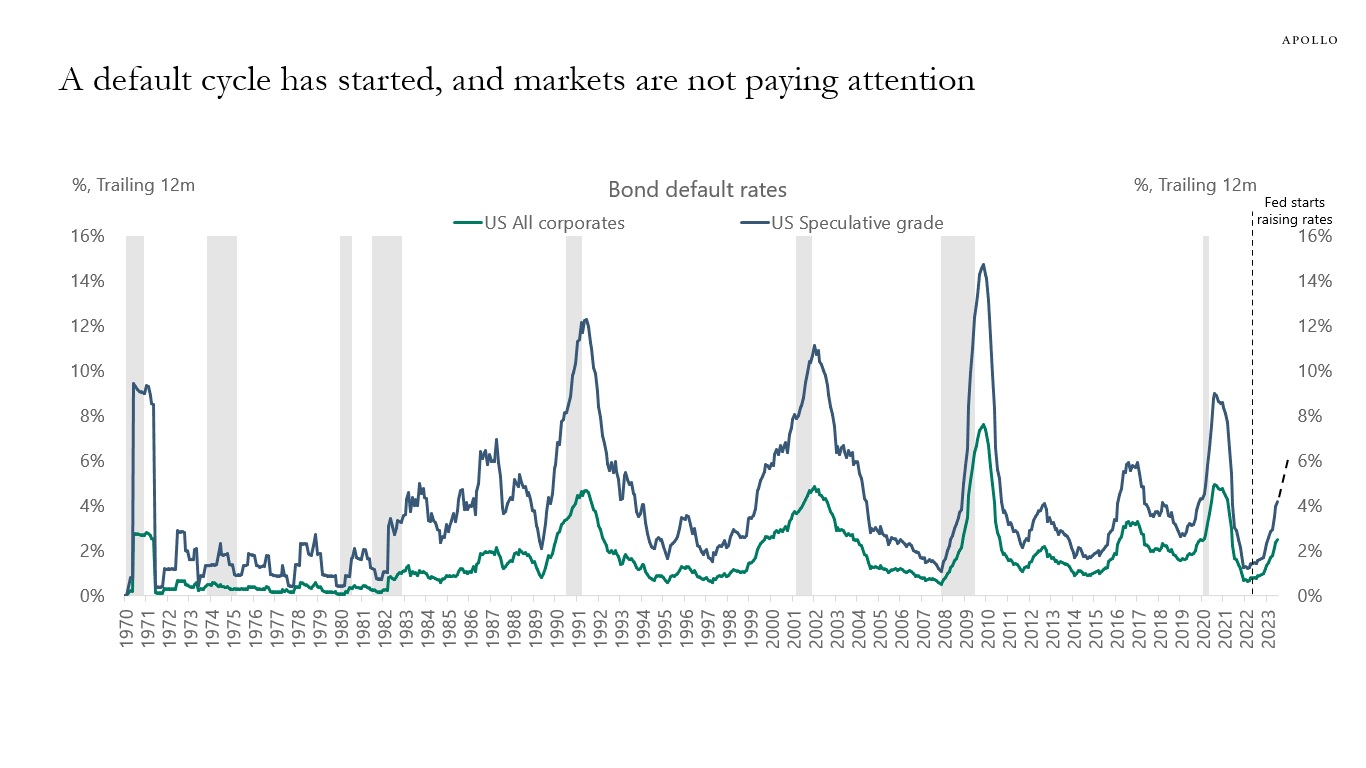

Since the Fed started hiking in March 2022, default rates have been moving higher, and every day there are companies that cannot get a new loan or refinance an existing loan.

This is how monetary policy works. A higher cost of capital makes it harder for firms to get financing.

With the strong uptrend in defaults over the past six months, and the Fed keeping interest rates at elevated levels, the HY default rate could reach 6% by the end of 2023, see chart below.

The bottom line is that a default cycle has started, and markets are not paying attention.

Source: Moody’s Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

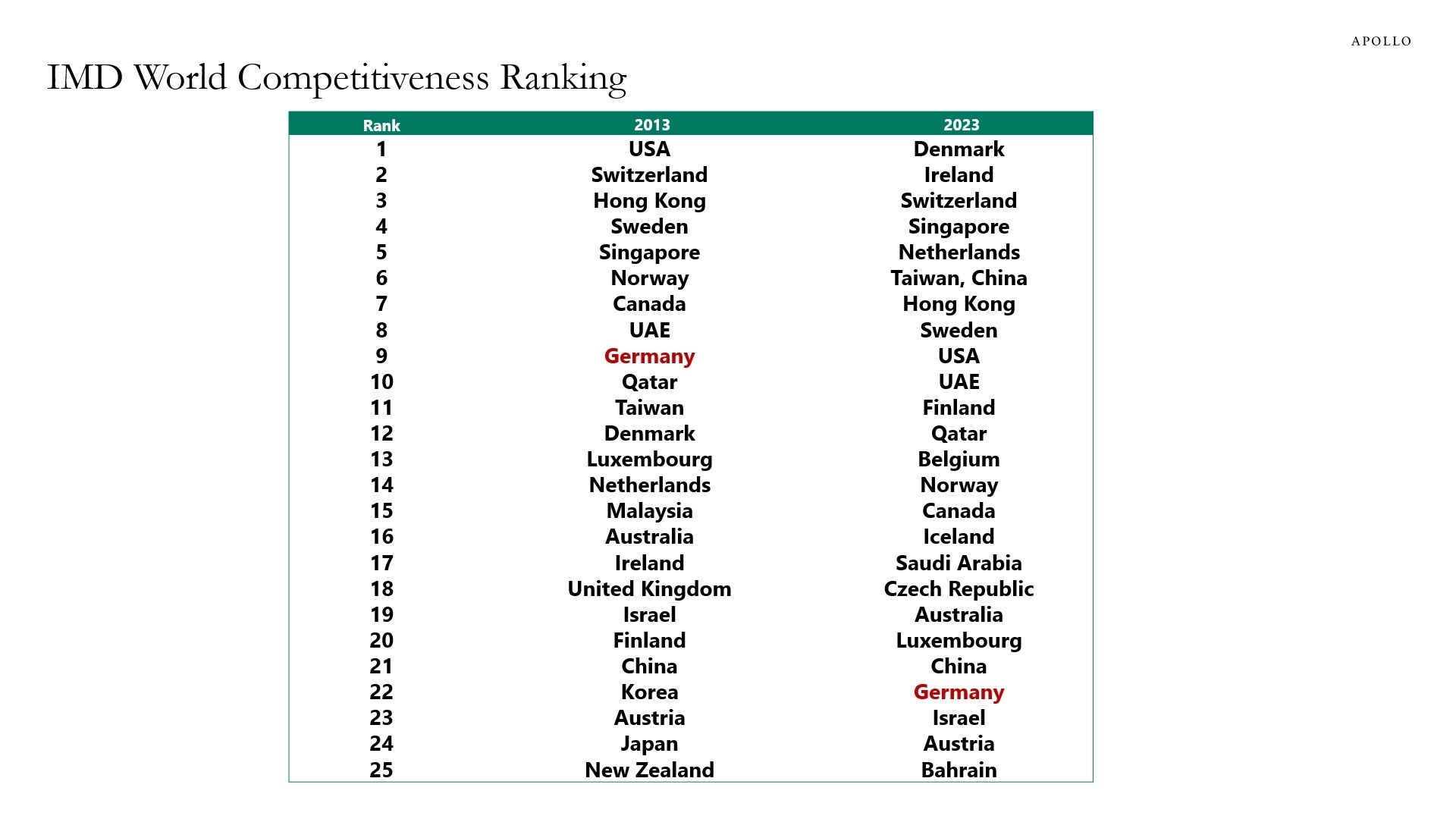

The IMD every year ranks the competitiveness of countries by comparing indicators for Infrastructure, Business Efficiency, Government Efficiency, and Economic Performance, see table below.

Over the past decade, Germany has moved from being the ninth most competitive economy in the world to currently number 22. The current rankings for Germany across the four categories are: Infrastructure (14), Business Efficiency (29), Government Efficiency (27), and Economic Performance (12).

Source: IMD, Apollo Chief Economist. Note: The IMD World Competitiveness Ranking is based on 336 indicators under four categories: Infrastructure, Business Efficiency, Government Efficiency, and Economic Performance. See important disclaimers at the bottom of the page.

-

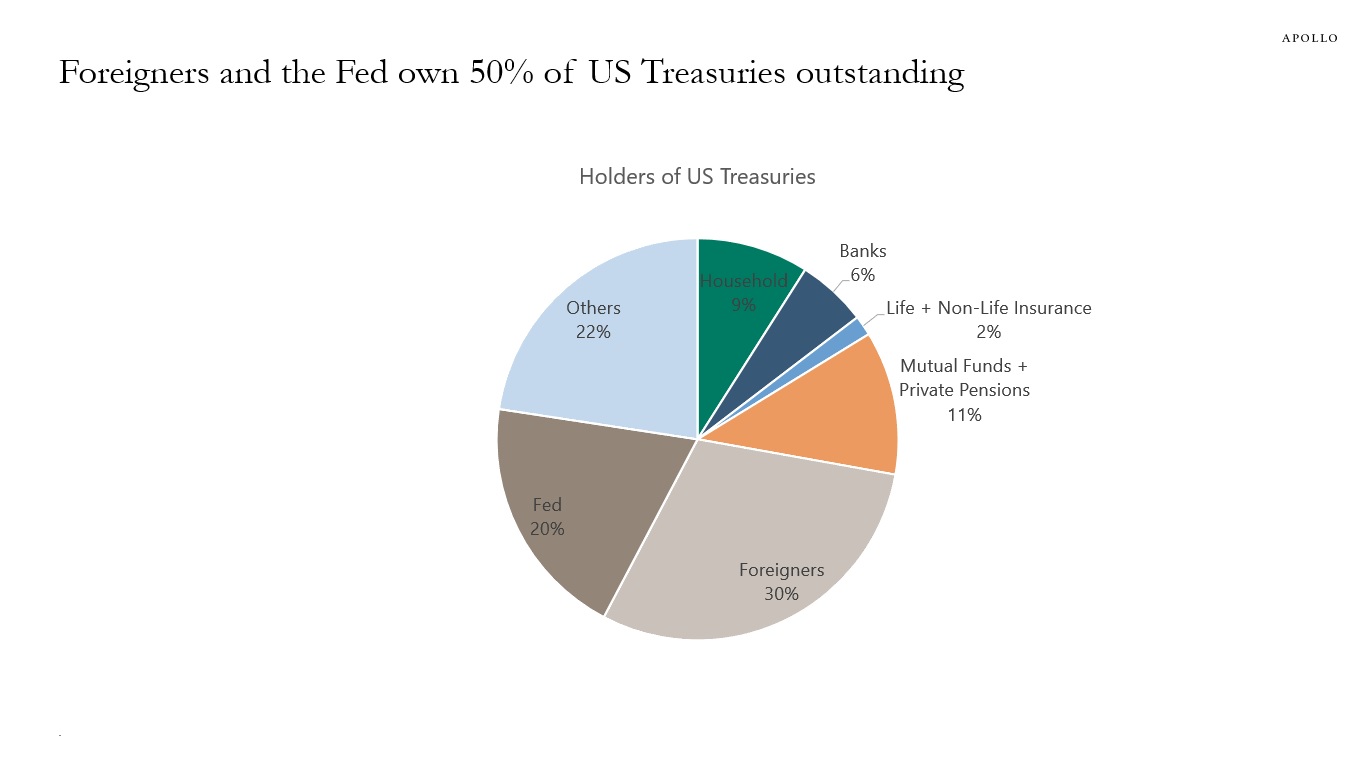

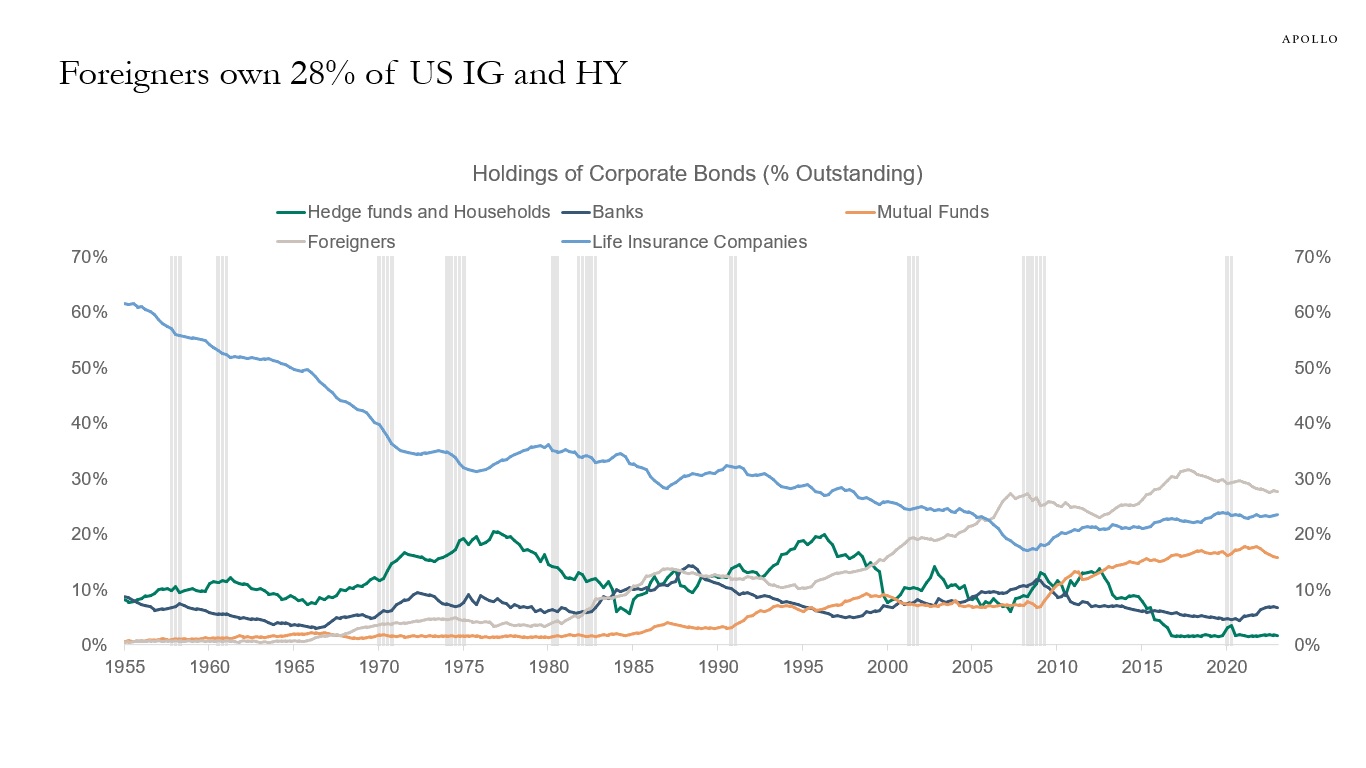

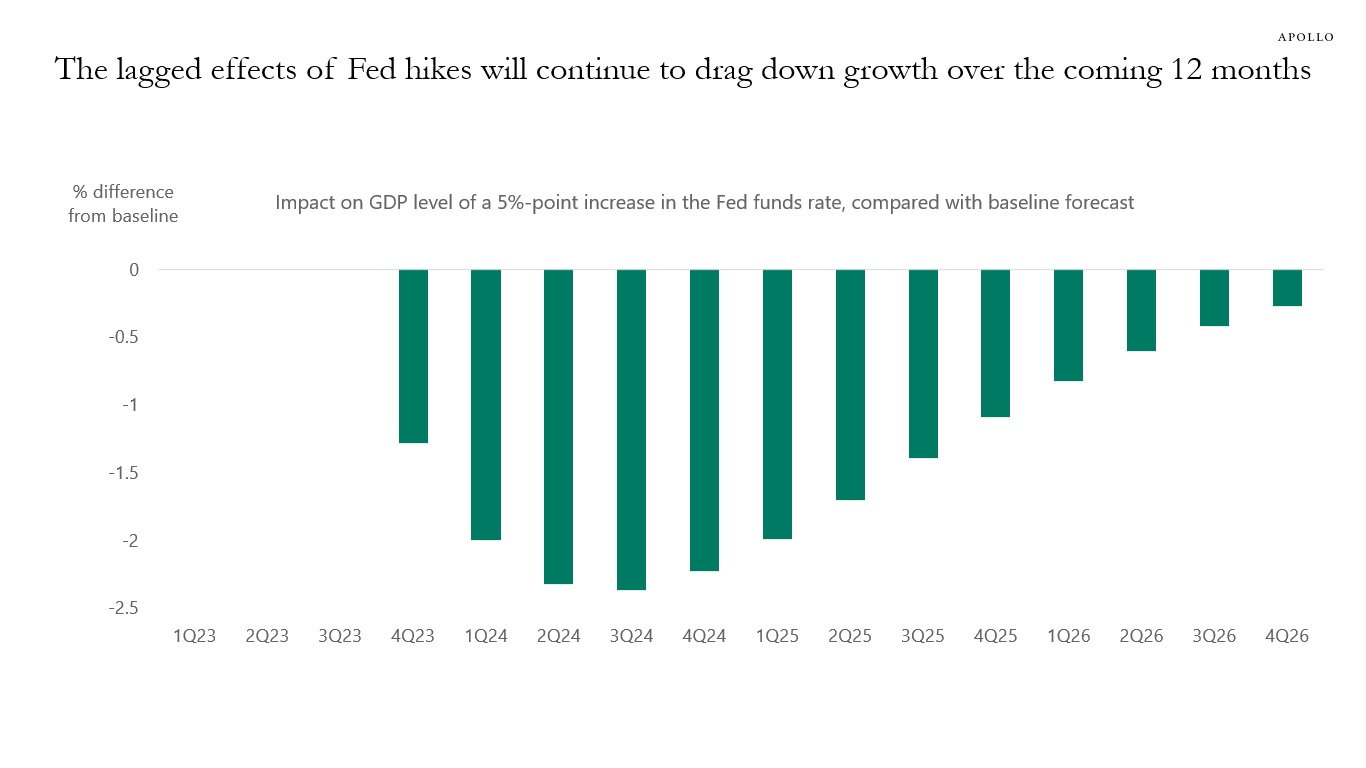

When interest rates increase, holders of fixed income get a higher cash flow. The problem is that the Fed and foreigners own 50% of Treasuries outstanding, and foreigners own 28% of IG and HY credit outstanding, so a lot of the additional cash flow created by higher US yields is not boosting US GDP growth.

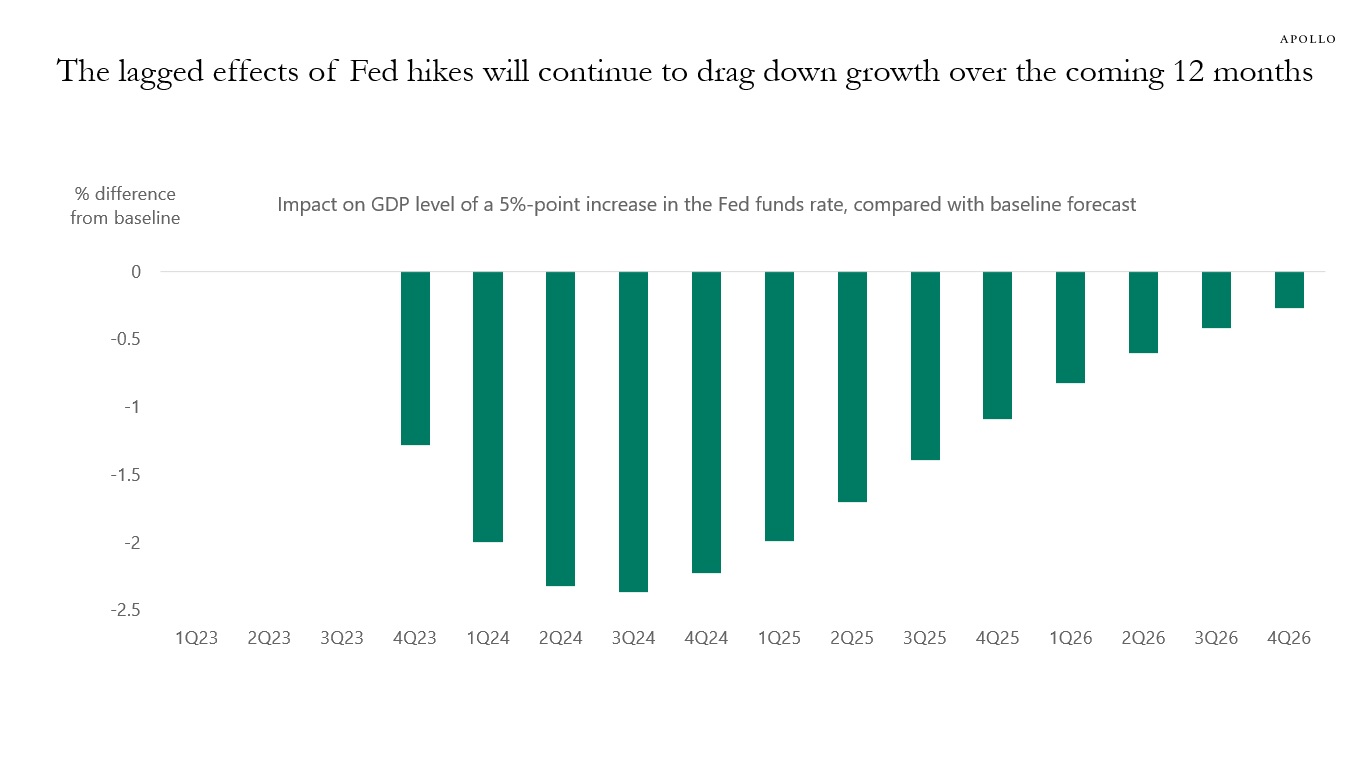

The bottom line is that higher interest rates are a net negative for the US economy, see also the third chart, which shows the effects on US GDP as a result of raising the Fed funds rate 5%-points using a model similar to the Fed’s FRB/US model of the US economy.

Source: FRB, Haver Analytics, Apollo Chief Economist. “Others” include nonfinancial businesses, state and local governments, and federal government retirement funds.

Source: FFUNDS, Haver, Apollo Chief Economist

Source: Bloomberg, Apollo Chief Economist. Note: 500bps monetary policy shock in 3Q23. See important disclaimers at the bottom of the page.

-

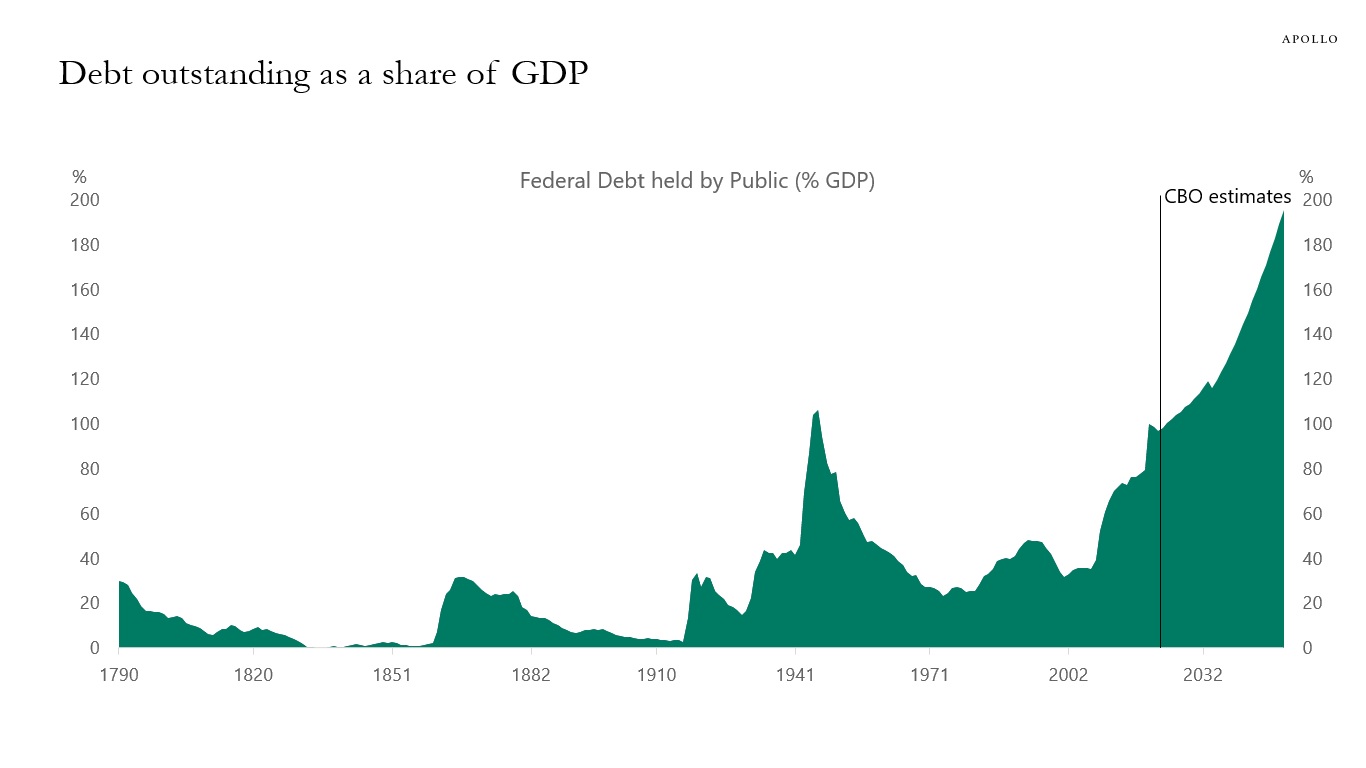

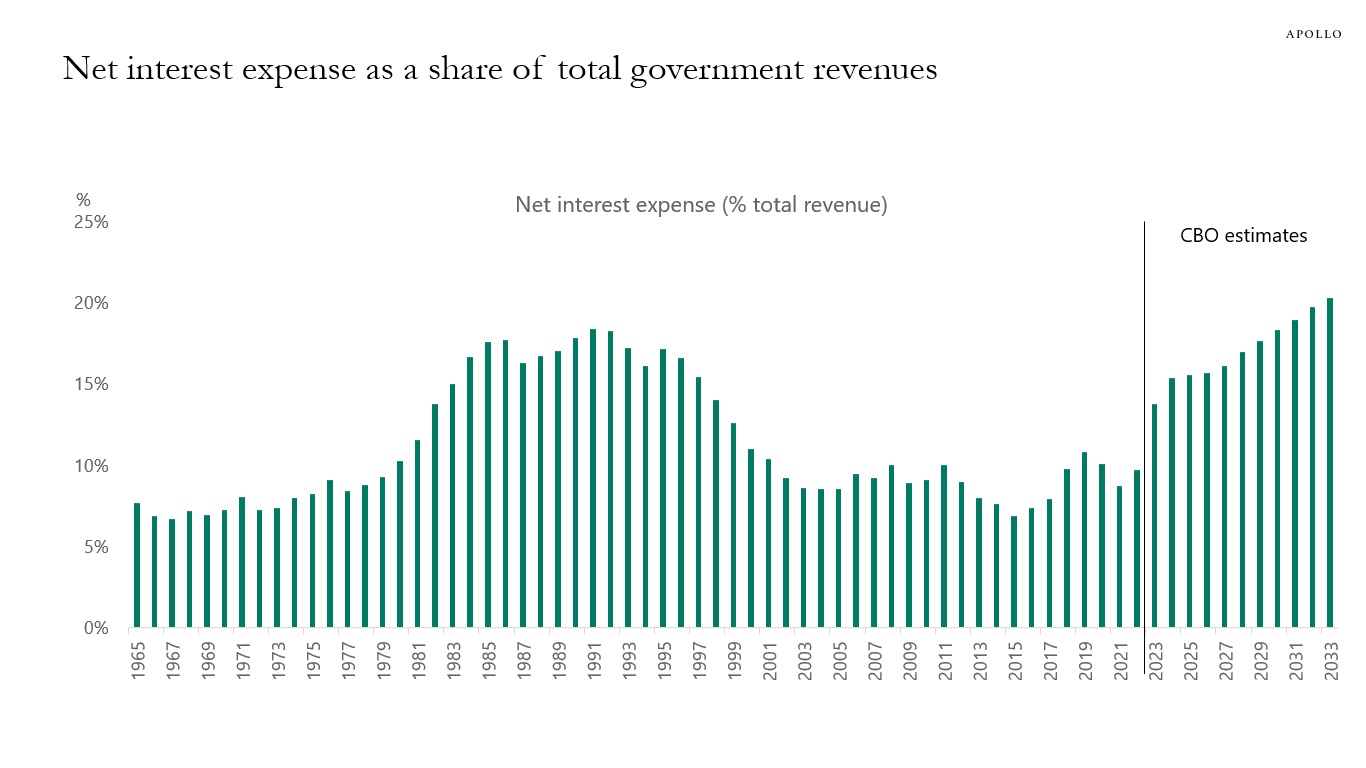

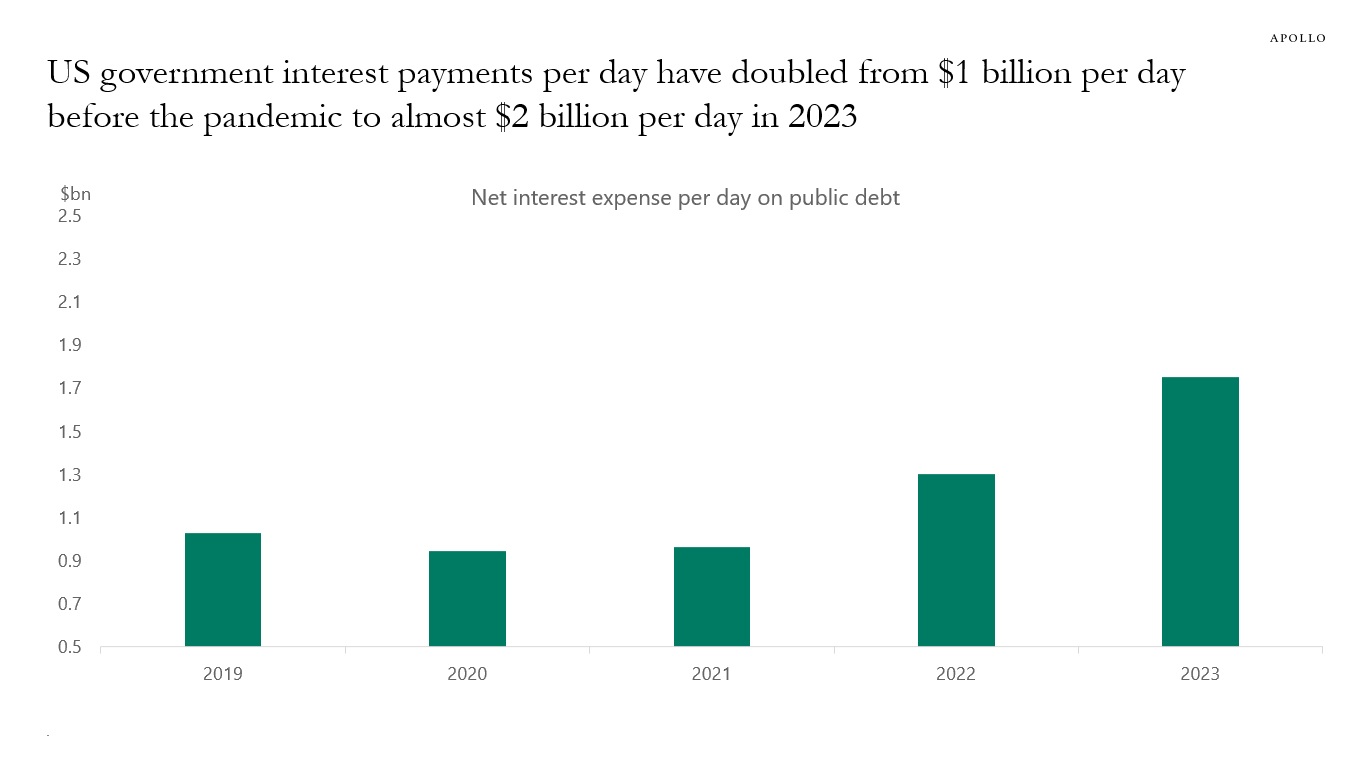

Interest rates are rising, the annual debt servicing cost of the US government is close to $1 trillion, and the net interest expense as a share of total government revenues is near all-time high levels, see charts below.

The implication for markets is that higher rates are not only slowing down consumers and corporates through higher borrowing costs. Higher rates are also a drag on growth through higher debt servicing costs for the government. In other words, higher debt servicing costs are impacting not only consumers and corporates but also the government.

The bottom line is that when government debt levels are high, it is more difficult for interest rates to stay elevated for a long time because the negative impact on the economy of higher rates is also working through higher debt servicing costs for the government.

Source: CBO, Haver Analytics, Apollo Chief Economist

Source: Treasury, Haver Analytics, Apollo Chief Economist. Note: Estimated monthly cost is calculated as average interest rate total outstanding in marketable and non-marketable debt and includes public debt and intragovernmental holdings.

Source: CBO, Haver Analytics, Apollo Chief Economist

Source: CBO, Haver Analytics, Apollo Chief Economist. Note: Interest rate assumptions by CBO: 2.1% in 2022 and 2.7% in 2023. Annual CBO data divided by 365. See important disclaimers at the bottom of the page.

-

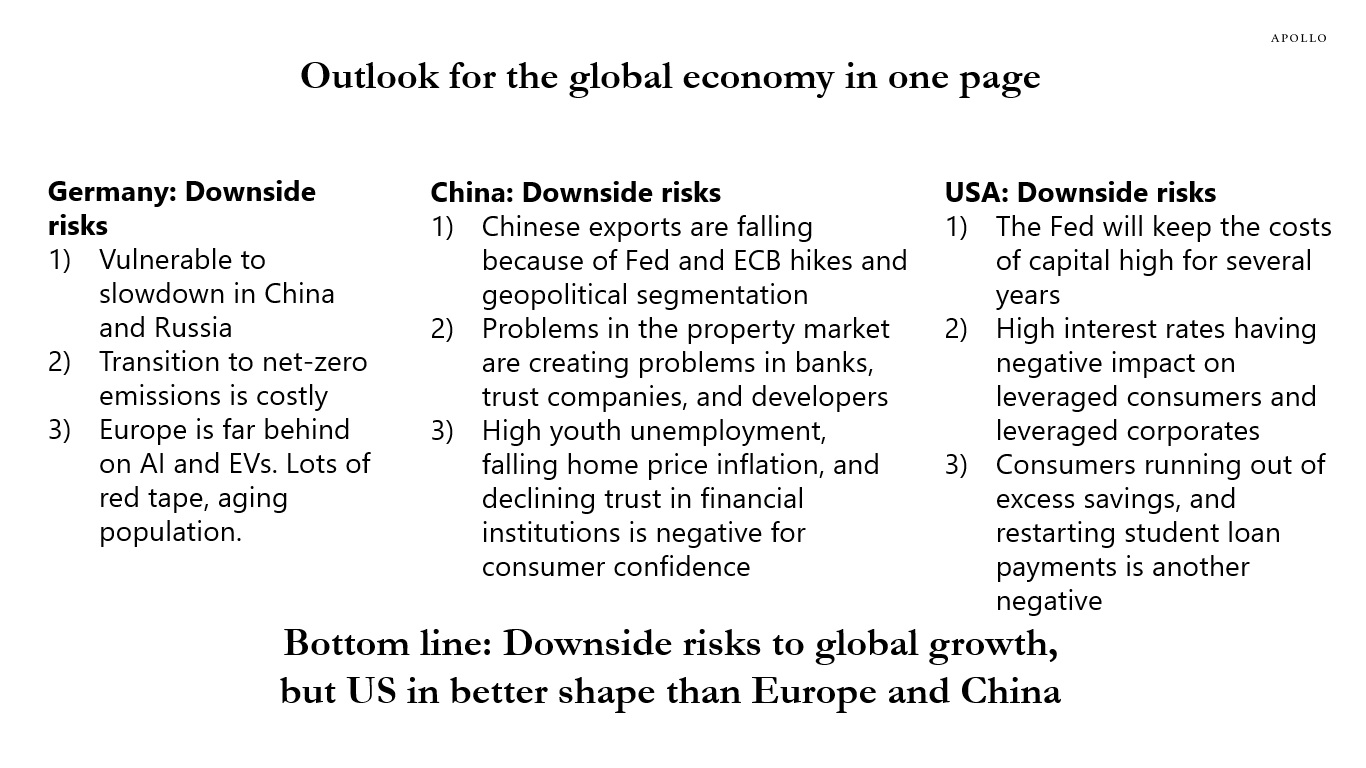

The list of downside risks to the global economy keeps growing, see overview below.

Source: Apollo Chief Economist See important disclaimers at the bottom of the page.

-

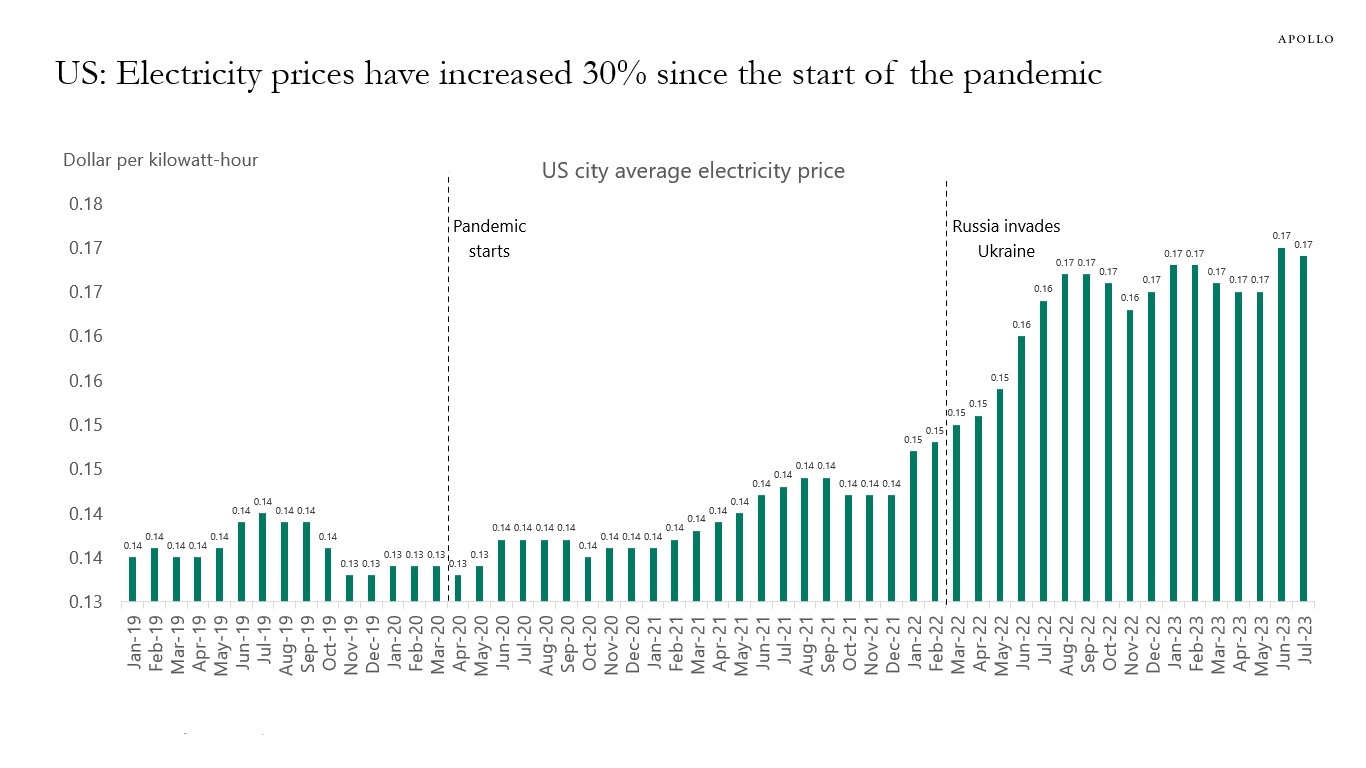

Electricity prices for households are up 30% since the pandemic started, see chart below.

Source: FRB of St. Louis, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

The FOMC started raising rates 16 months ago, and there are two different explanations for why Fed hikes have not yet slowed down the economy in a meaningful way:

1) The Fed has not raised interest rates enough.

2) The lagged effects of Fed hikes take longer than we think.

The Fed does not know if the continued strength in the economic data is because it has not raised rates enough or if the lagged effects of Fed hikes take longer than usual. As a result, the FOMC’s approach is to keep interest rates elevated until the economy starts slowing down. Against this backdrop, a soft landing is not an option because the Fed will keep interest rates high until they get the economic slowdown required for them to turn dovish.

Even if inflation comes down and growth is still strong, the Fed will continue to be hawkish because of worries about strong growth causing a re-acceleration in inflation. The implication for markets is that a recession is a pre-condition for the Fed to stop being hawkish.

Source: Bloomberg, Apollo Chief Economist. Note: 500bps monetary policy shock in 3Q23. See important disclaimers at the bottom of the page.

-

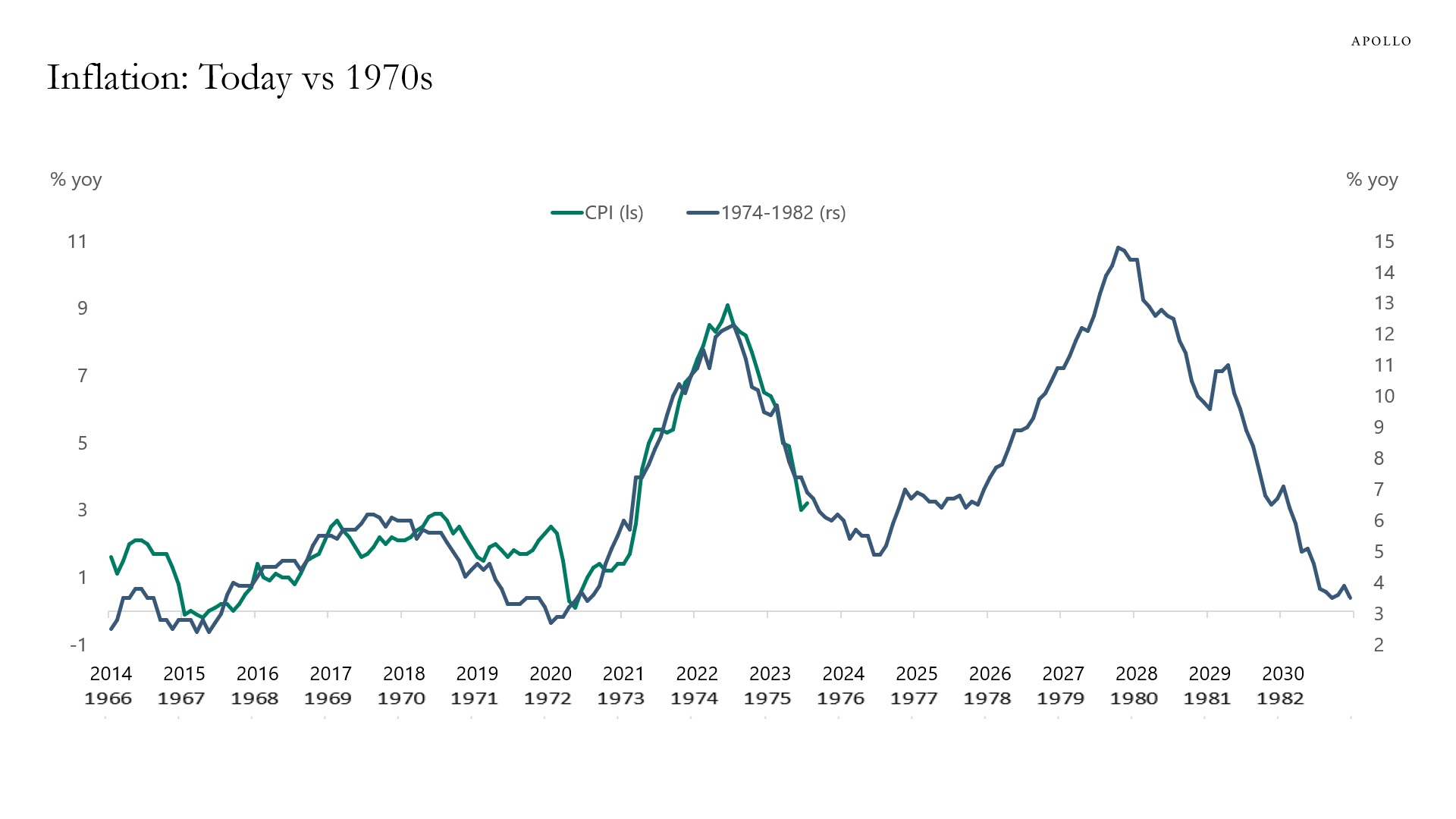

There are two lessons from the 1970s for the Fed today, see chart below.

First, if the Fed turns dovish too quickly, then inflation and inflation expectations will not settle at 2%.

Second, if the economy re-accelerates, the Fed will have to raise rates a lot more.

The implication for markets is that the Fed will be keeping the cost of capital higher for longer than the market is currently pricing to ensure that the FOMC doesn’t repeat the mistakes made in the 1970s.

Source: BLS, Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.