Want it delivered daily to your inbox?

-

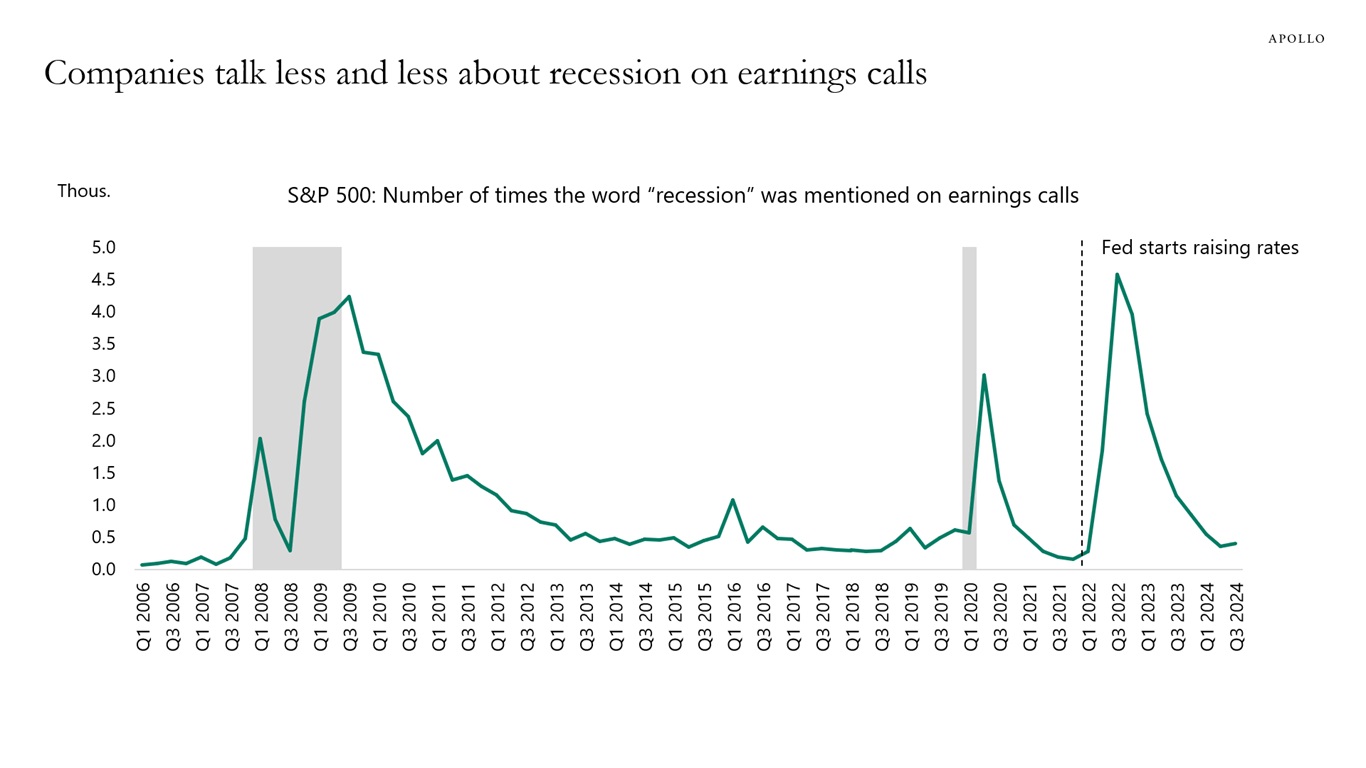

The media is full of anecdotes from earnings calls about the economy supposedly slowing down.

But the reality is that firms on earnings calls talk less and less about recession, see chart below.

In fact, we have never had a recession at the current low level of recession talk, see again chart below.

Source: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

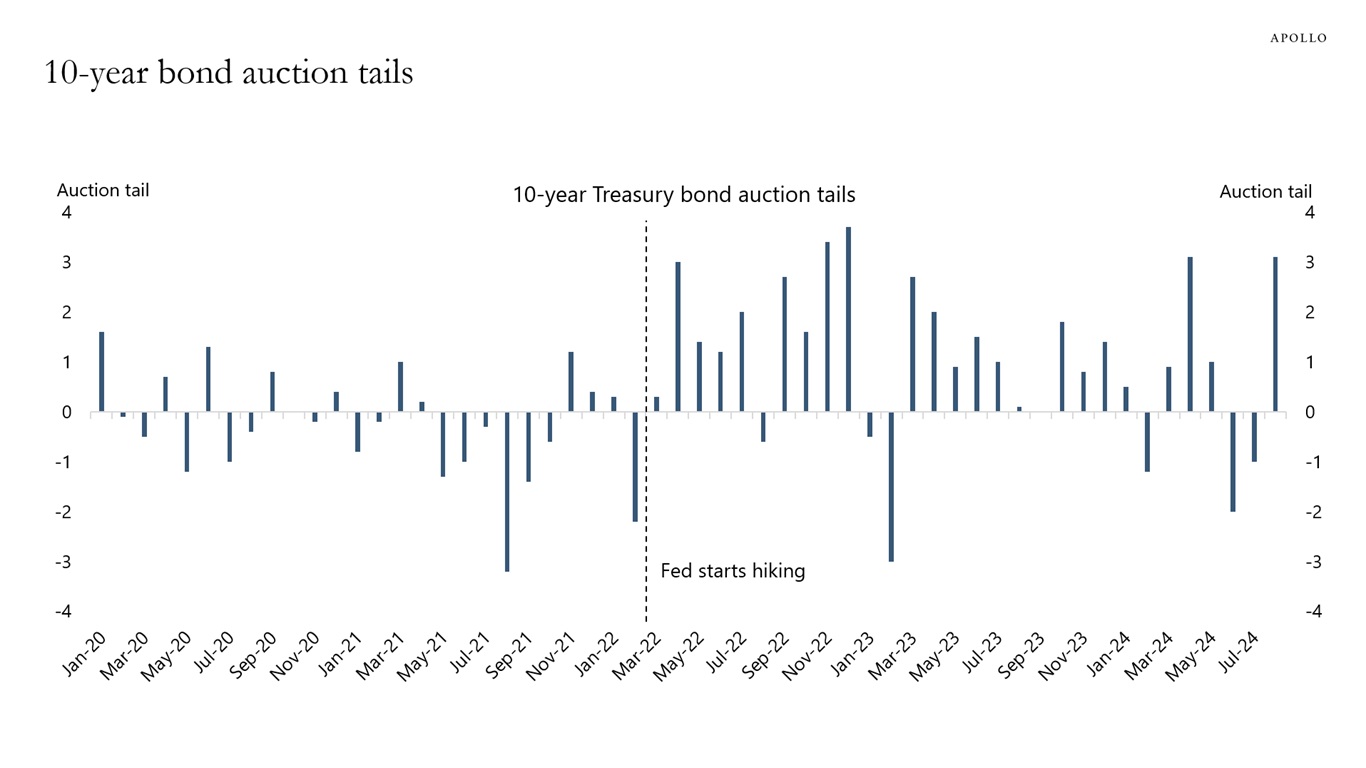

When a US government bond auction is announced, a new when-issued bond starts trading, which allows the market to trade the new Treasury bond before the auction has completed. Such trading activity promotes price discovery and allows the market to trade the government bond before it is available for sale.

When the auction is complete, the yield difference between the when-issued bond and the new bond is generally called the tail. Specifically, a one basis point tail means that the auction result was one basis point higher than where the when-issued yield was trading minutes before the auction was completed, normally at 1 p.m.

This past week, there were auctions for 10-year and 30-year Treasuries, and they both tailed three basis points, which signals that demand for Treasuries was significantly weaker than the market expected. The chart below shows tails for 10-year auctions since January 2020, and the chart shows that a three basis point tail is very significant.

The bottom line is that the trend of larger and more frequent tails since the Fed started raising interest rates in March 2022 underscores the importance of investors closely monitoring Treasury auction metrics. These metrics can provide early indications of weakening demand for Treasuries.

It is possible to track tails in Bloomberg using the tickers USN10YTL and USBD30TL.

Source: US Treasury Department, Bloomberg, Apollo Chief Economist. Note: Bloomberg ticker USN10YTL Index. Auction tail = Difference between the auction draw and when–issued price at auction. A positive tail means the auction yield was higher than or worse than expected. A negative tail means the auction yield was lower than or better than expected. See important disclaimers at the bottom of the page.

-

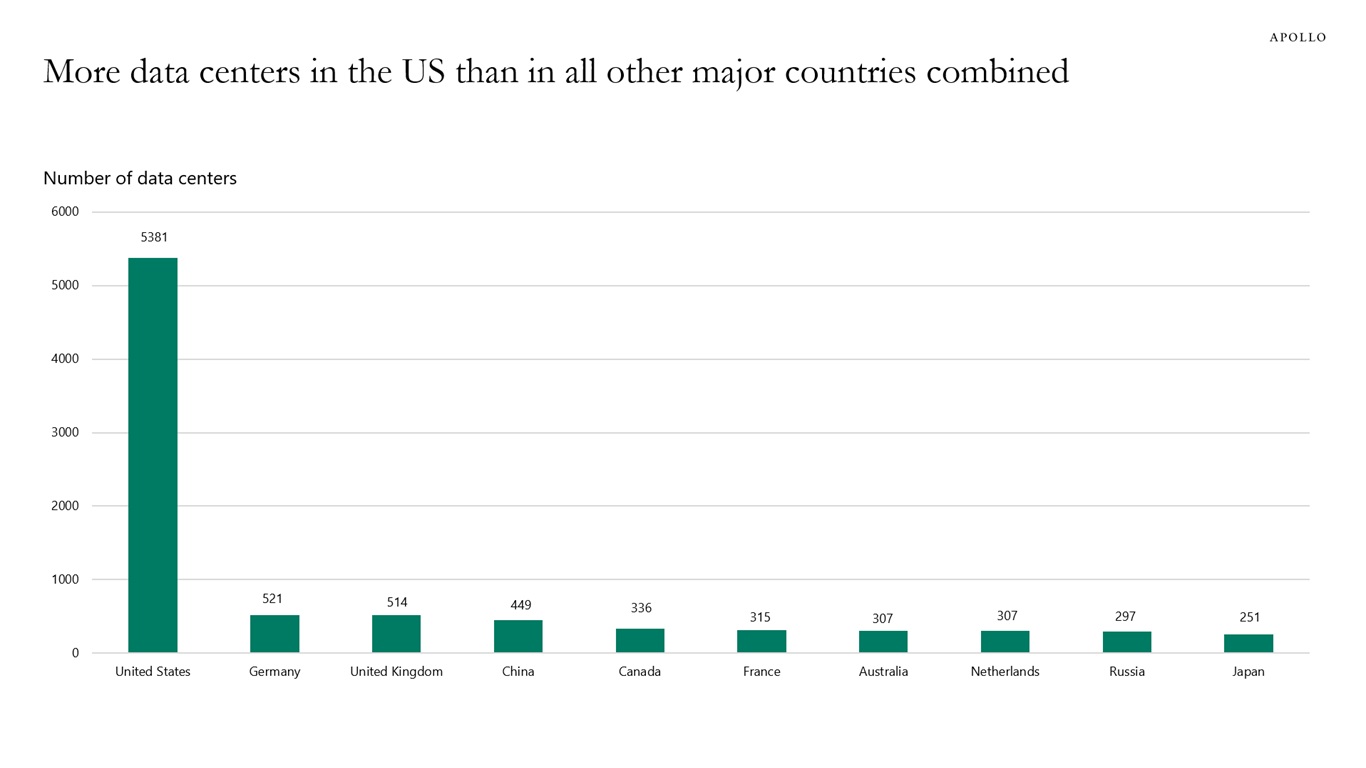

There are more than 5000 data centers in the US. In Germany there are 521 and in China 449, see chart below.

Source: Statista, Cloudscene, Apollo Chief Economist. Note: Data as of March 2024. See important disclaimers at the bottom of the page.

-

Jobless claims declined this week, the Atlanta Fed GDP for Q3 currently stands at 2.9%, and the Dallas Fed weekly GDP indicator is currently 2.2%.

The bottom line is that there are still no signs of a US recession, and the US economy is doing just fine with steady growth in daily and weekly data for restaurant bookings, air travel, hotel bookings, credit card data, bank lending, Broadway show attendance, box office grosses, and weekly data for bankruptcy filings trending lower, see our chart book with indicators updated as of August 10.

In short, Fed pricing is wrong, and the market is making the same mistake it made at the beginning of the year.

See important disclaimers at the bottom of the page.

-

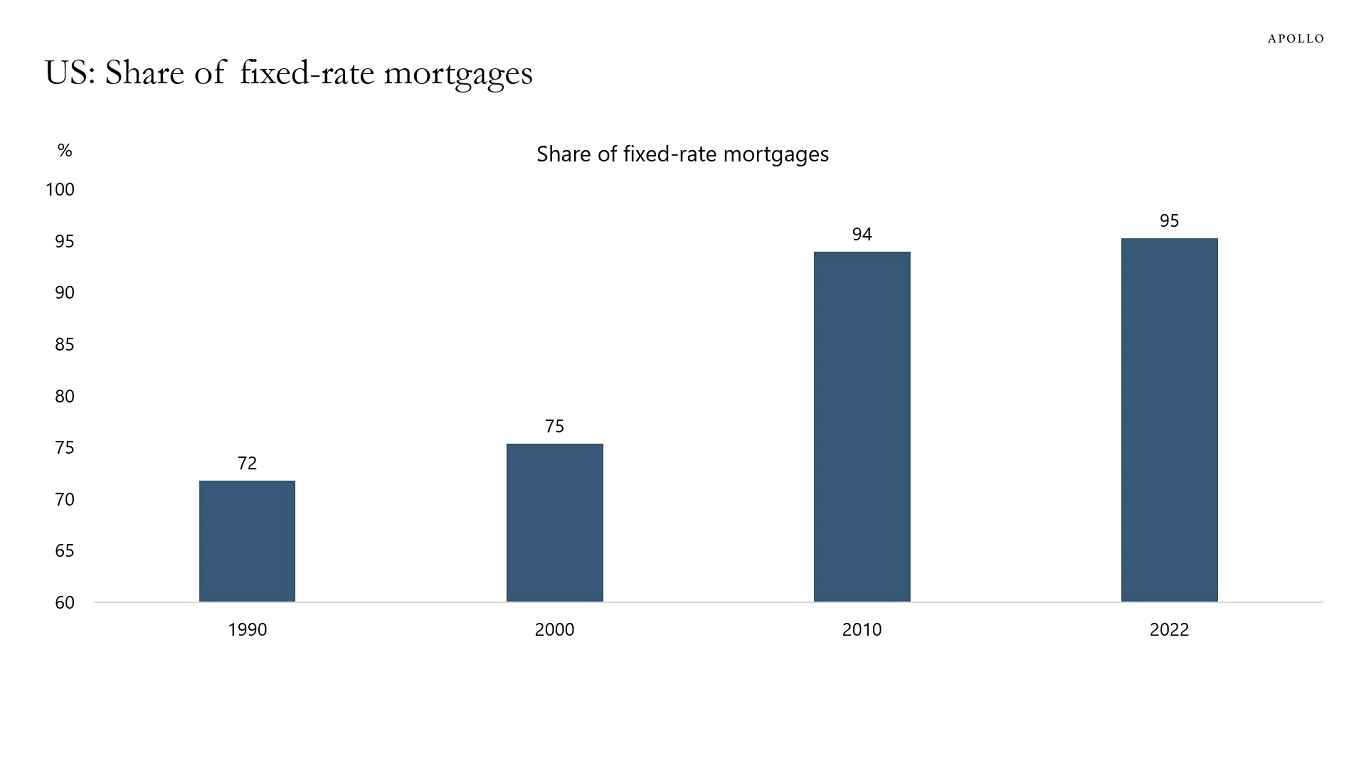

The rise in the share of fixed-rate mortgages over the past four decades is the reason why the transmission mechanism of monetary policy is weaker today, see chart below.

When interest rates go up, it has a milder impact on the economy as mortgages are locked-in at lower interest rates. But this effect is symmetric. When the Fed starts cutting interest rates in September, lowering interest rates will not trigger a strong boost to housing demand because 95% of mortgage holders are already in mortgages with low interest rates. In addition, a record-high 40% of homeowners don’t have a mortgage, which also contributes to making monetary policy less potent.

The bottom line is that the high share of fixed-rate mortgages makes monetary policy less effective both when the Fed raises interest rates and when the Fed lowers interest rates.

Source: FHLMC, FHFA, Haver Analytics, IMF WEO, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

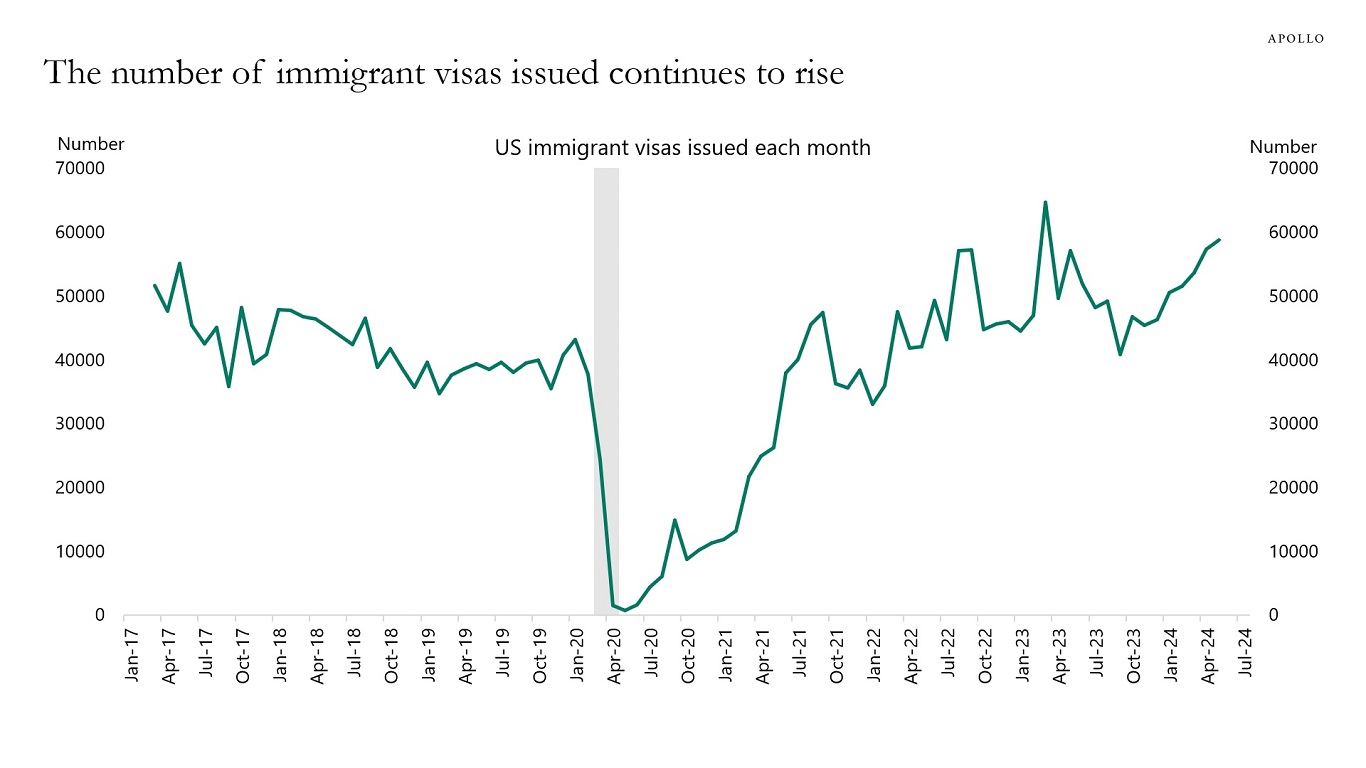

The uptrend in immigration continues with a near record-high level of immigrant visas issued every month, see chart below. Examples of immigrant visas include employer-based visas and family-sponsored visas (such as spouses of US citizens). Maybe the reason why the unemployment rate is rising is because the government is gradually working through a Covid-related backlog of visa applications, which increases the labor supply.

Note: The data is monthly visas issued. Source: US Department of State, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

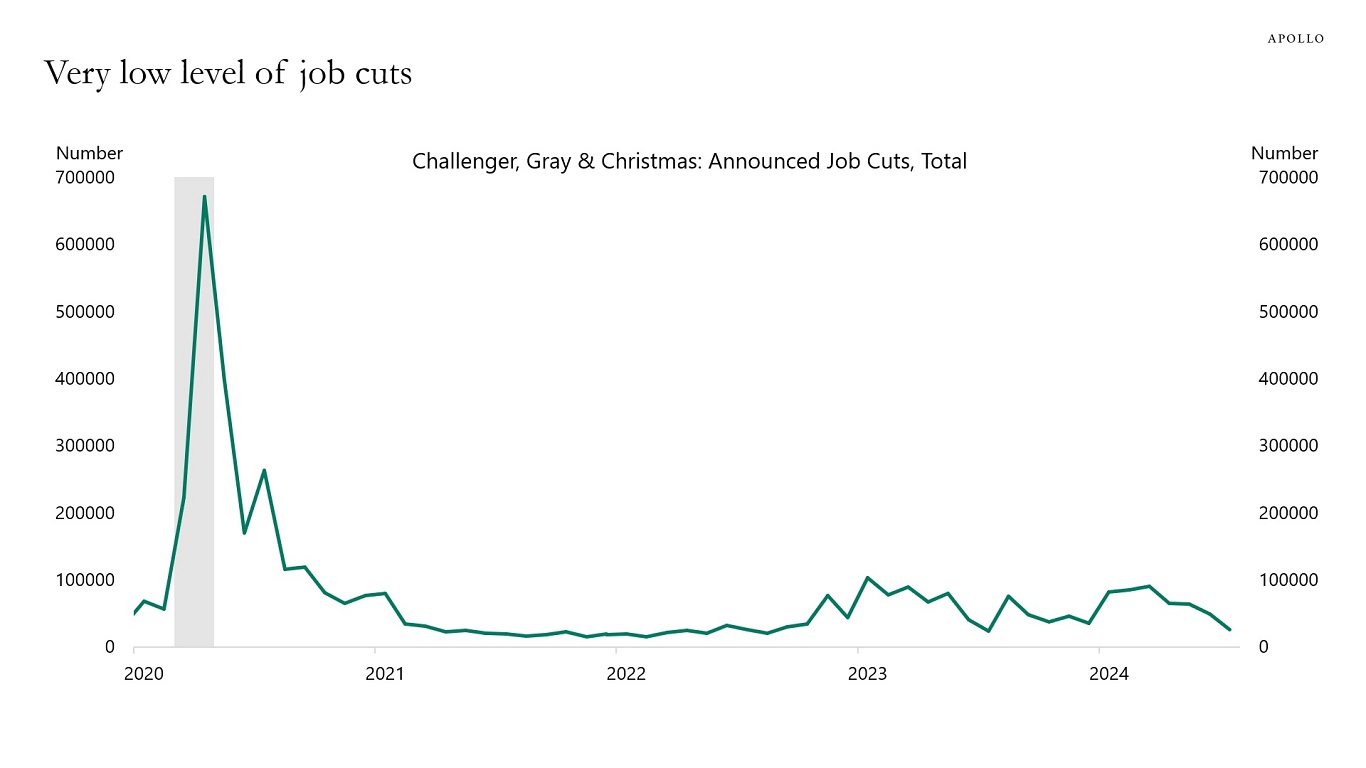

The source of the rise in the unemployment rate is not job cuts but a rise in labor supply because of rising immigration. That is the reason why the Sahm rule doesn’t work. The Sahm rule was designed for a decline in labor demand, not a rise in immigration.

For more insights, a replay of my Tuesday webcast on the current market volatility and its implications for the Fed, the economy, and the markets is available here.

Source: Challenger, Gray & Christmas, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

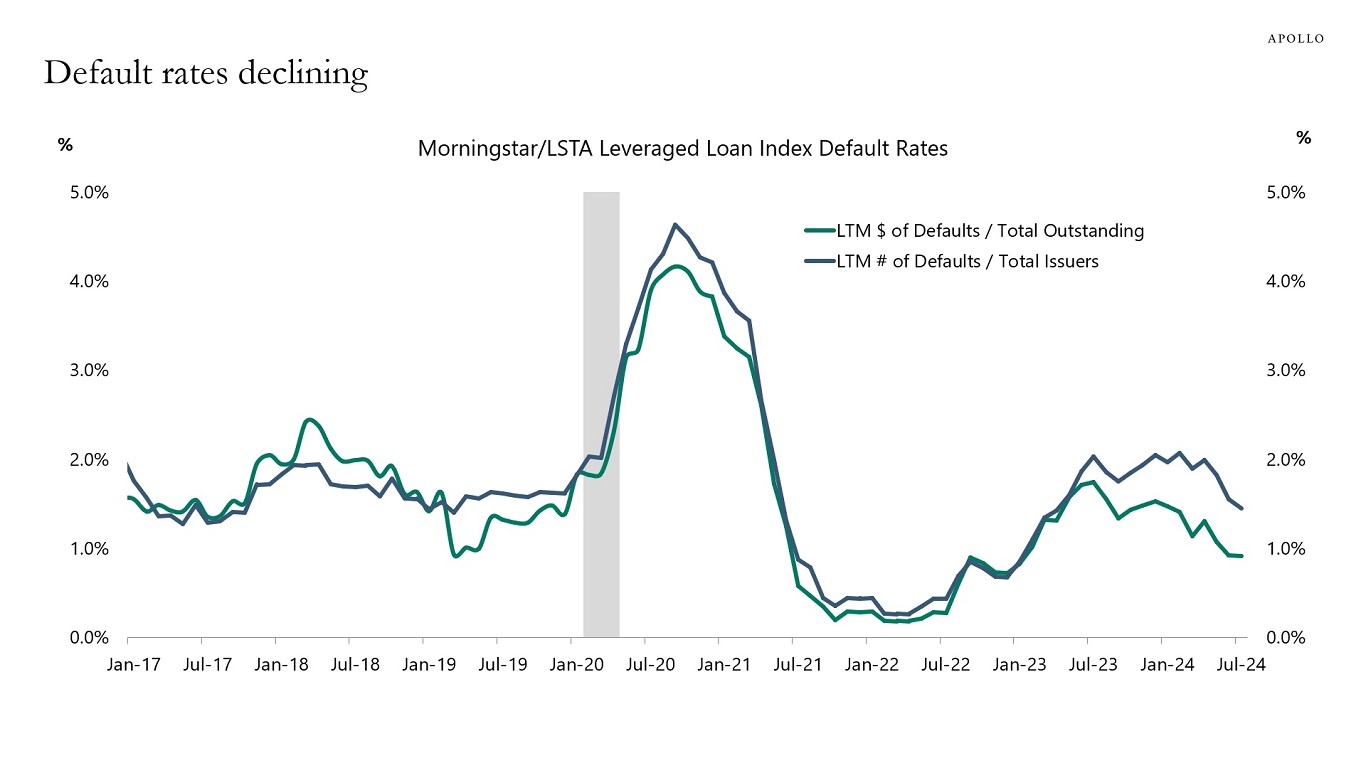

The soft employment report for July is in sharp contrast to the steady decline in default rates seen in recent months, see chart below.

If the economy were crashing, default rates would be spiking higher, and that is not what the data shows.

Also, join us today for a live discussion hosted by yours truly on what the current market volatility might mean for the Fed, the economy, and the markets. We start at 8:00 am EDT. Register now.

Source: PitchBook LCD, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

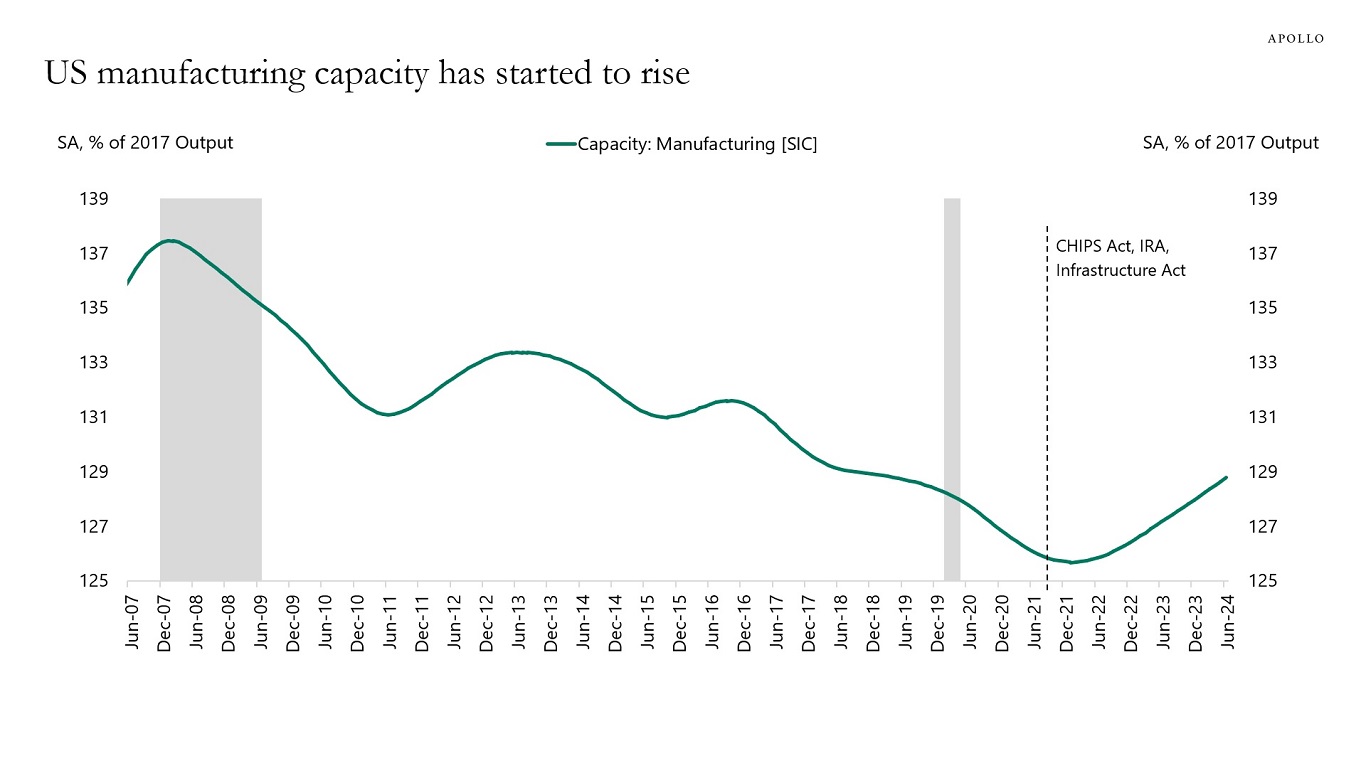

The CHIPS Act, the Inflation Reduction Act, and the Infrastructure Act have triggered a new industrial renaissance in AI and energy. Also, US manufacturing capacity is now growing after having declined for many decades, see chart below.

Note: SIC = Standard Industrial Classification. Source: Federal Reserve Board, National Bureau of Economic Research, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

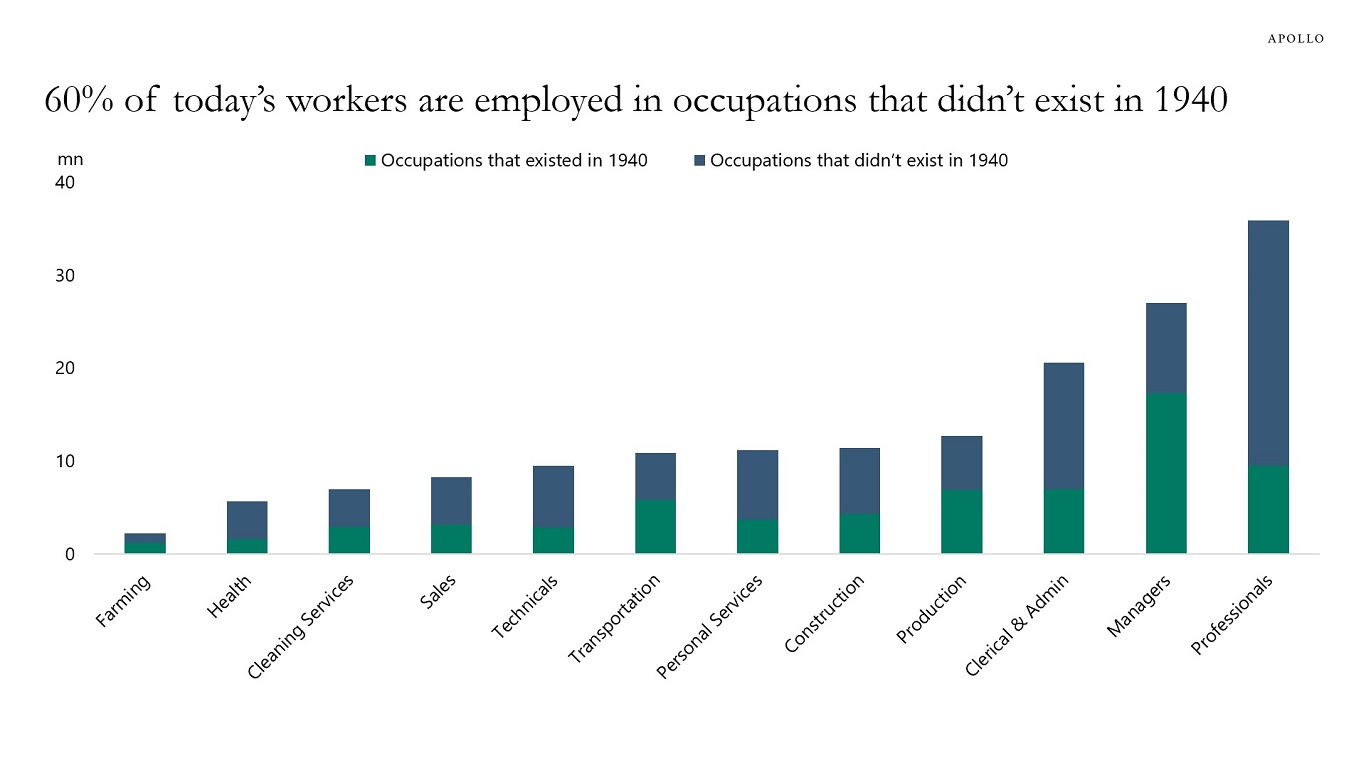

Research by David Autor from MIT shows that 60% of today’s workers are employed in occupations that didn’t exist in 1940, see chart below.

This is important when discussing what impact AI may have on the labor market.

Source: David Autor, Caroline Chin, Anna Salomons, Bryan Seegmiller, “New Frontiers: The Origins and Content of New Work, 1940–2018.” The Quarterly Journal of Economics, Volume 139, Issue 3, August 2024; Apollo Chief Economist See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.