Want it delivered daily to your inbox?

-

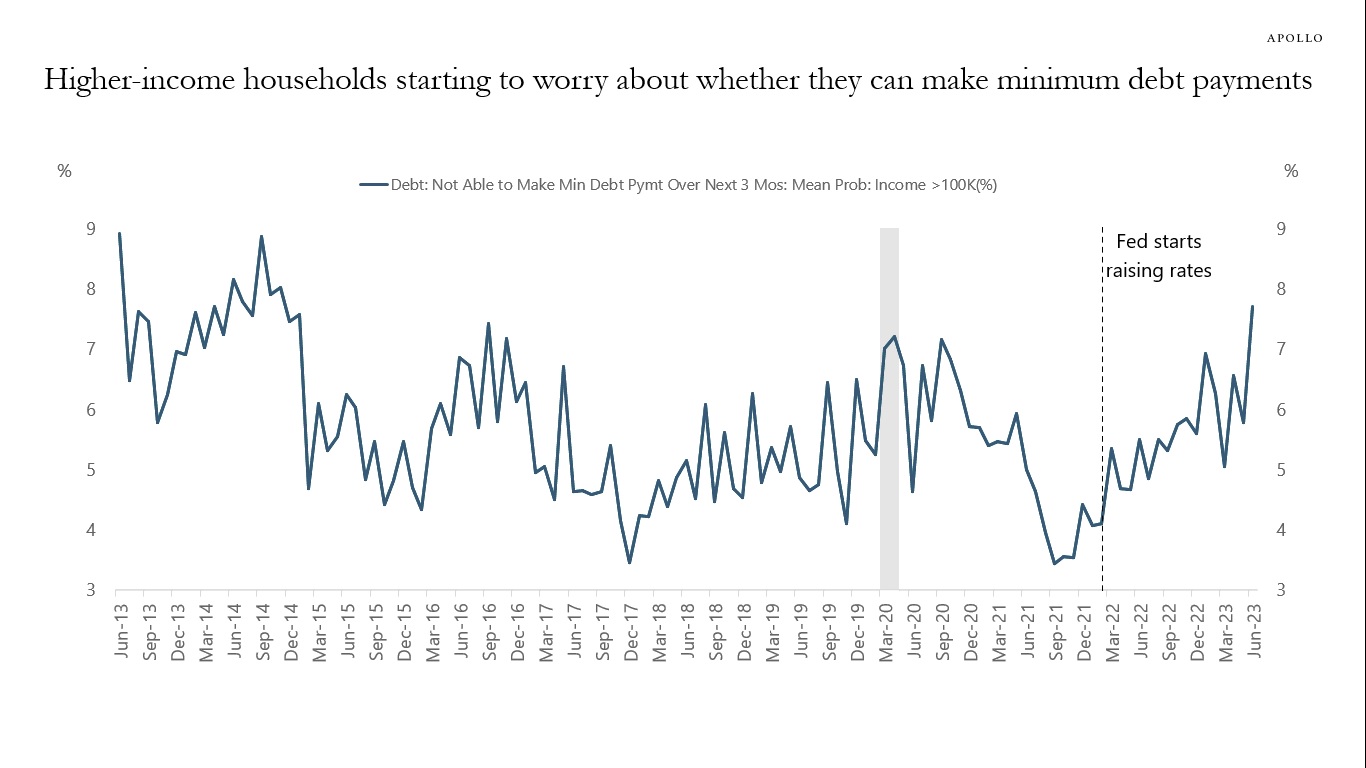

The chart below shows the average probability of not being able to make minimum debt payments over the next three months for people earning more than $100,000. The bottom line is that higher-income households are starting to worry about their finances.

Source: FRBNY, Haver Analytics, Apollo Chief Economist. Note: The data shows the average probability of not being able to make minimum debt payment over the next three months for people earning (income) greater than $100K. See important disclaimers at the bottom of the page.

-

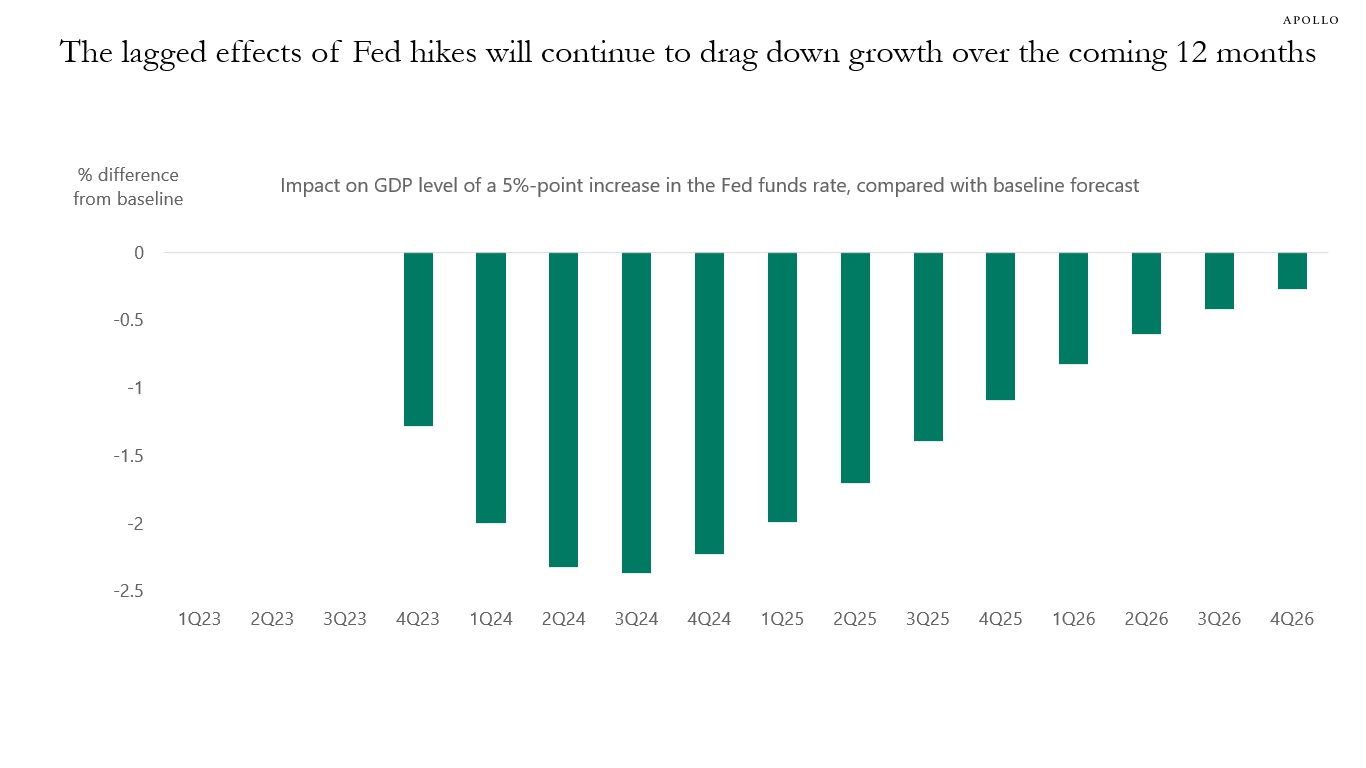

The Fed has raised the Fed funds rate to 5%, and the lagged effects of Fed hikes will continue to drag down growth over the coming 12 months. See chart below, which shows a simulation with the impact of a 5% increase in the Fed funds rate on the level of GDP done on a variant of the Fed’s FR/BUS model of the US economy.

In other words, the transmission mechanism of monetary policy takes time, and the drag on growth from lagged Fed hikes over the coming year will be significant. That is why a recession is a more likely outcome than a soft landing, no matter what happens to inflation.

Source: Bloomberg, Apollo Chief Economist. Note: 500bps monetary policy shock in 3Q23. See important disclaimers at the bottom of the page.

-

The market seems to be of the view that if inflation quickly declines to the Fed’s 2% target, then everything will be fine and stocks will continue to go up, and credit spreads will continue to narrow.

There are two problems with this logic.

1) If inflation comes down faster than the Fed expects, it is because the economy is slowing faster than the Fed expects. For example, if wholesale car prices decline more quickly than expected, then it is driven by a sharper-than-expected drop-off in demand for cars.

2) The Fed and academics agree that it takes 12 to 18 months before monetary policy impacts the economy, and this is true both when the Fed is raising rates and when they are cutting rates. So if inflation quickly declines to 2%, we would still have 12 to 18 months of slowing growth ahead of us.

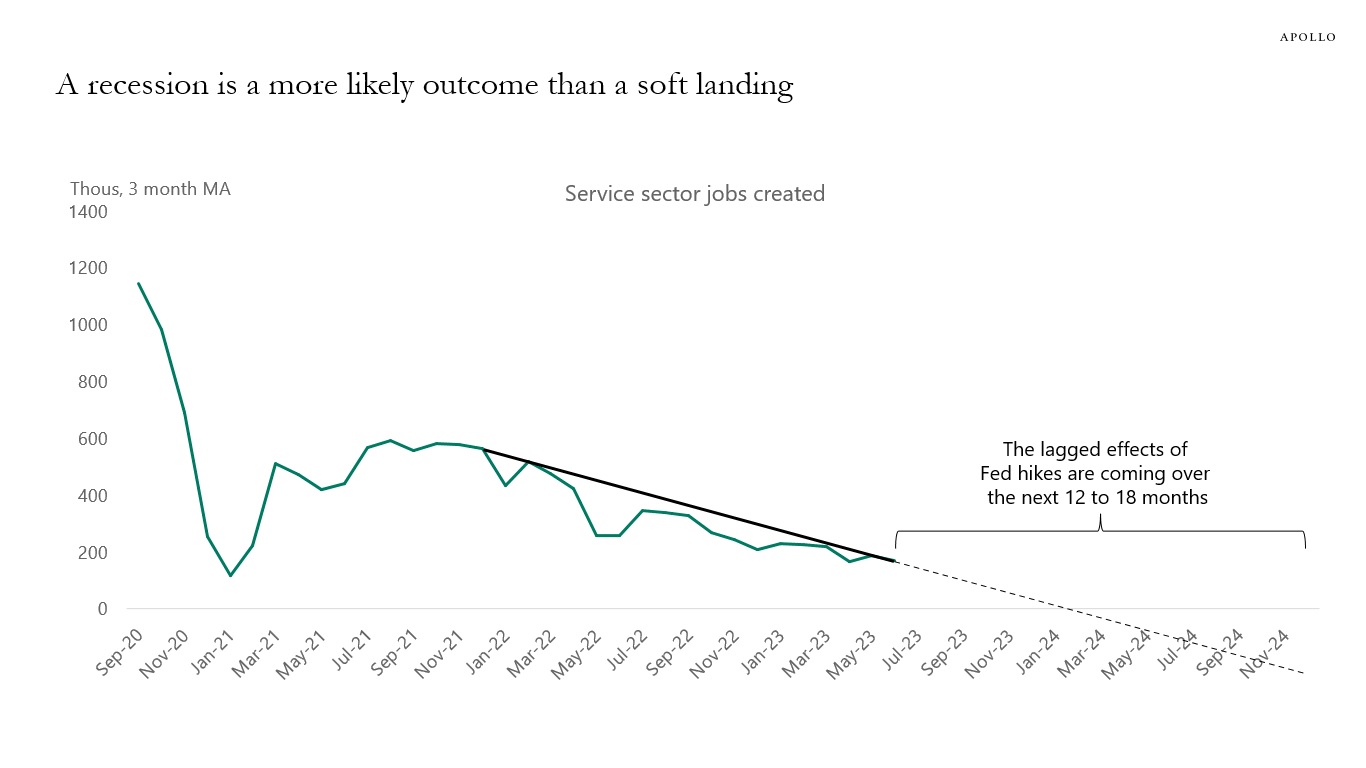

The bottom line is that no matter what happens to inflation, the lagged effects of Fed hikes will continue to drag the economy down over the coming 12 to 18 months, and that is why a recession is a more likely outcome than a soft landing, see chart below.

Source: BLS, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

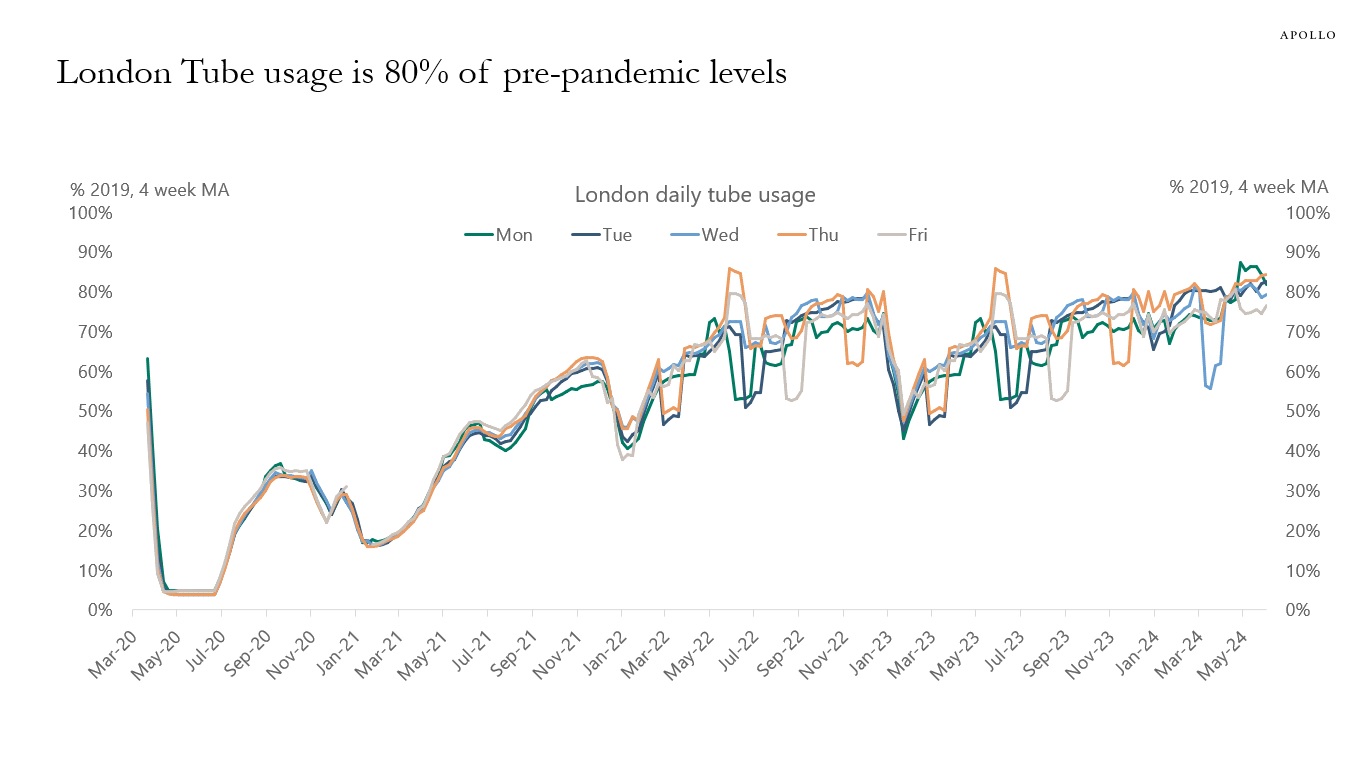

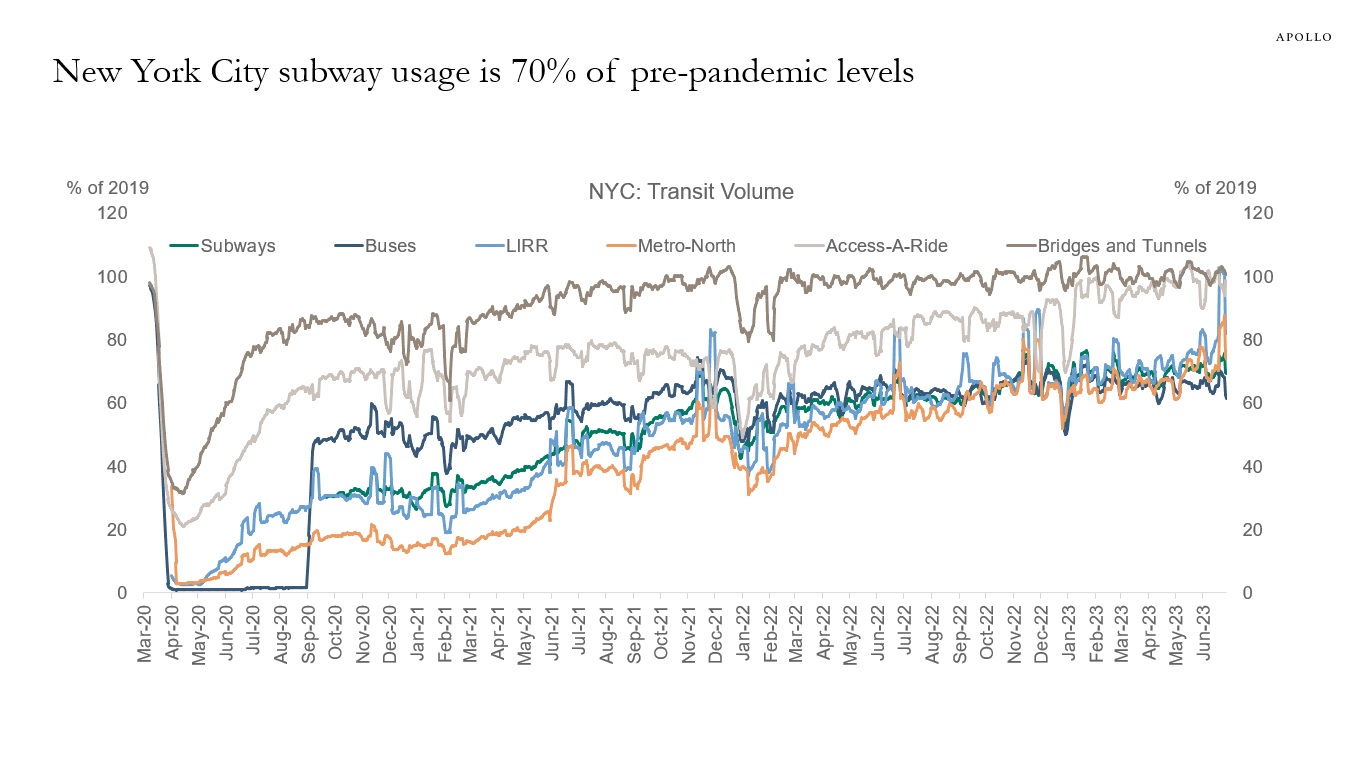

Both London and New York are seeing a gradual move back towards normal. London underground usage is 80% of pre-pandemic levels, and New York City subway usage is 70%, see charts below. The rising trends in these charts bode well for a recovery over time in office, retail, and commercial real estate more broadly.

Source: ONS, TfL, Apollo Chief Economist

Source: MTA, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

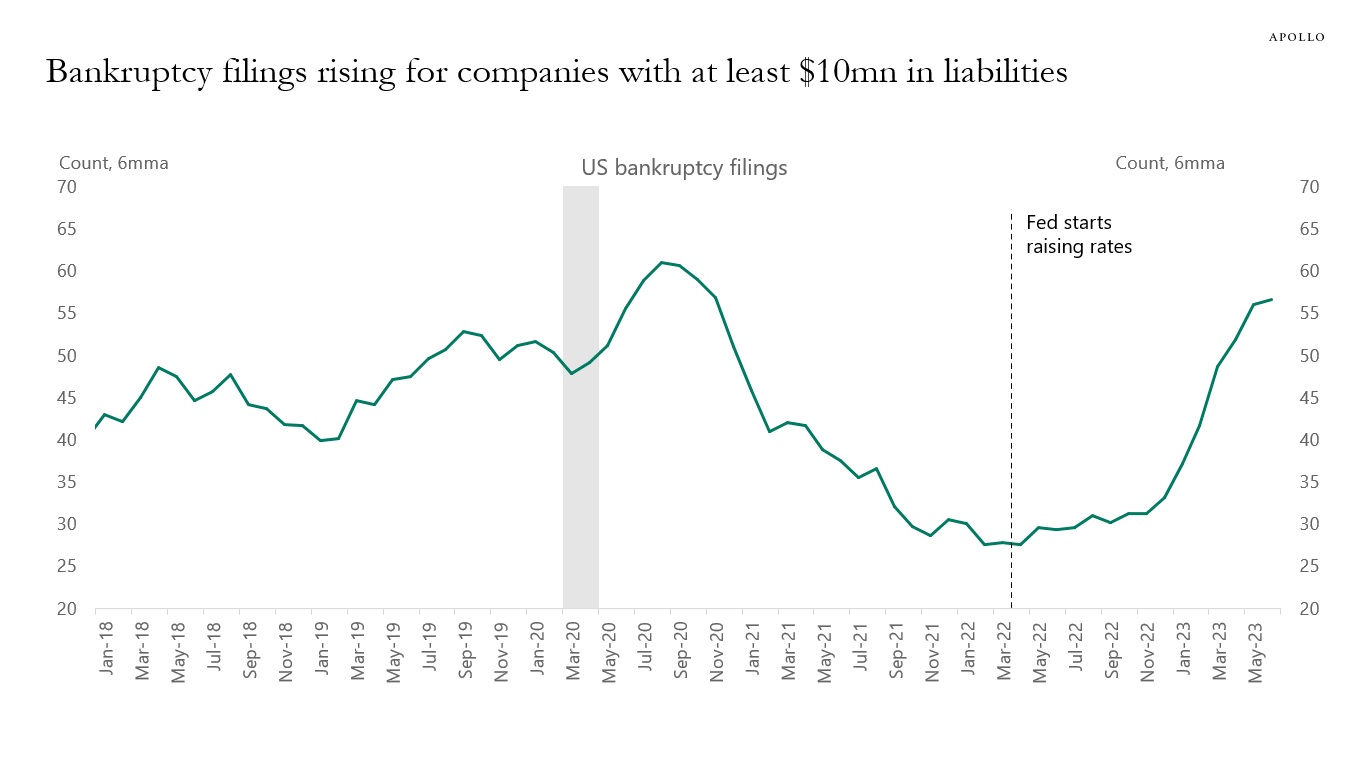

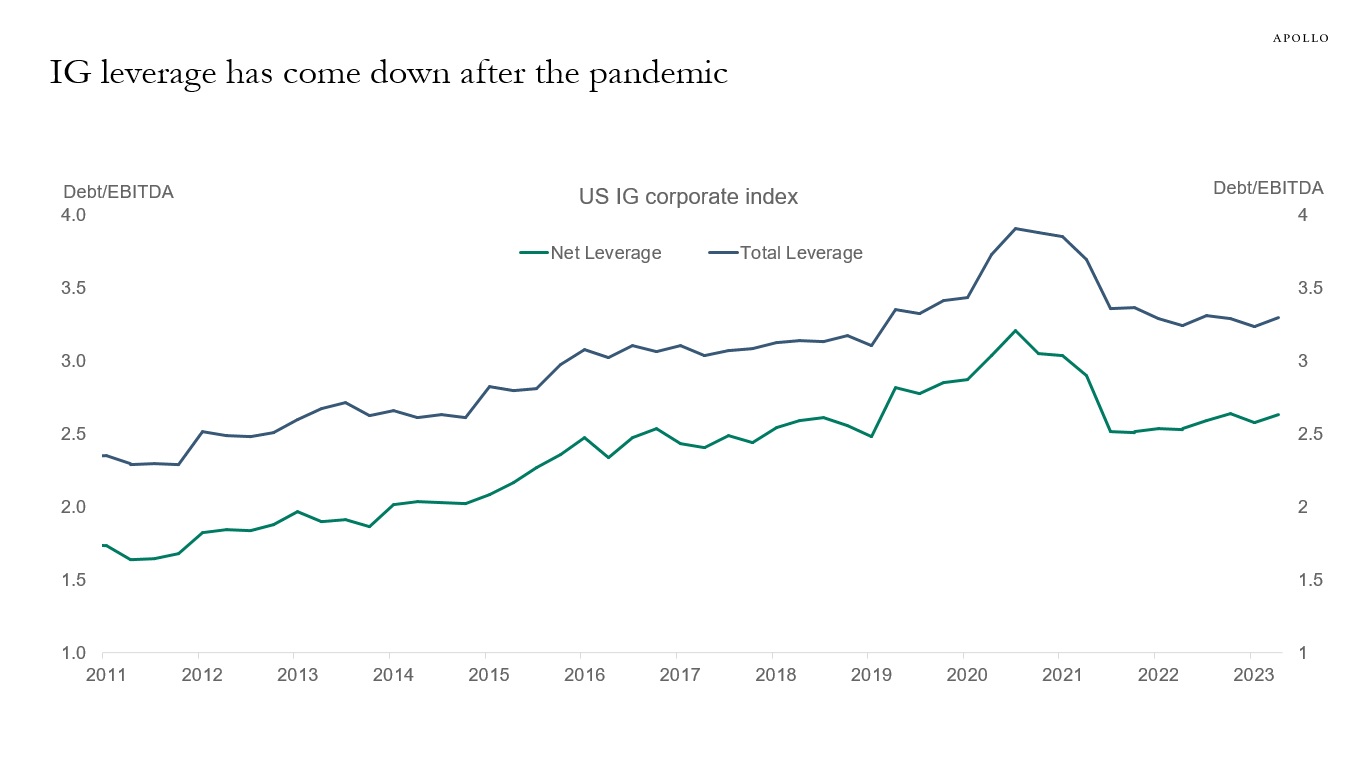

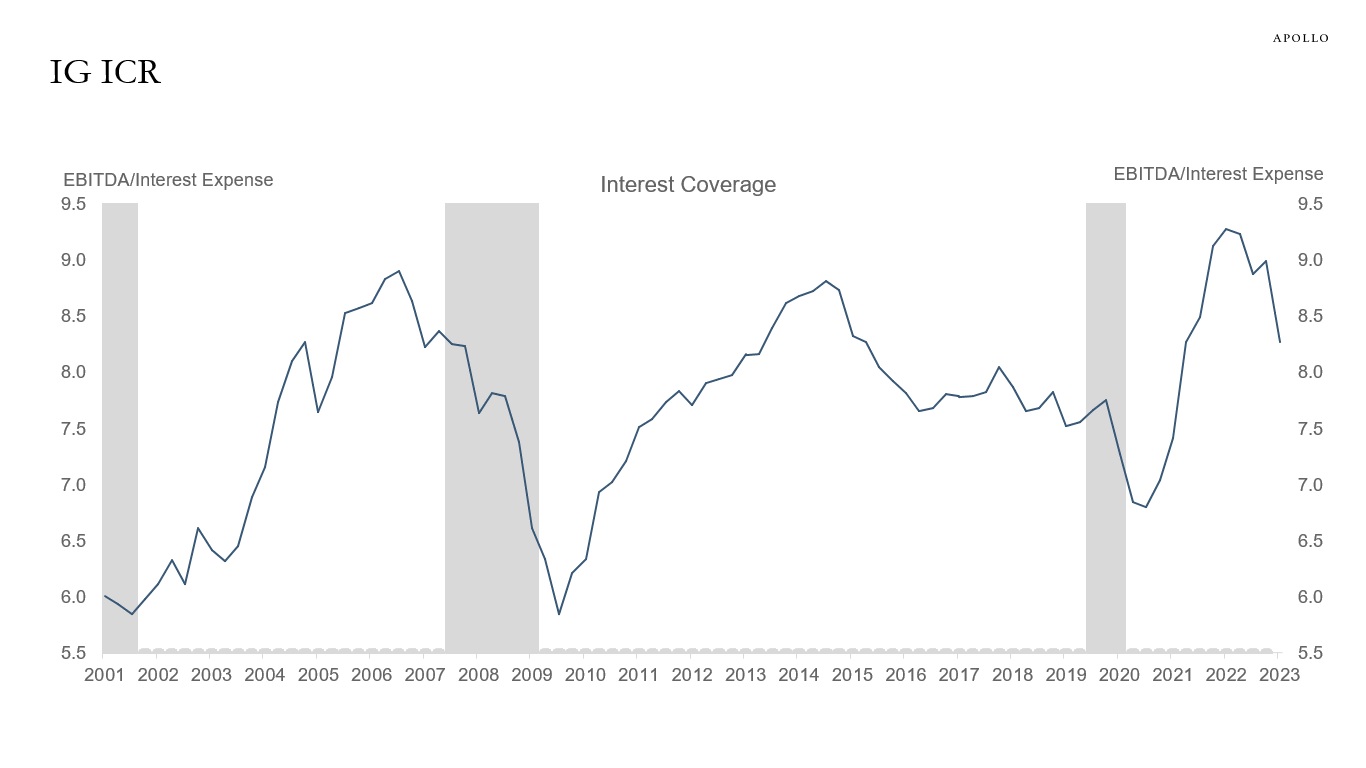

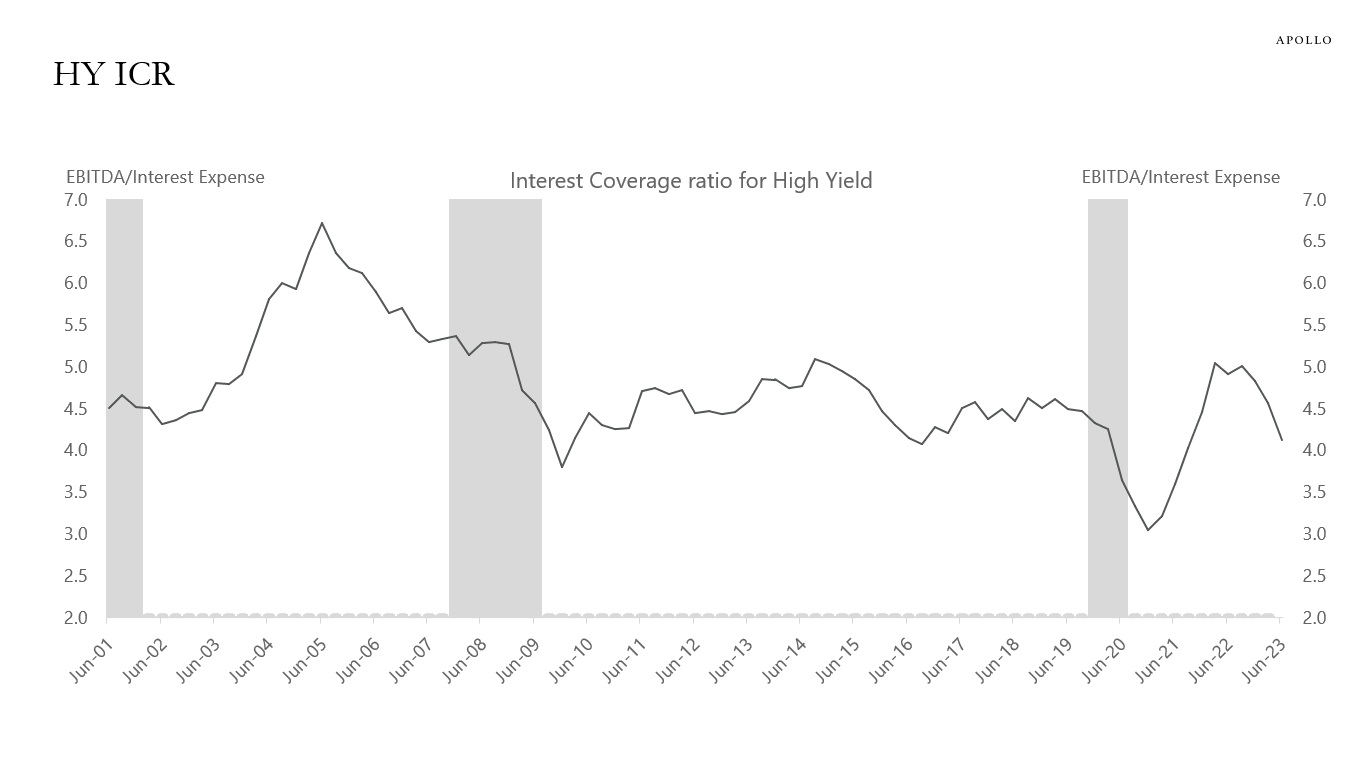

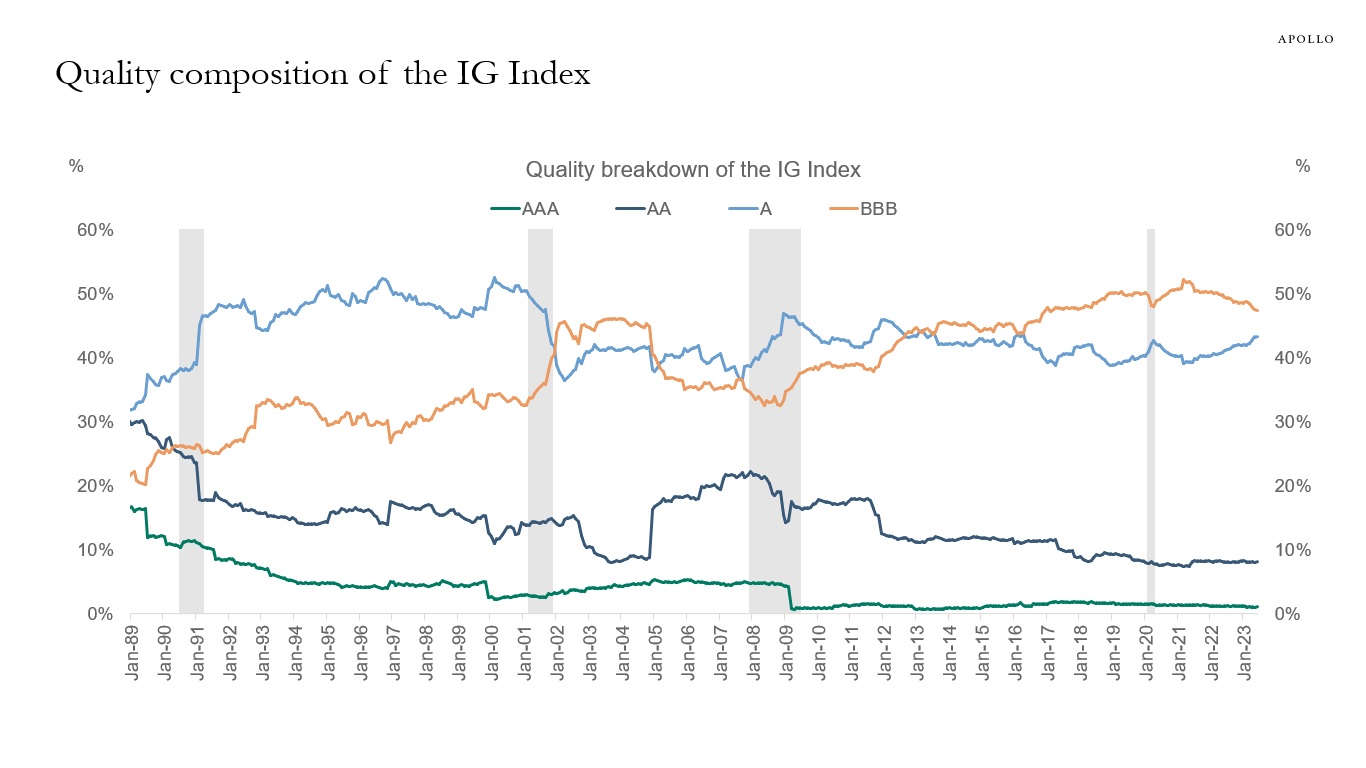

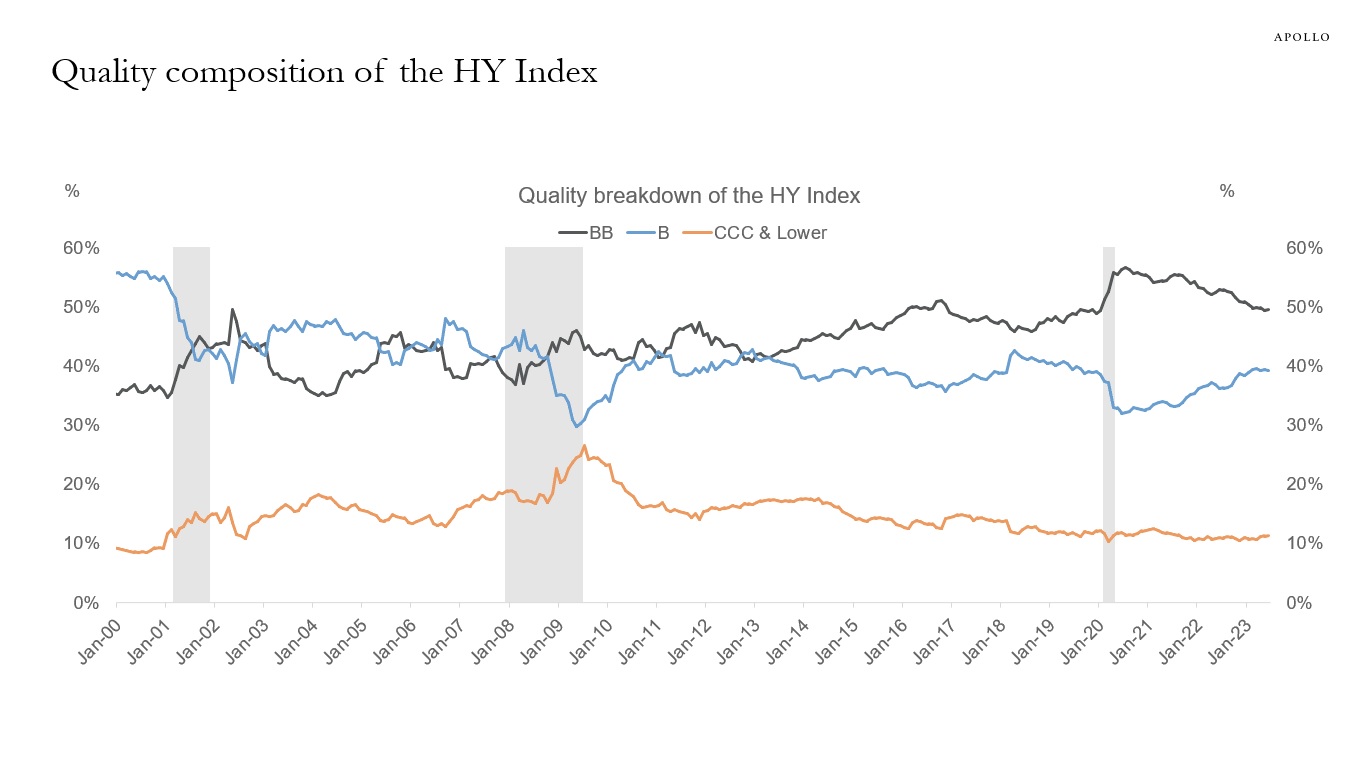

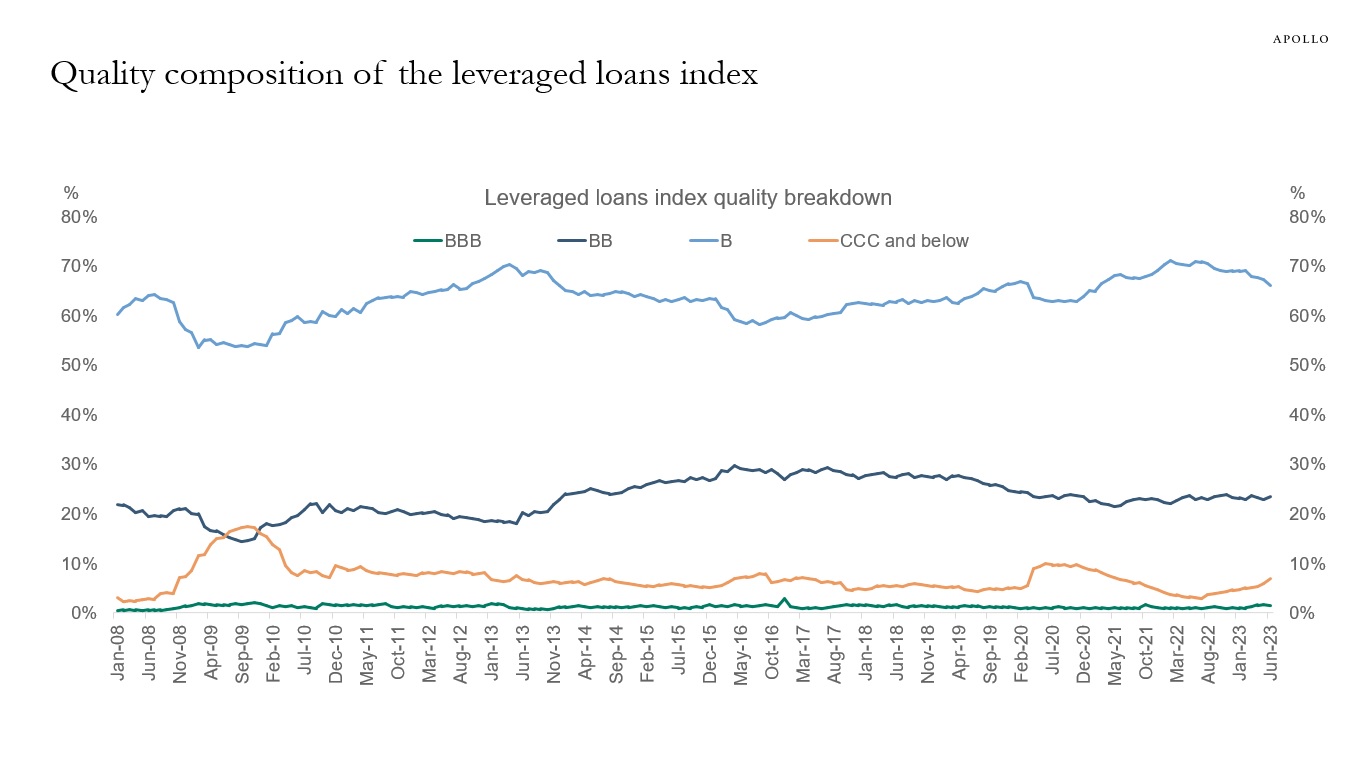

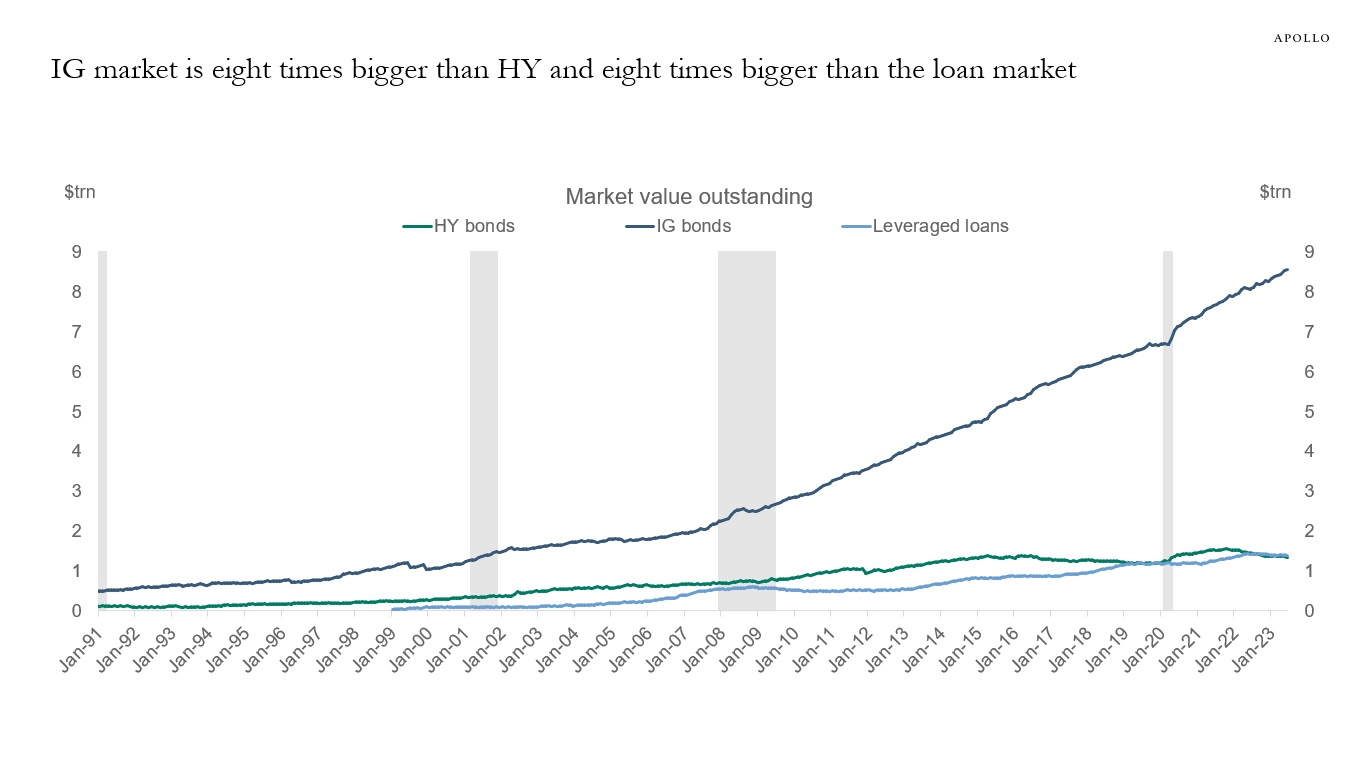

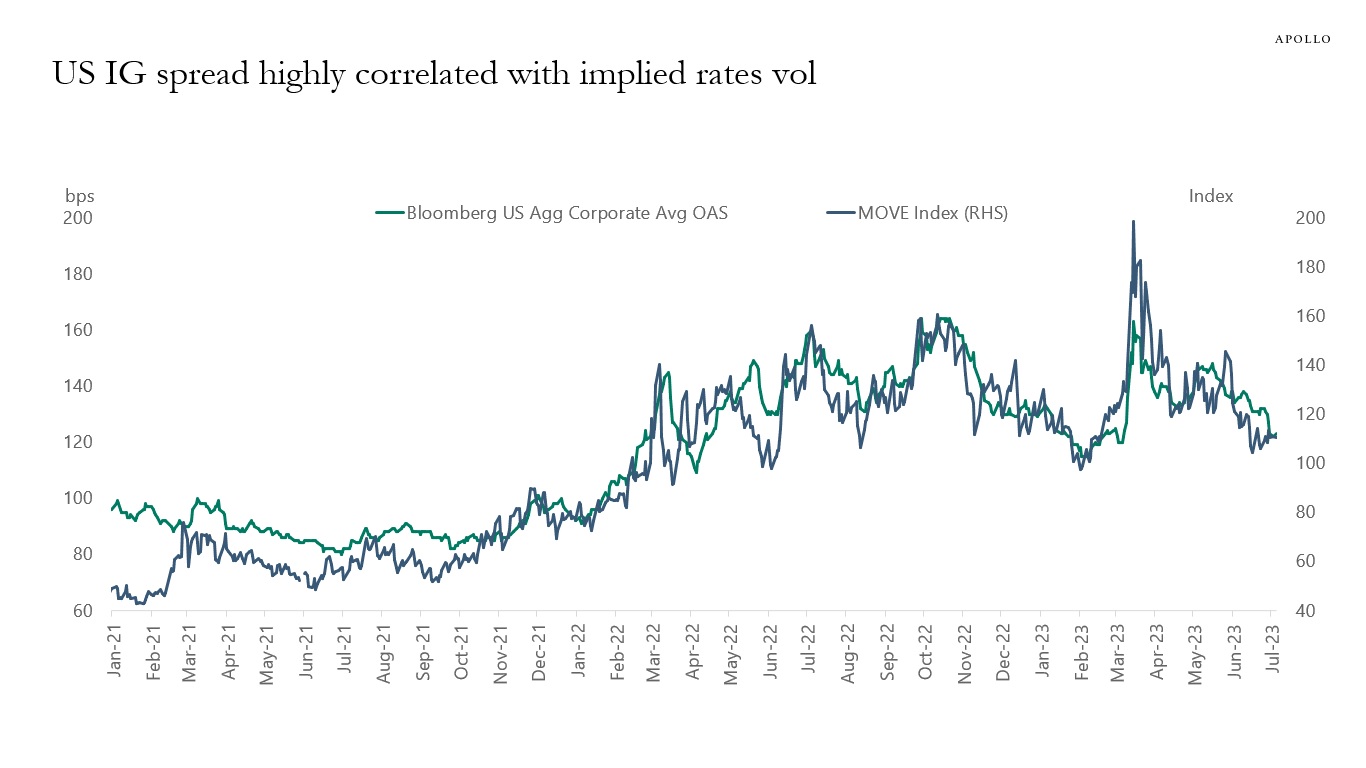

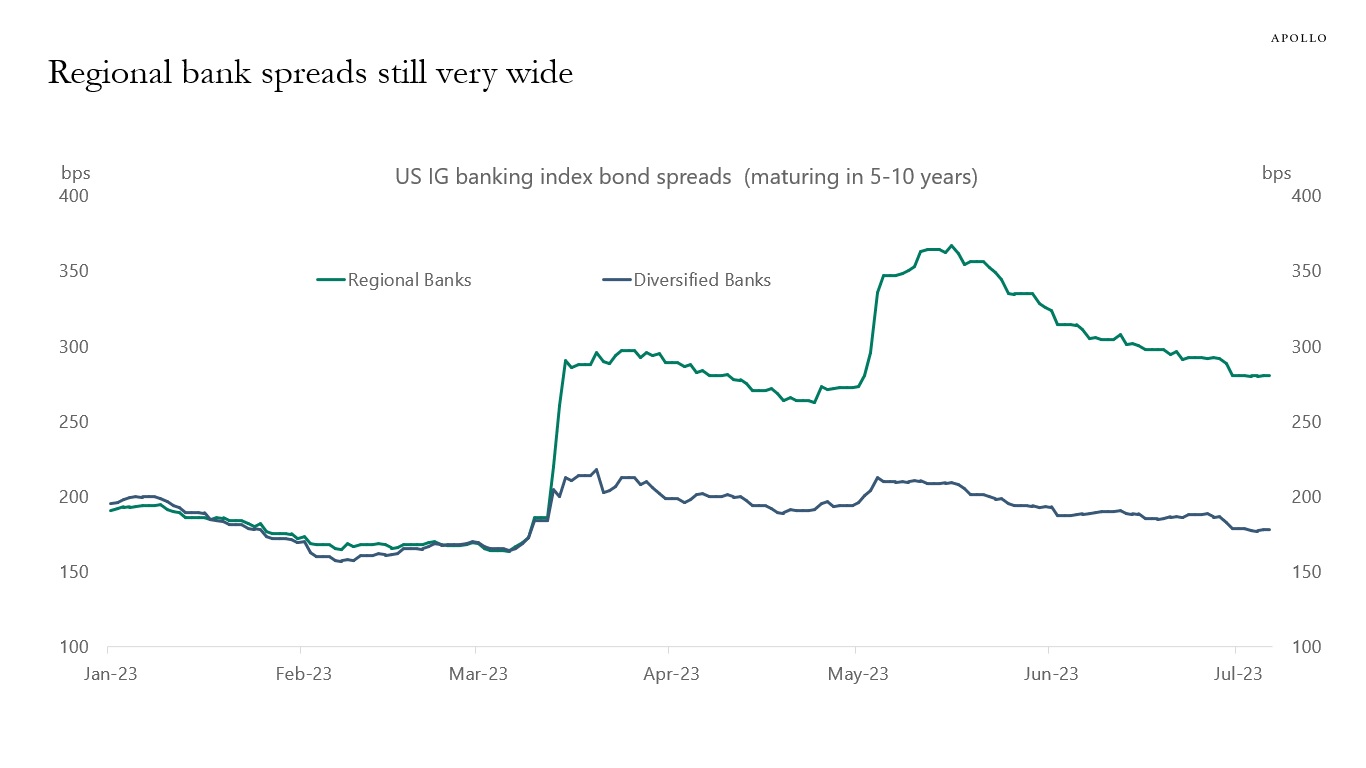

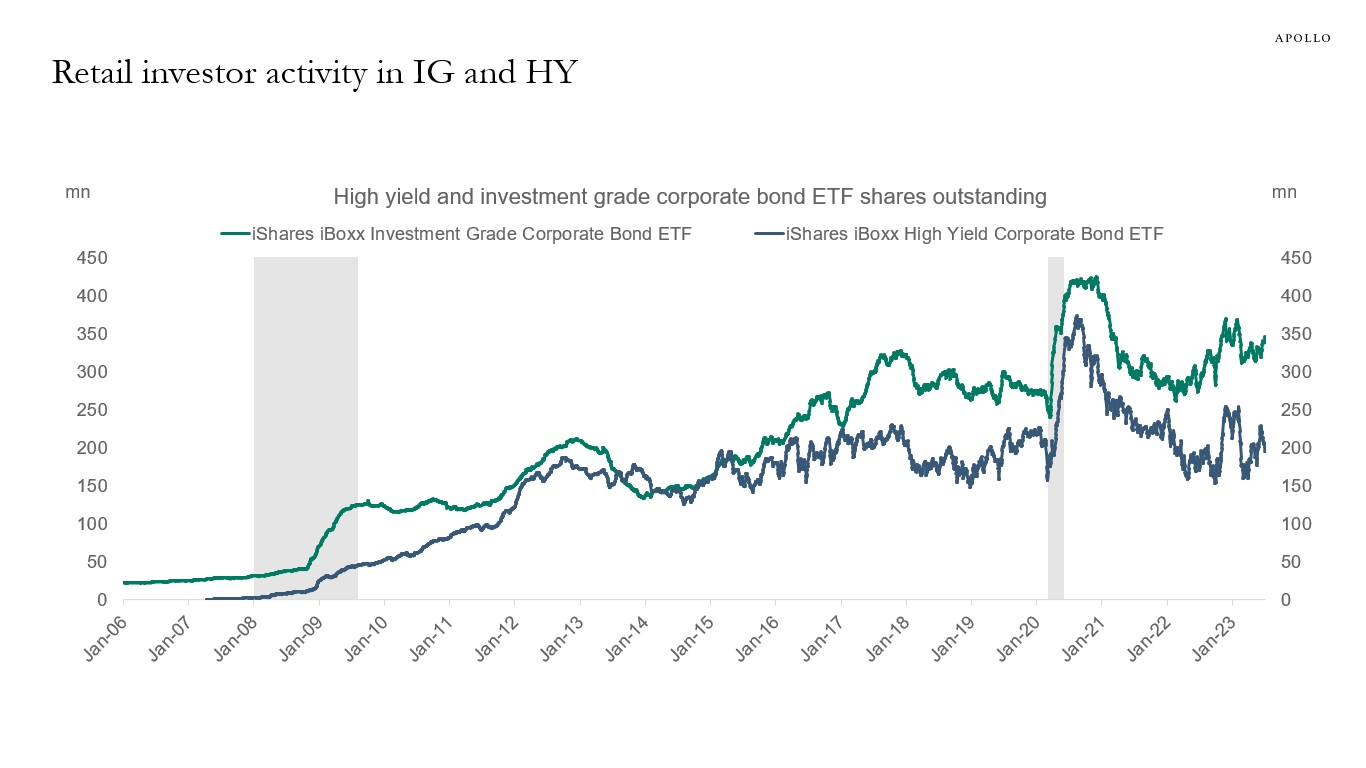

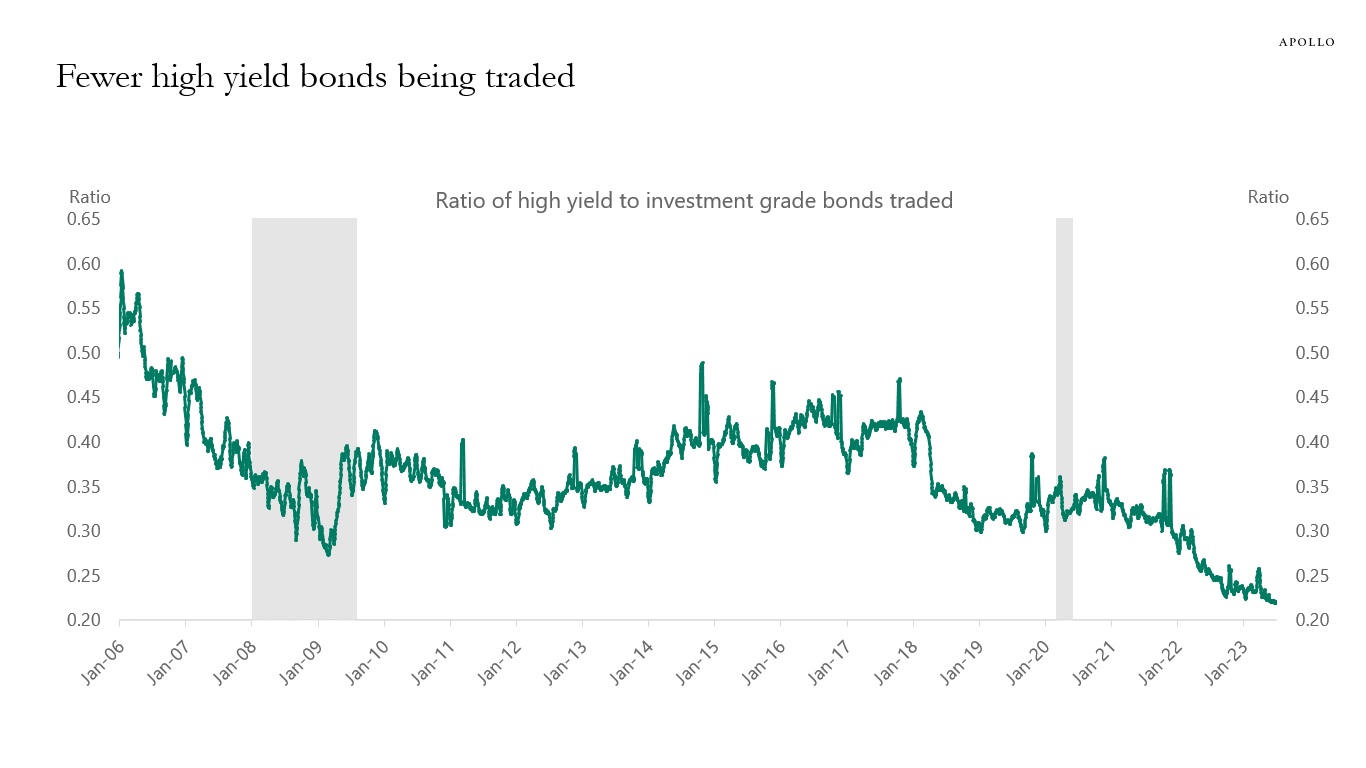

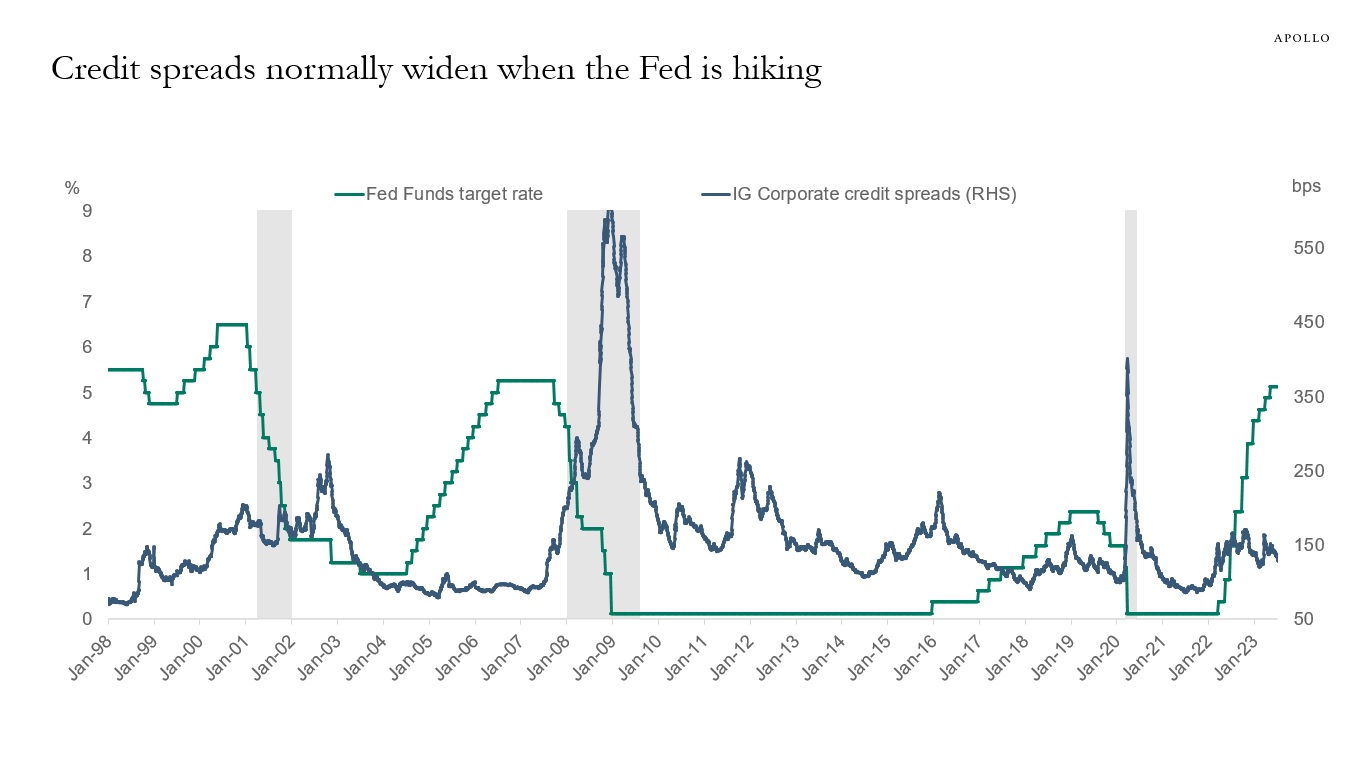

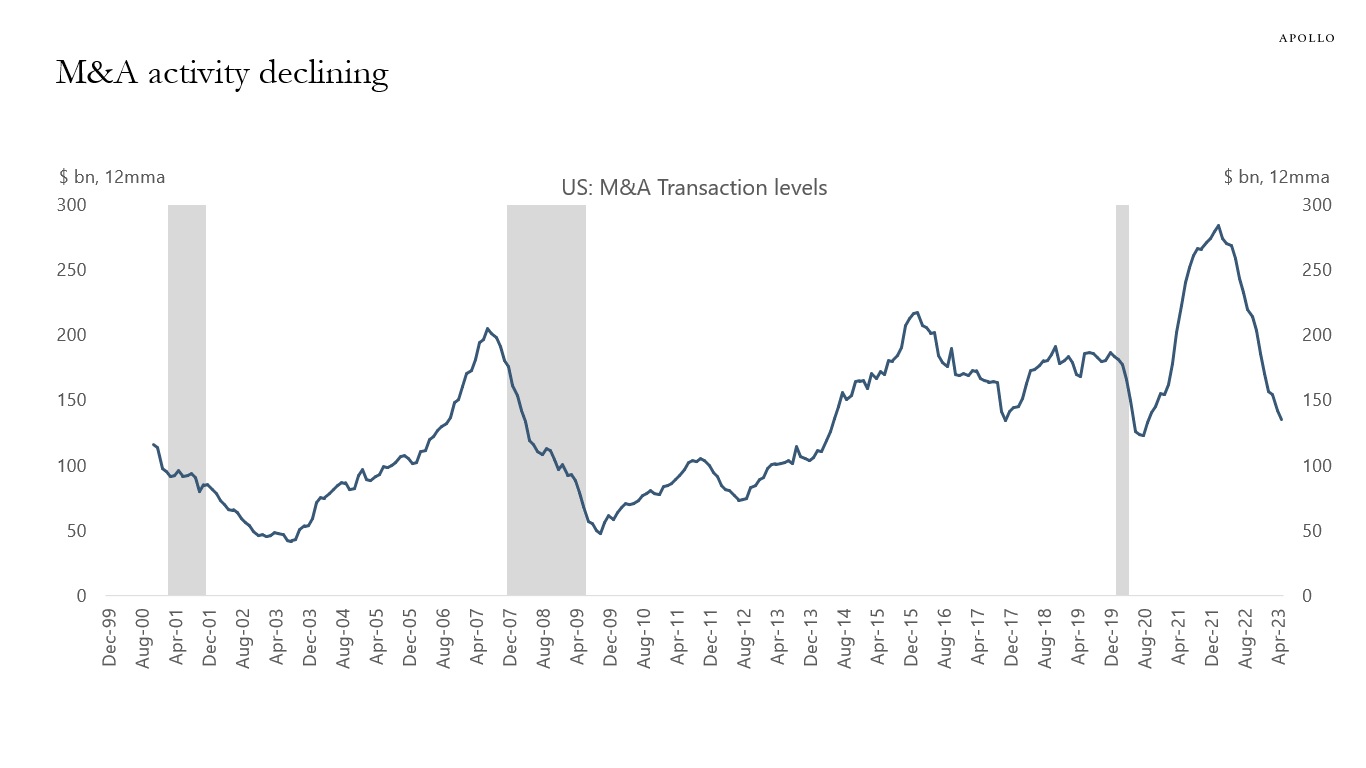

High rates and a slowing economy are creating opportunities for credit investors. Our latest credit market outlook is available here, key charts inserted below.

Source: S&P Capital IQ, Bloomberg, Apollo Chief Economist. Note: Bankruptcy figures include public companies or private companies with public debt with a minimum of $2 million in assets or liabilities at the time of filing, in addition to private companies with at least $10 million in assets or liabilities.

Source: Bloomberg, Apollo Chief Economist. Note: Median leverage for the bonds in H0A0 index.

Source: ICE BofA, Bloomberg, Apollo Chief Economist. Note: Index used C0A0 Index.

Source: Bloomberg, Apollo Chief Economist

Source: Bloomberg, Apollo Chief Economist

Source: ICE BofA, Bloomberg, Apollo Chief Economist. Note: Breakdown by market value. Data as of June 30, 2023.

Source: ICE BofA, Bloomberg, Apollo Chief Economist. Note: Breakdown by market value. Data as of June 30, 2023.

Source: Pitchbook LCD, Apollo Chief Economist

Source: ICE BofA, Bloomberg, Pitchbook LCD, Apollo Chief Economist. Note: Ticker used for HY is H0A0 Index and for IG it is C0A0 Index and for Loans it is SPBDALB Index.

Source: Bloomberg, Apollo Chief Economist

Source: ICE BofA, Bloomberg, Apollo Chief Economist. Note: Unweighted average spreads of bonds from ICE 5-10 Year US Banking Index, C6PX Index for bonds issued before Jan 1, 2023. There are 8 banks in the Regional index and 41 banks in the Diversified index. Regional banks include BankUnited Inc, Citizens Financial Group, Huntington Bancshares Incorporated, Regions Financial Corporation, Truist Financial Corporation, Webster Financial Corp, Wintrust Financial Corp, and Zions. Diversified banks include JP Morgan, Citibank, Bank of America, etc.

Source: Bloomberg, Apollo Chief Economist. Note: Tickers used HYG US Equity and LQD US Equity.

Source: FINRA Trace, Bloomberg, Apollo Chief Economist

Source: Bloomberg, Apollo Chief Economist

Source: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

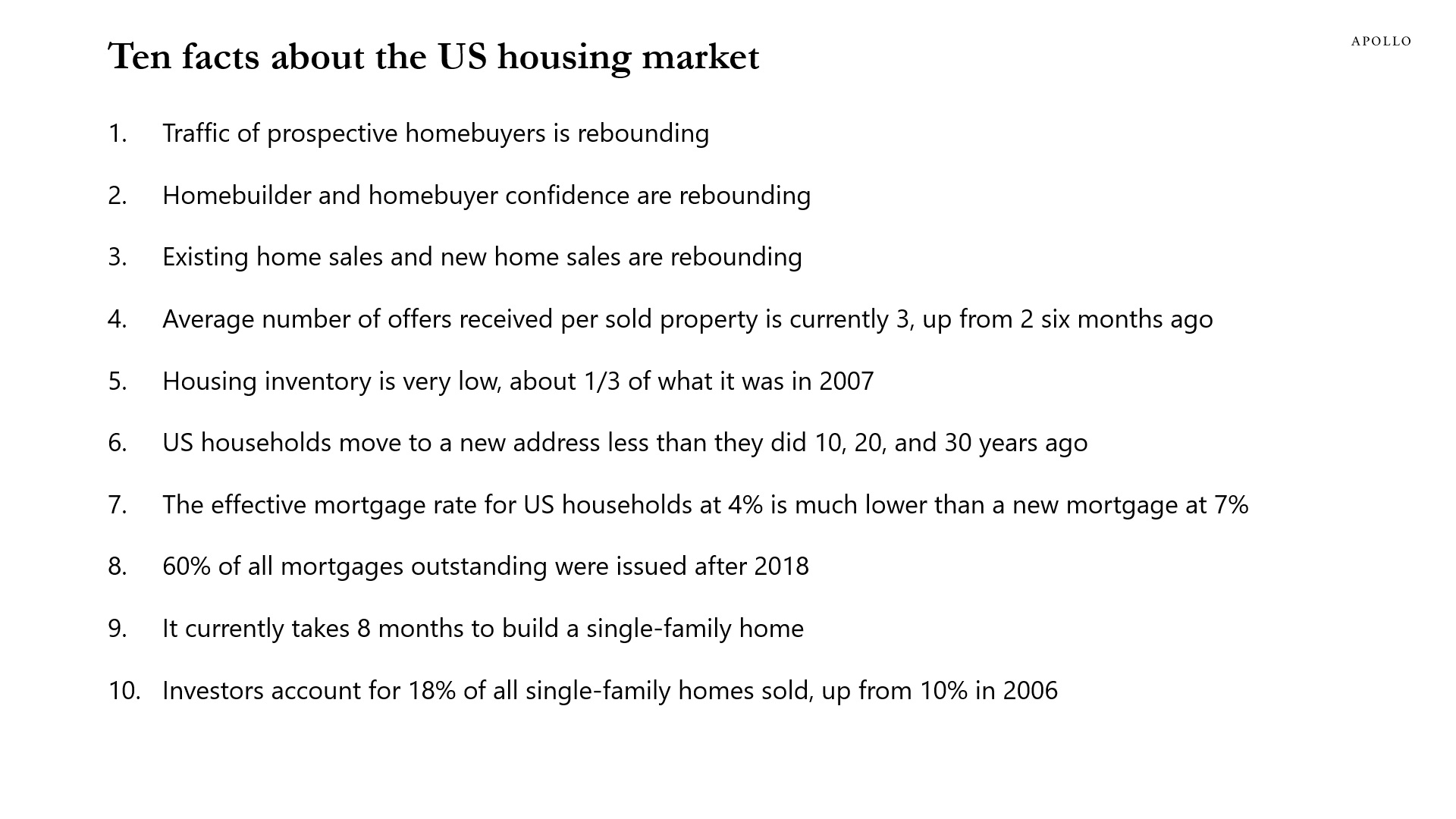

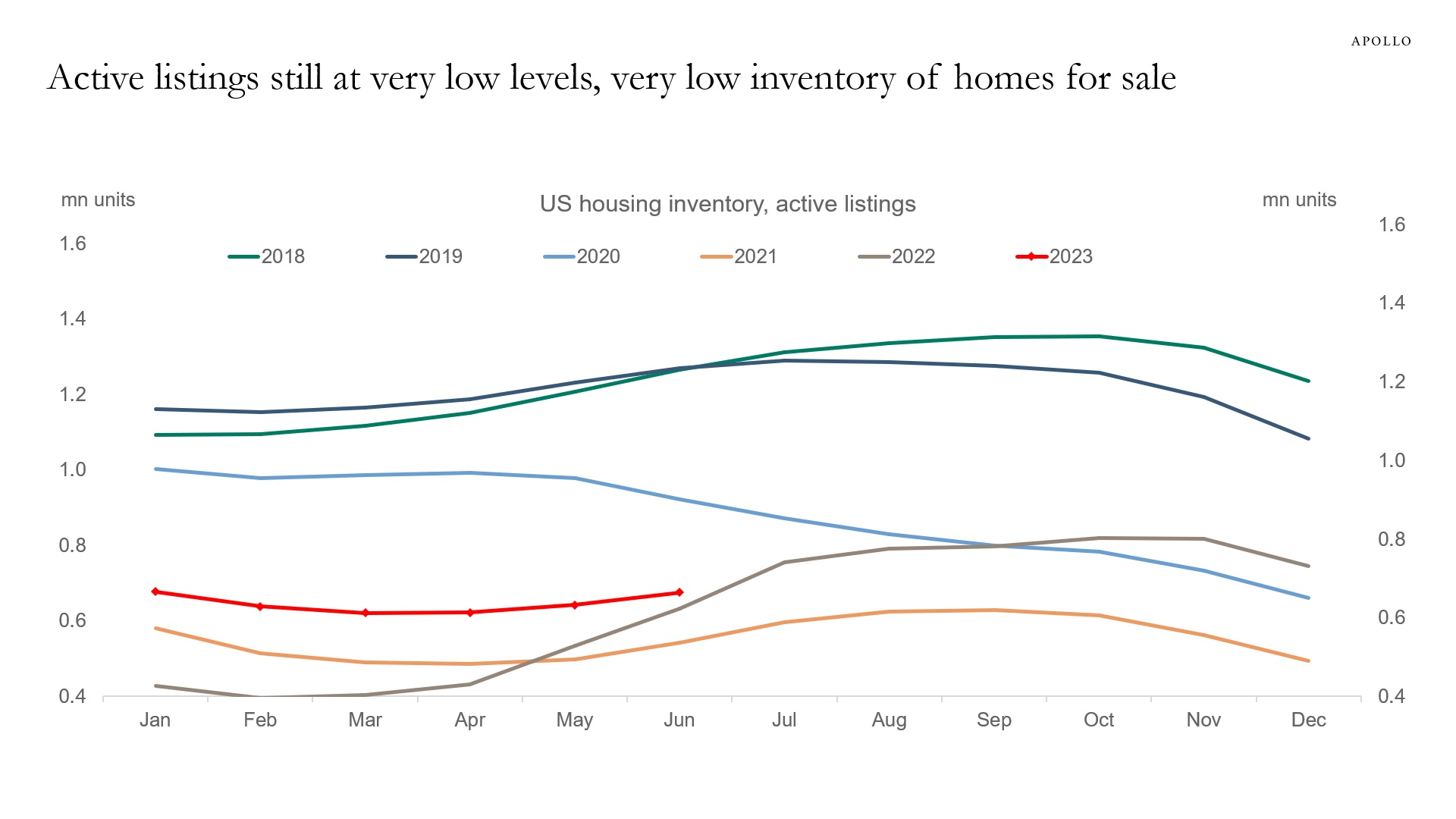

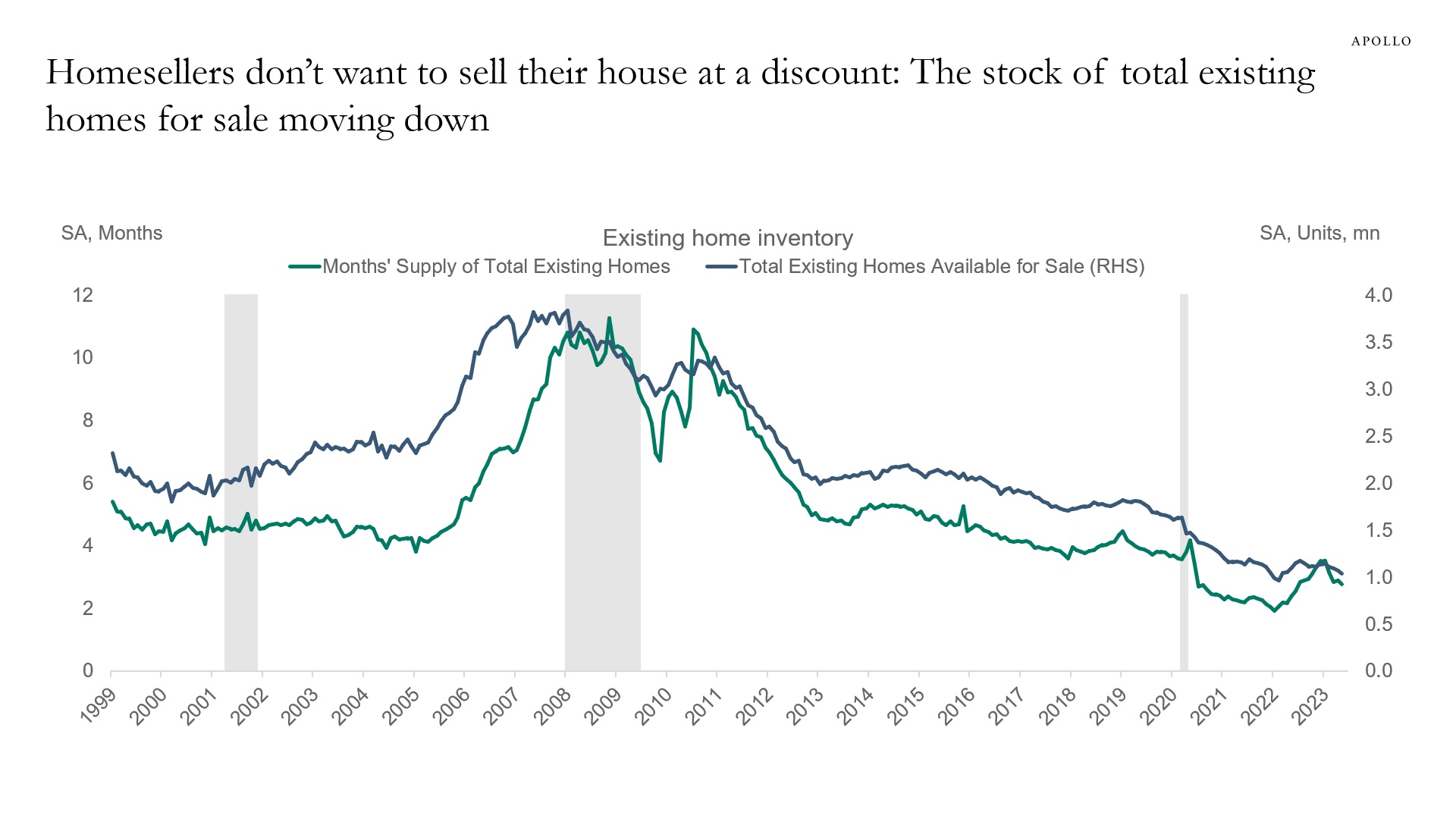

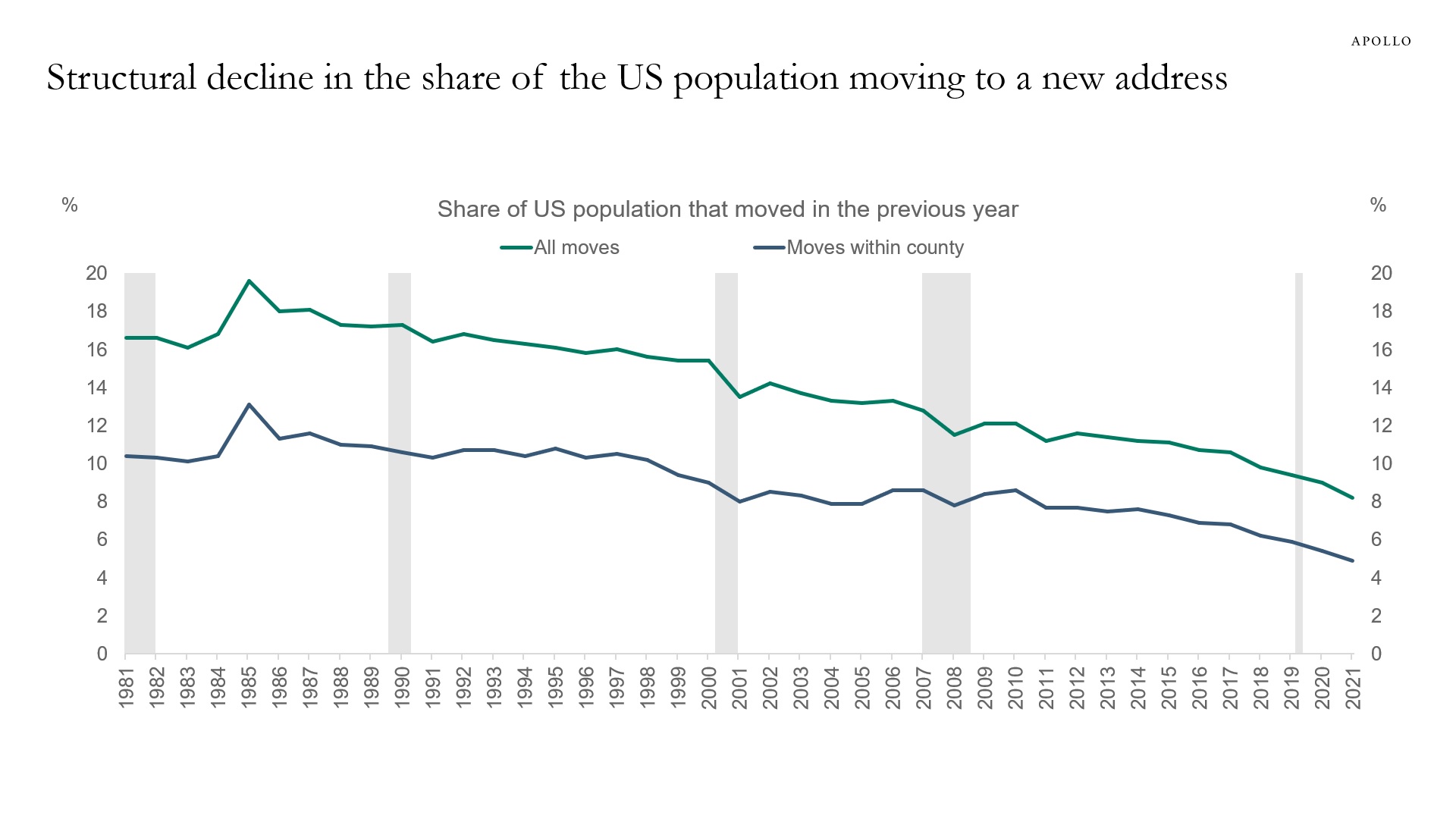

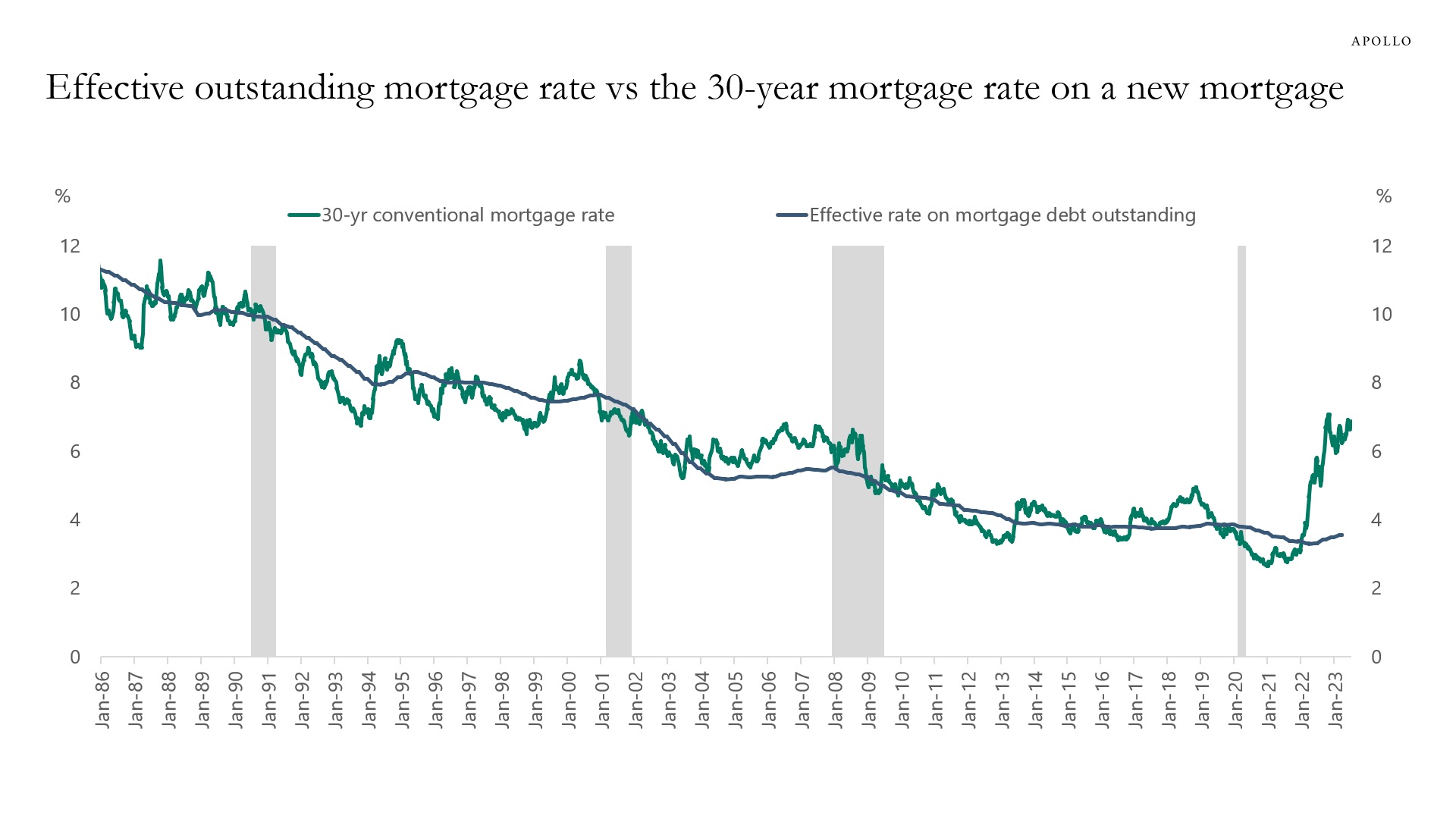

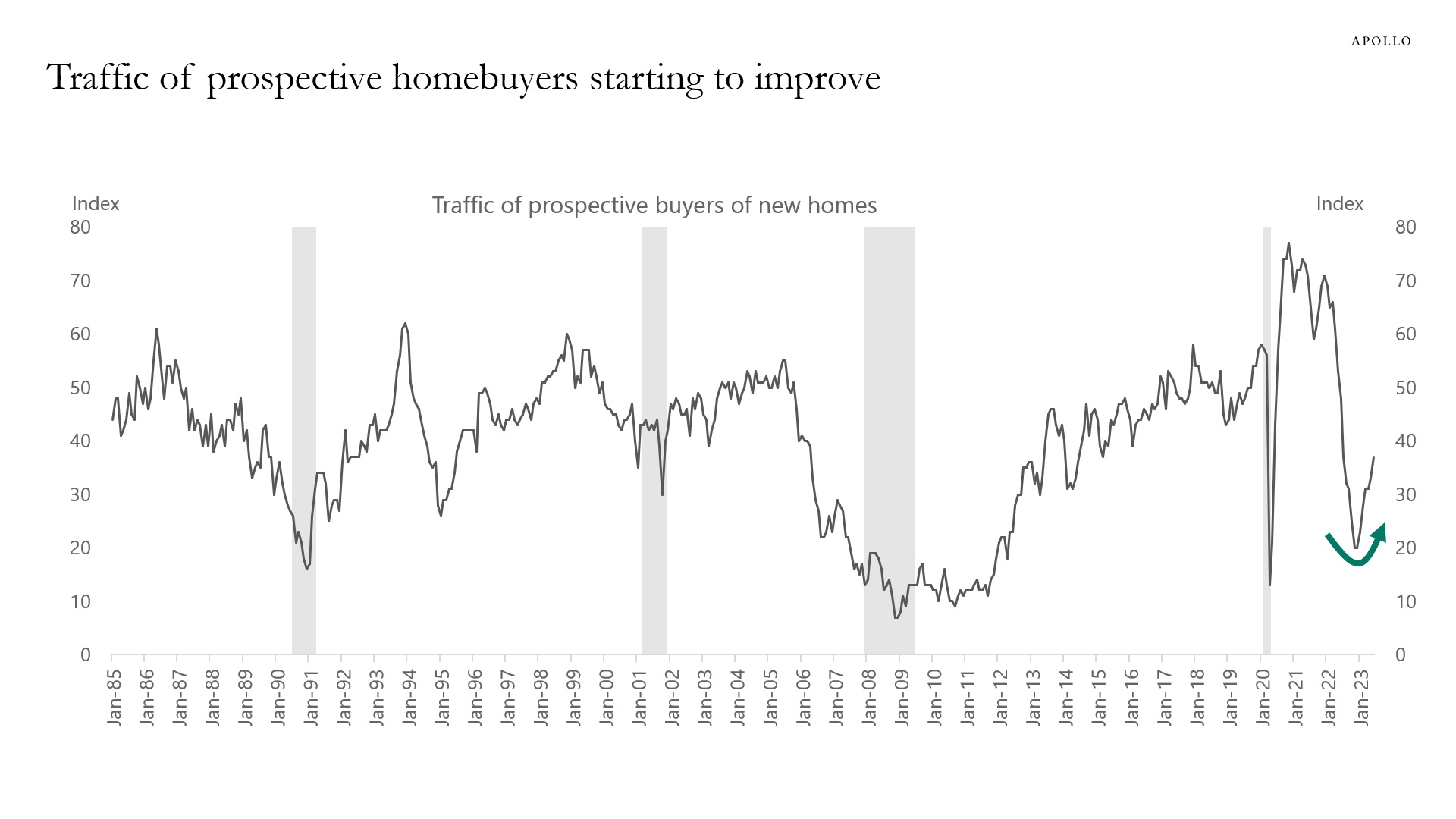

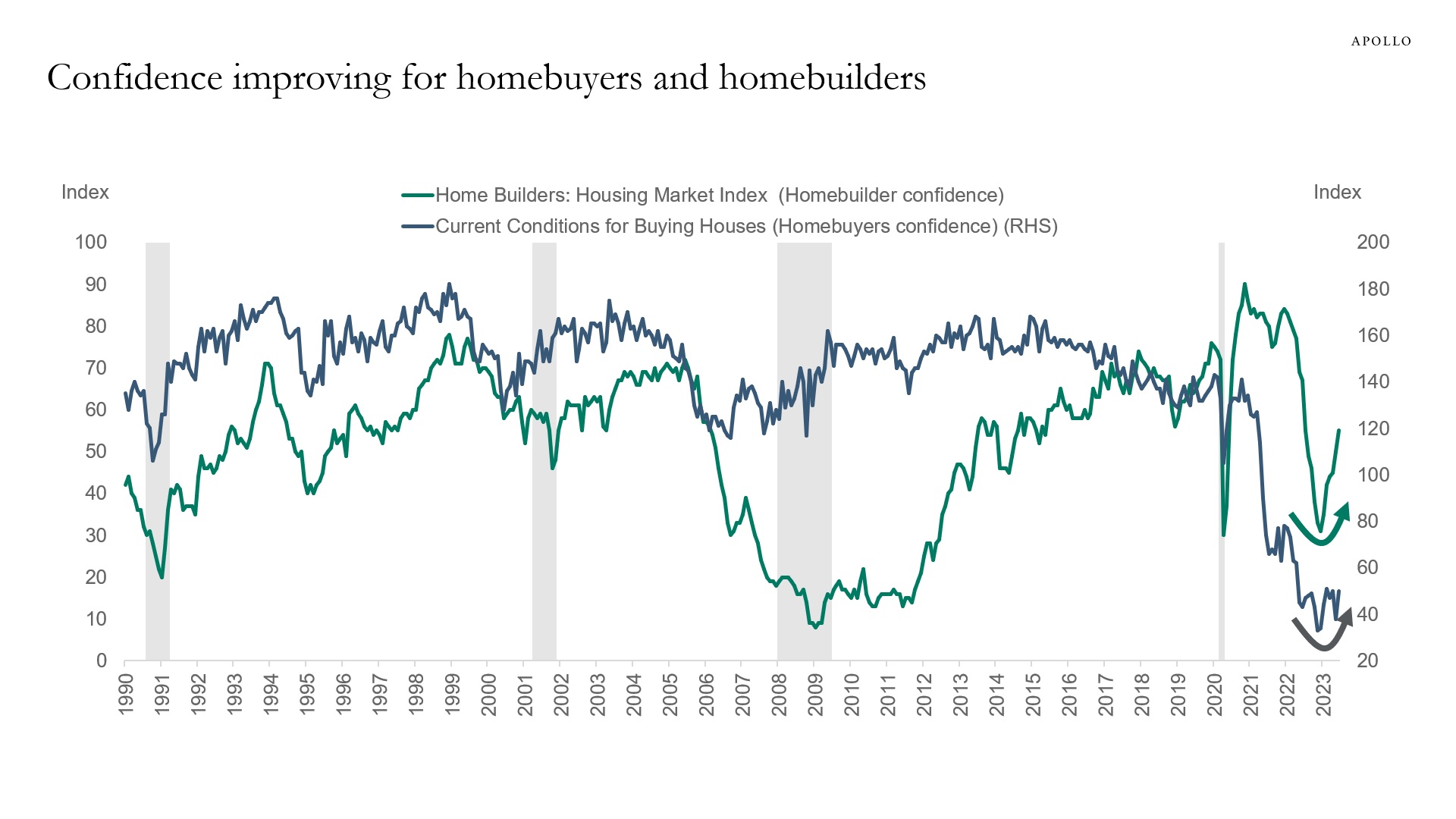

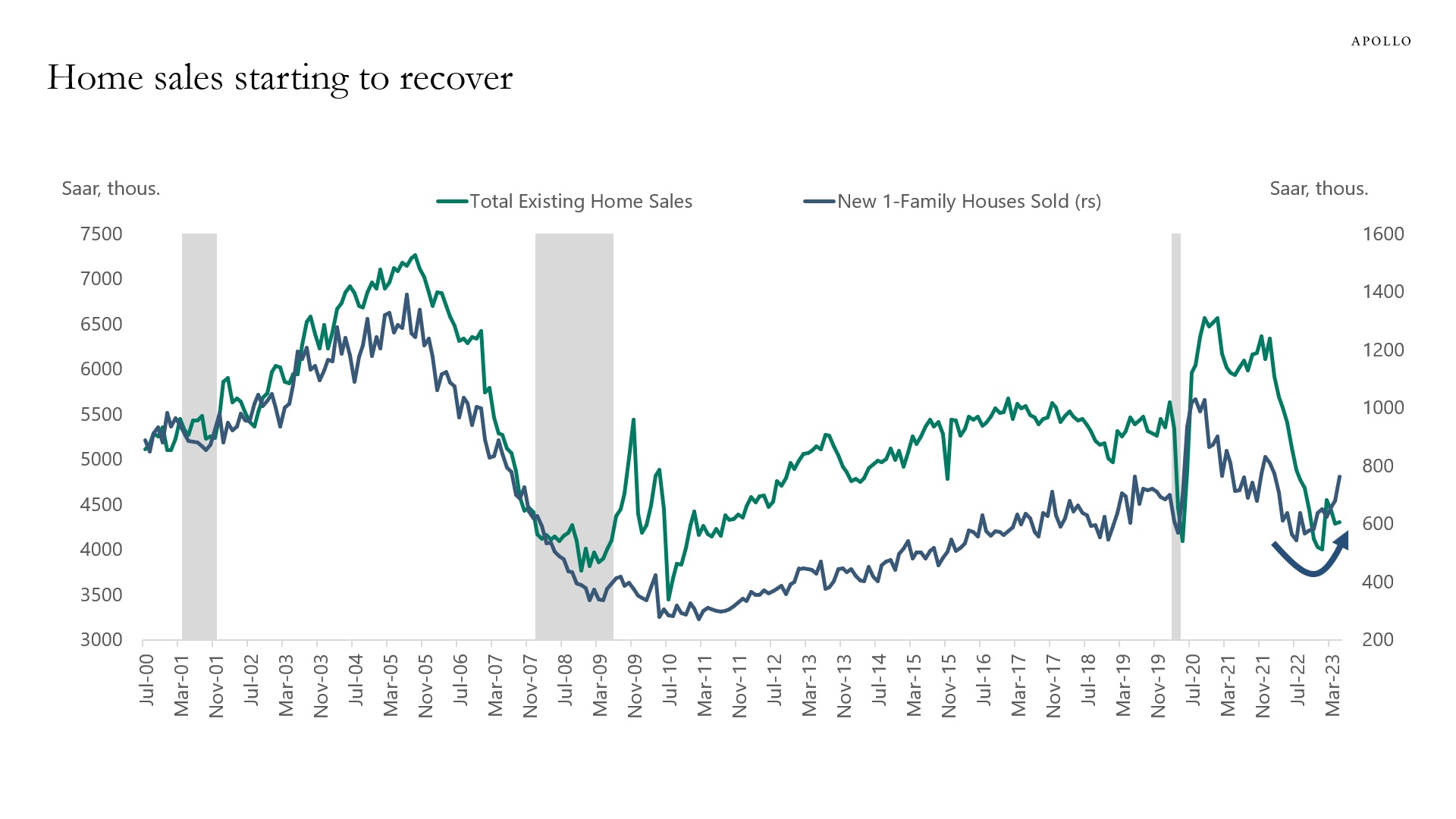

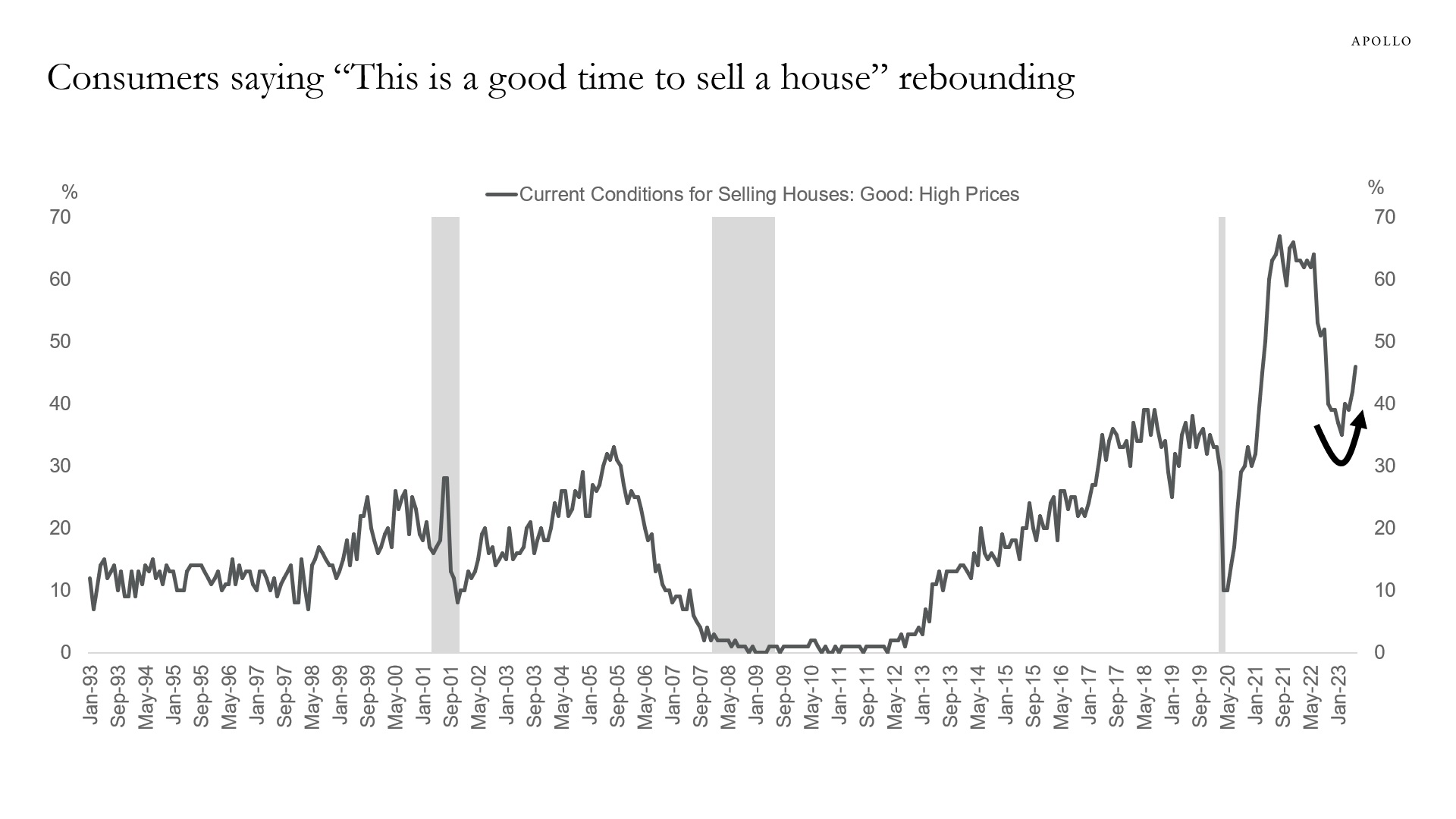

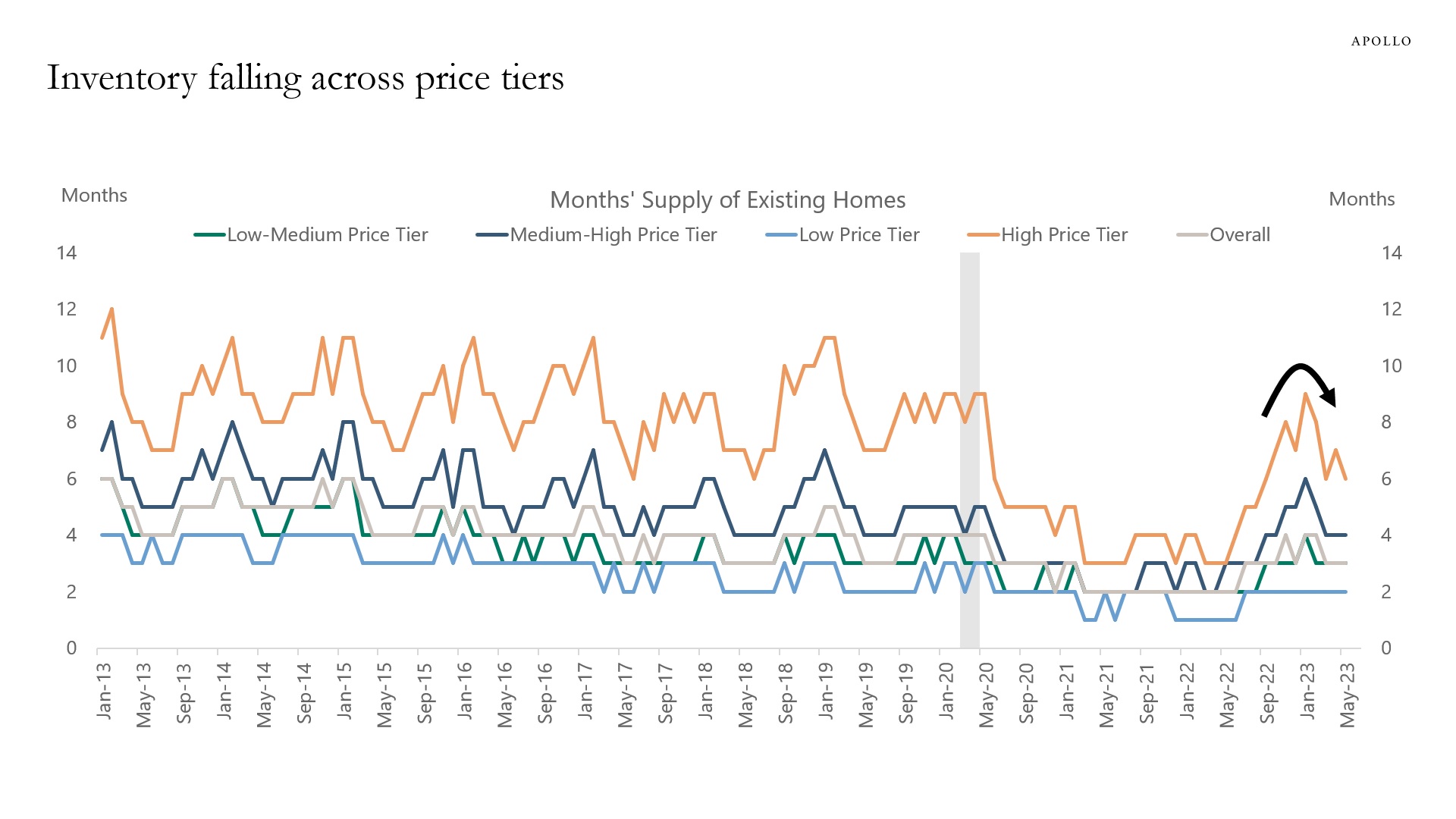

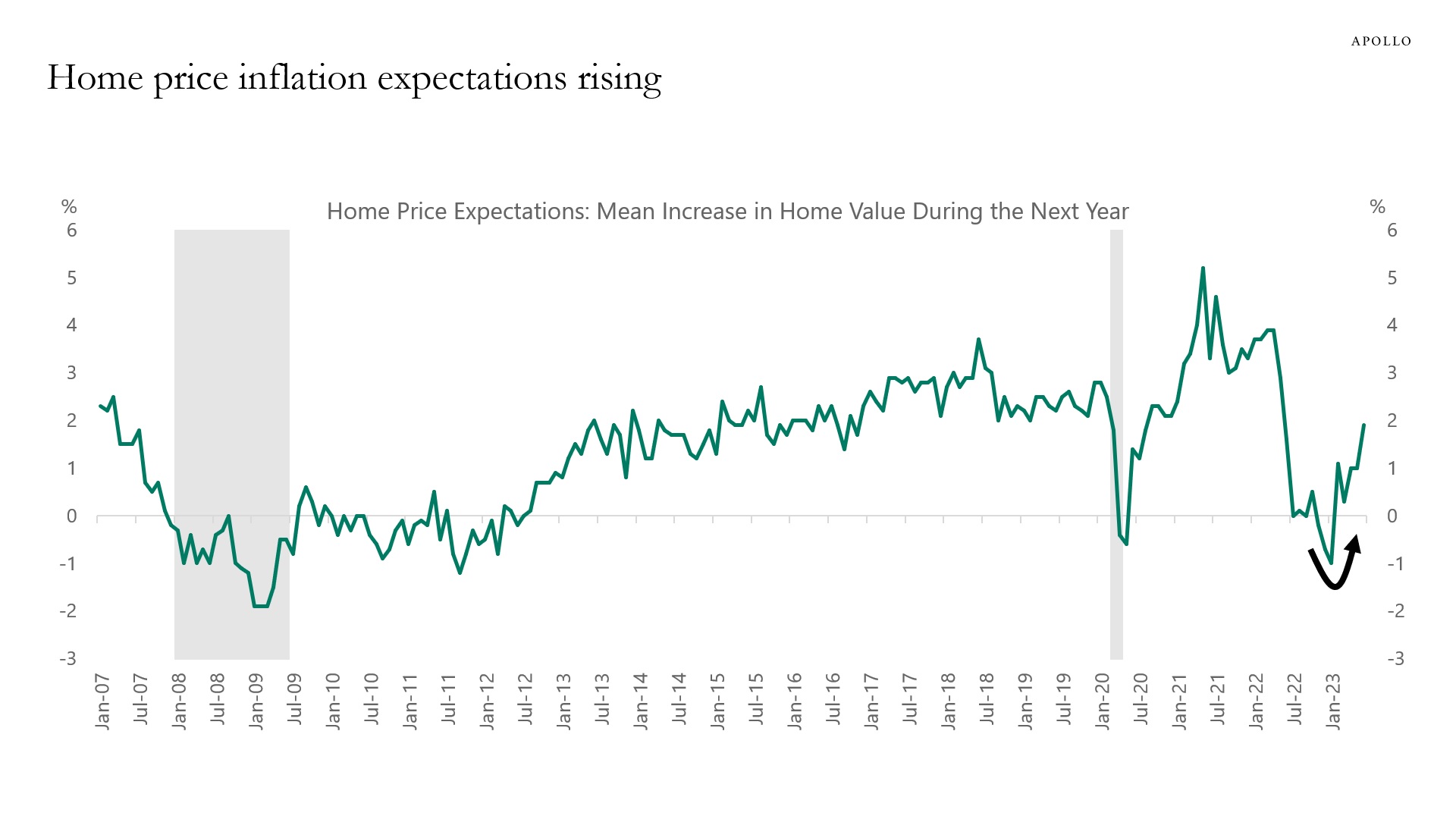

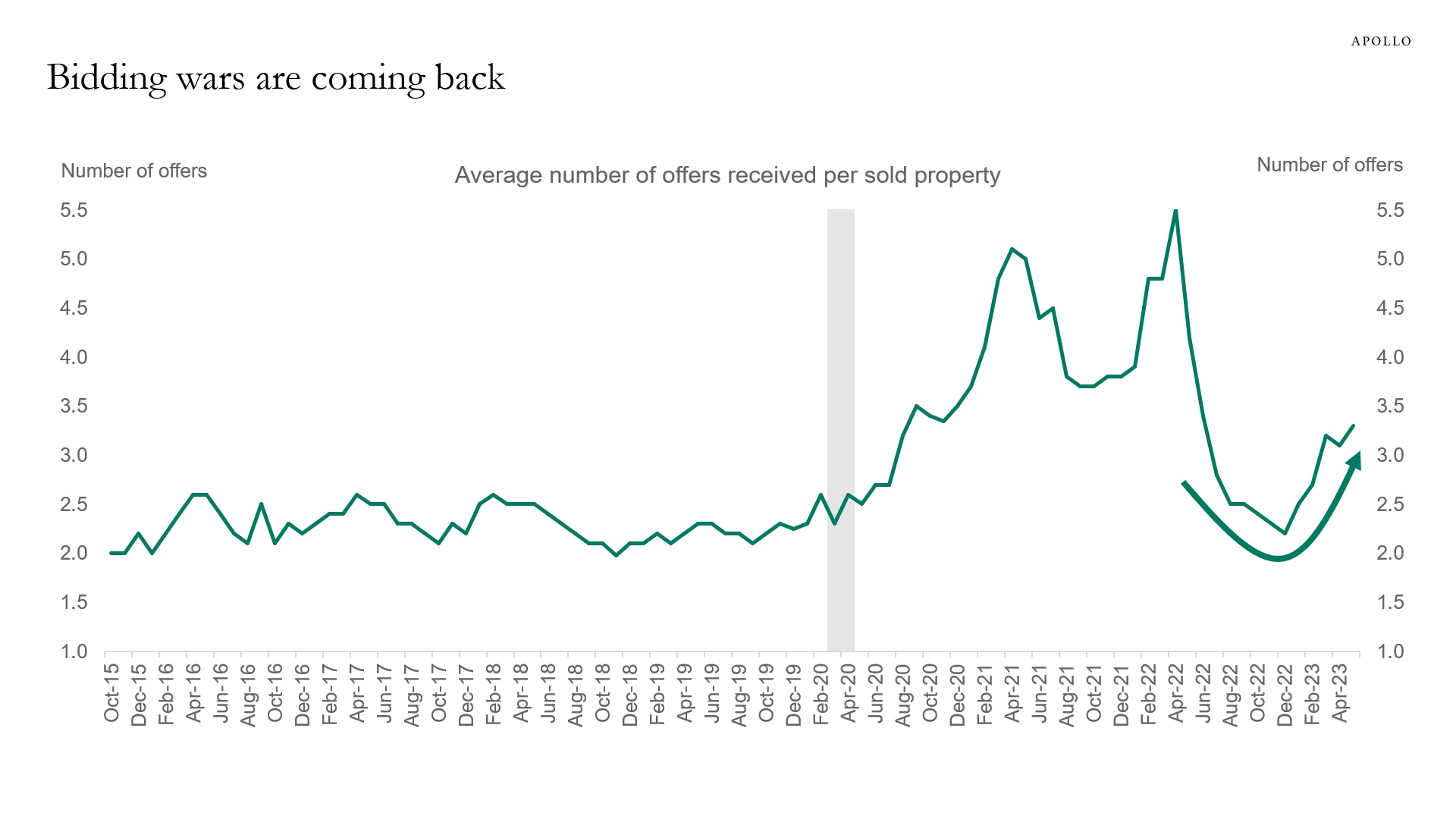

The housing market is recovering, see charts below and this presentation. With core inflation at 5%, this is a problem for the Fed because it will ultimately put upward pressure on housing inflation and make overall inflation more sticky. Maybe the Fed needs not only a softer labor market but also a softer housing market to achieve its goal of getting inflation back to 2%.

Source: Apollo Chief Economist

Source: Realtor.com, Apollo Chief Economist

Source: NAR, Apollo Chief Economist

Source: Census CPS, Apollo Chief Economist

Source: Freddie Mac, BEA, Bloomberg, Apollo Chief Economist. The effective interest rate (%) reflects the amortization of initial fees and charges over a 10-year period, which is the historical assumption of the average life of a mortgage loan.

Source: National Association of Homebuilders, Bloomberg, Apollo Chief Economist

Source: University of Michigan, NAHB, Haver Analytics, Apollo Chief Economist

Source: Census Bureau, NAR, Haver, Apollo Chief Economist; Forecast is Bloomberg consensus.

Source: University of Michigan, Apollo Chief Economist

Source: American Enterprise Institute, Haver, Apollo Chief Economist

Source: University of Michigan, Haver Analytics, Apollo Chief Economist

Source: NAR, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

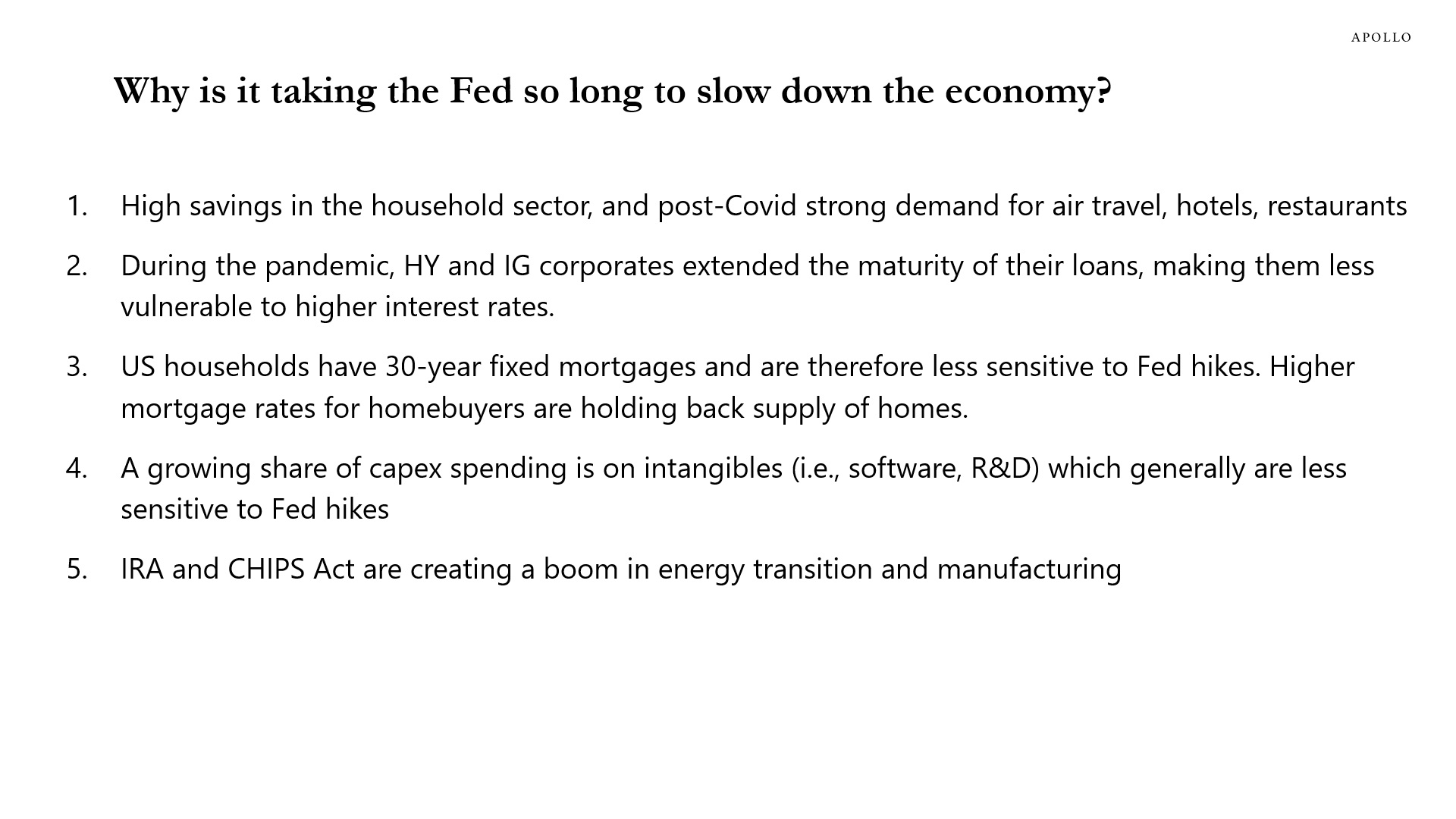

There are cyclical, structural, and policy reasons why the US economy continues to be so strong, see chart below.

The Fed is pressing harder and harder on the brakes, and some indicators are starting to soften in the background, see also the Daily Spark yesterday.

But we are not there yet. The economic data is slowing down and inflation is slowing down. But core inflation is still too high and sticky at 5%.

As a result, the Fed will continue to step on the brakes until they get what they want, namely slower growth and slower inflation.

But the harder the Fed steps on the brakes, the higher the likelihood that we will see a sudden stop in bank lending, capital markets issuance, consumer spending, capex spending, or a correction in financial markets.

Source: Apollo Chief Economist See important disclaimers at the bottom of the page.

-

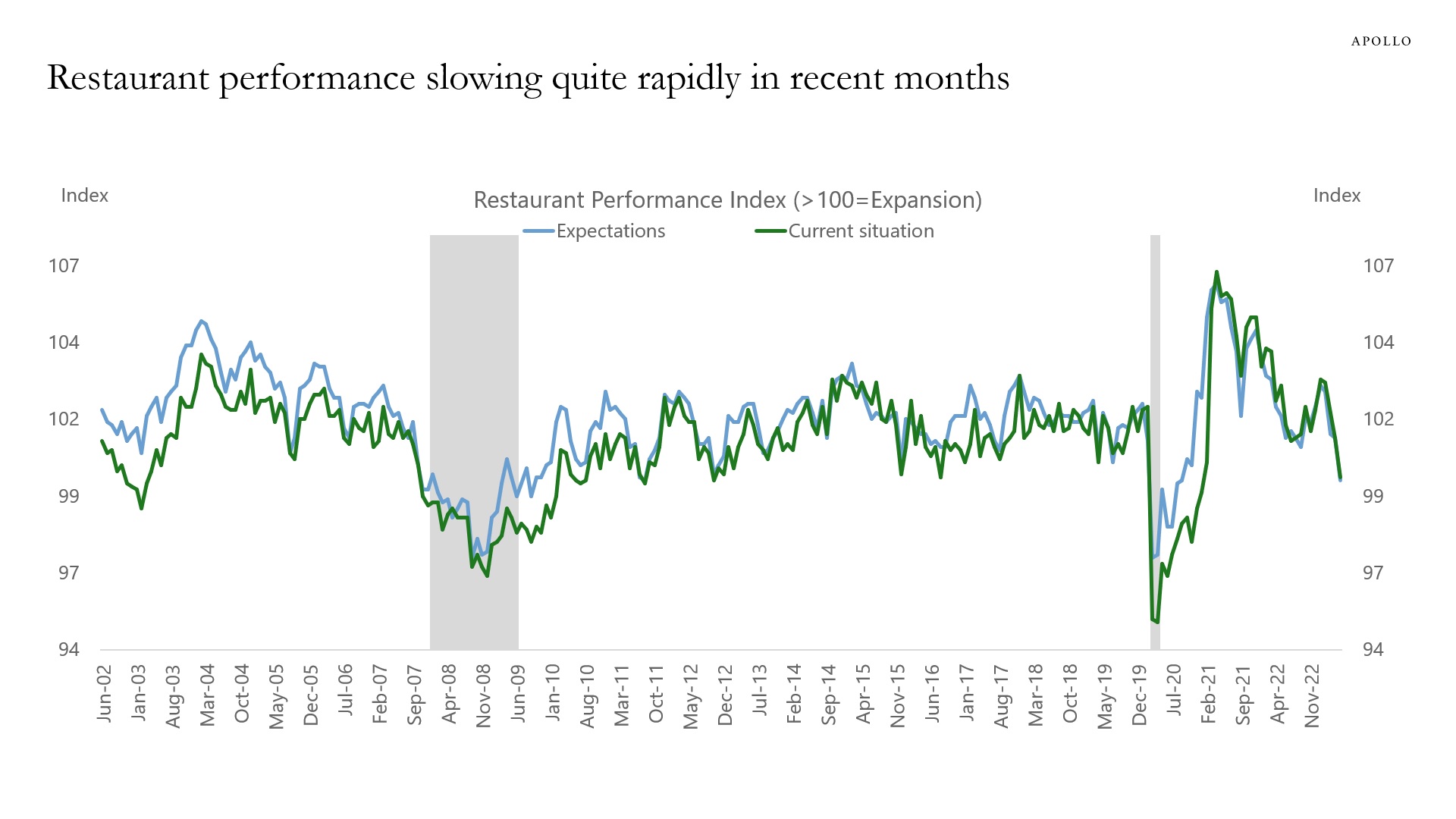

Just when everyone is abandoning the recession call, the data starts to slow down.

1) The Restaurant Performance Index has sharply declined in recent months, see the first chart below.

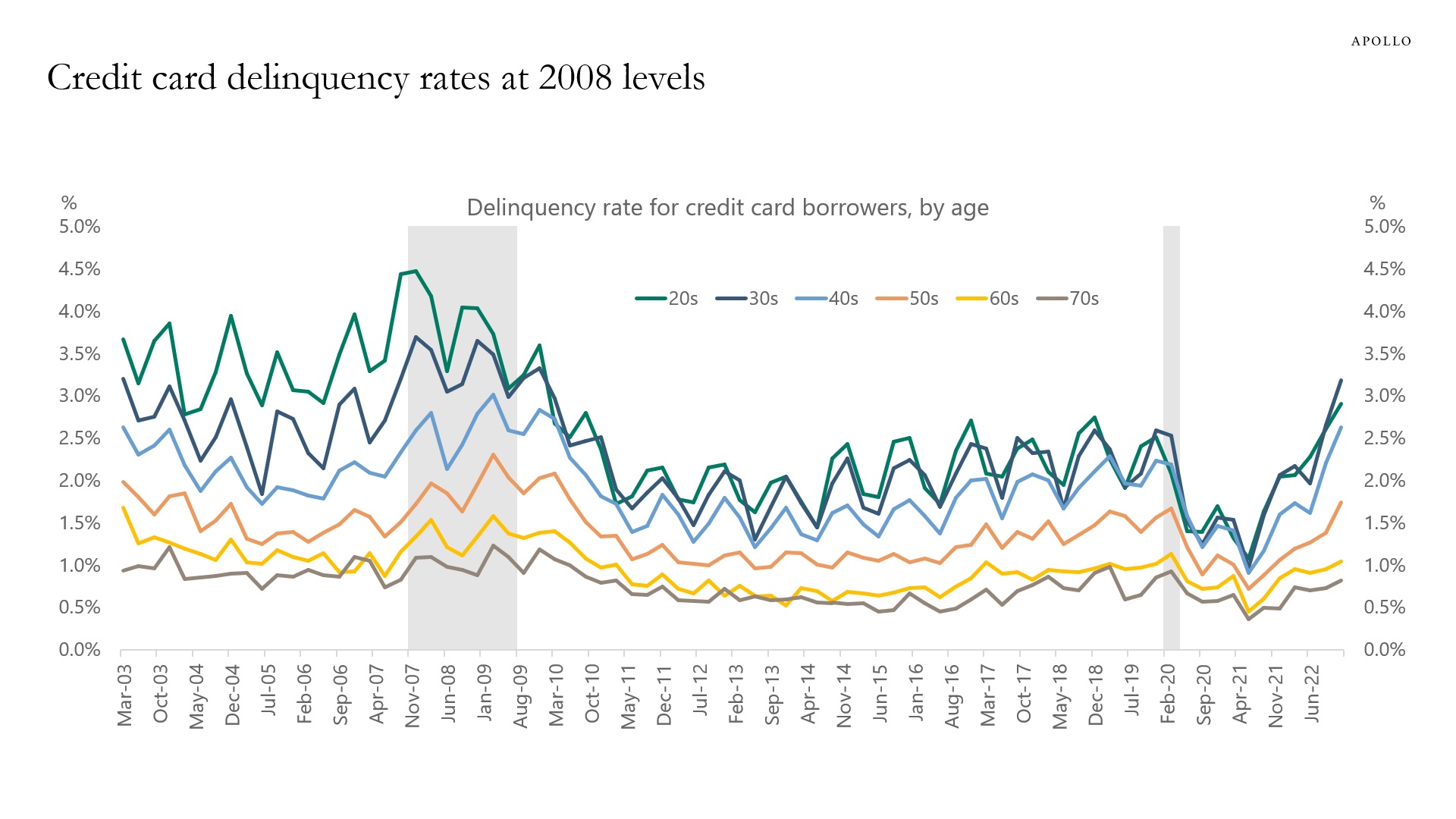

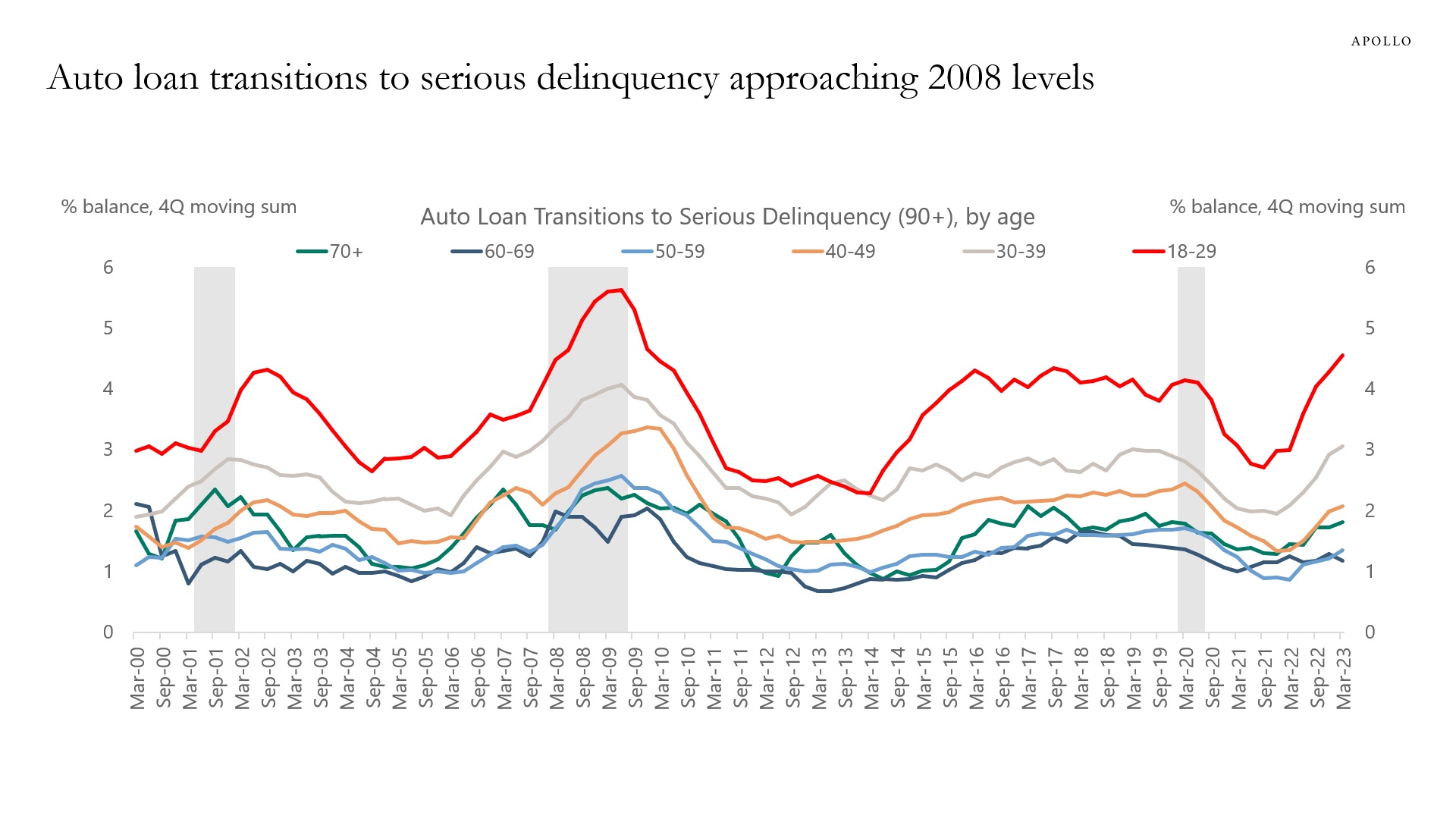

2) Credit card and auto loan delinquencies continue to rise, and these trends will continue with the Fed on hold well into next year; see the second and third charts.

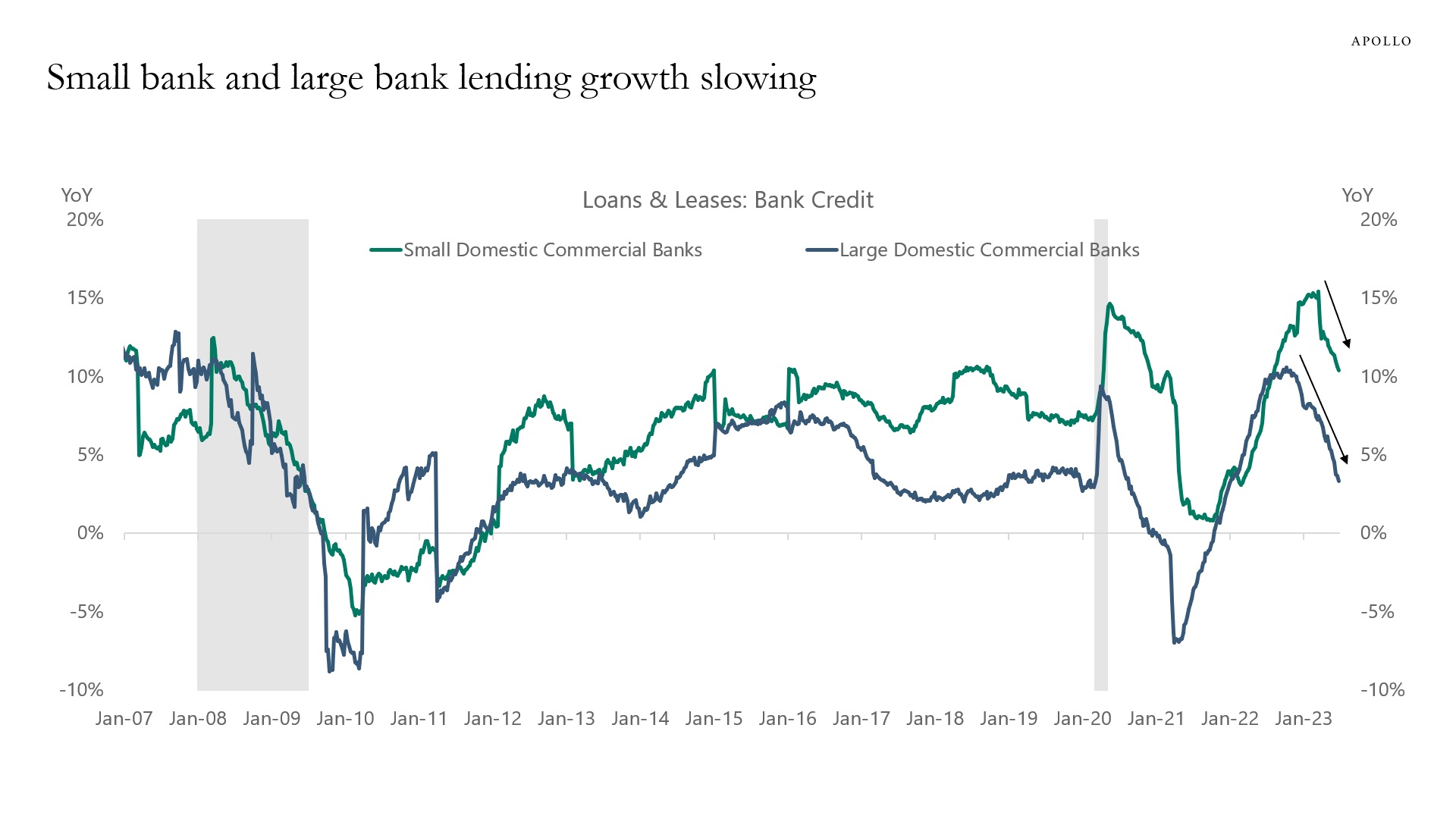

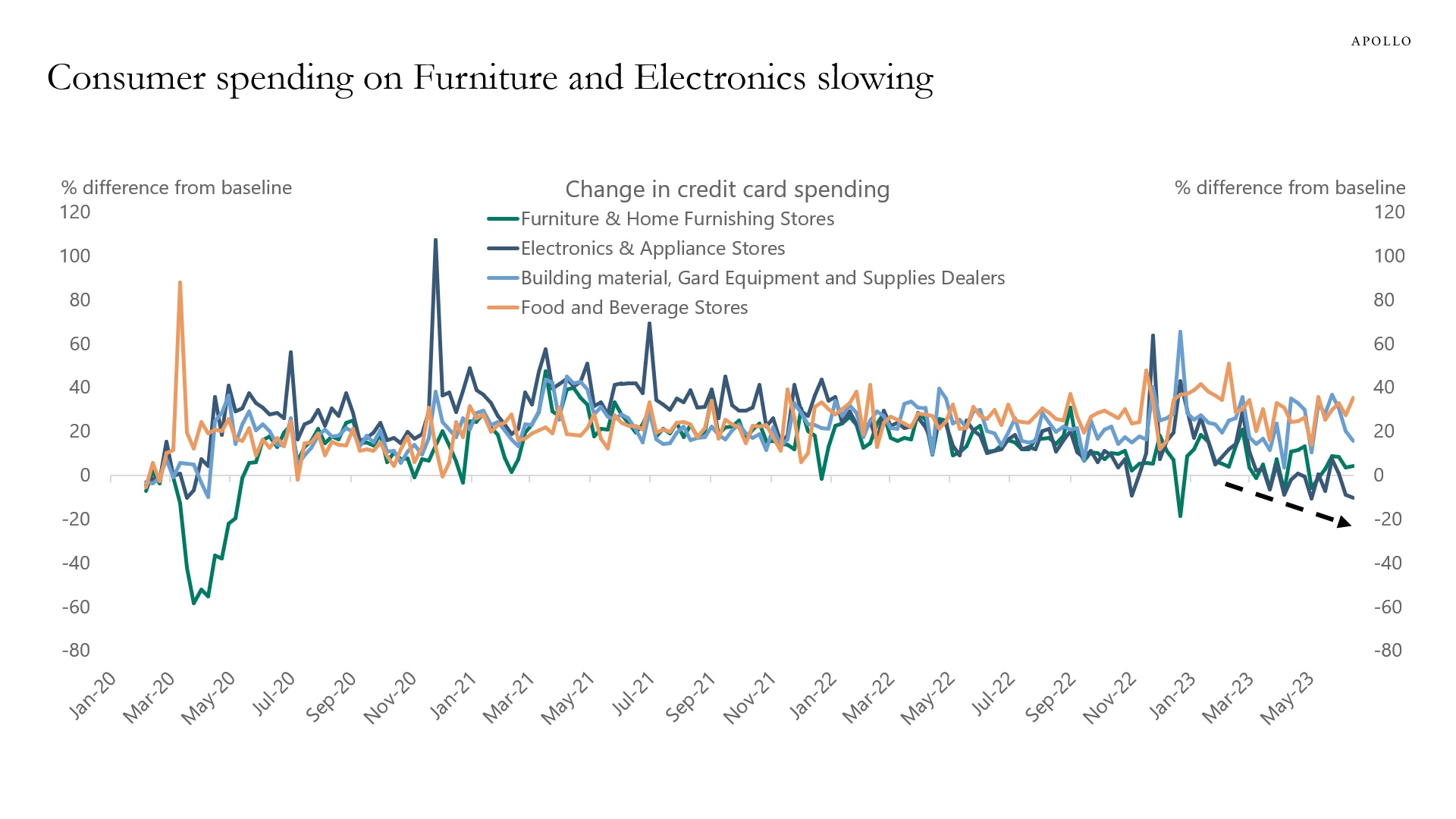

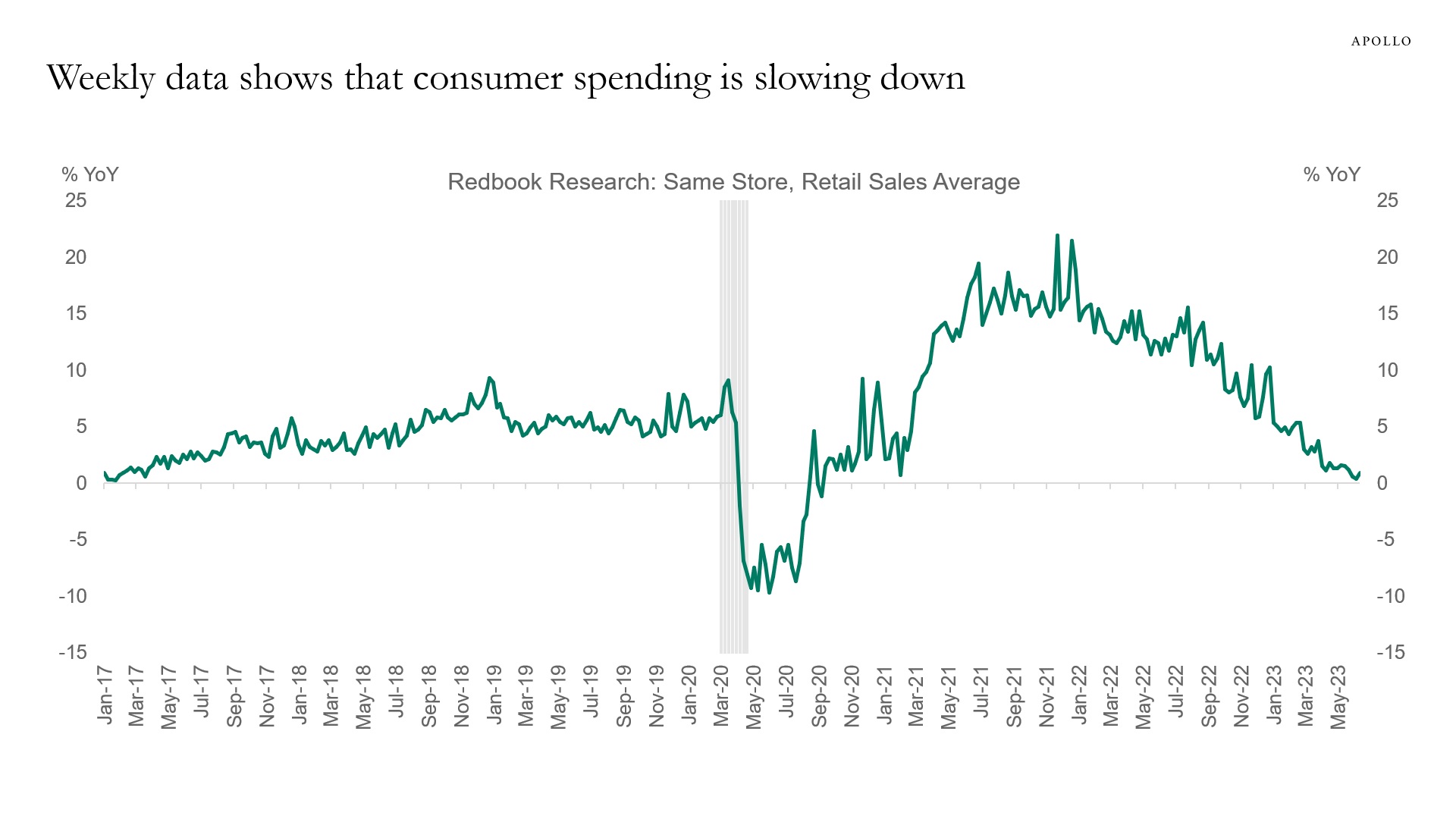

3) Weekly data for bank lending is slowing rapidly, and weekly credit card data shows that consumer spending on durables that require financing, such as furniture and electronics, is slowing, see the fourth and fifth charts.

The bottom line is that Fed hikes are starting to negatively impact consumer spending, as also shown in the weekly data in the sixth chart.

Weaker consumer spending is not surprising. The whole idea from the Fed raising interest rates is to slow down growth and ultimately inflation.

Source: National Restaurant Association, Haver, Apollo Chief Economist

Source: New York Fed Consumer Credit Panel / Equifax, Apollo Chief Economist

Source: FRBNY Consumer Credit Panel, Equifax, Haver Analytics, Apollo Chief Economist

Source: Federal Reserve Board, Haver Analytics, Apollo Chief Economist.

Source: BEA, Haver Analytics, Apollo Chief Economist. Note: The weekly values represent the predicted percentage difference from the typical level of spending (prior to the pandemic declared by the World Health Organization on March 11, 2020) after adjusting for day-of-week, month, and year effects, based on daily data. The typical level corresponds to a value of zero.

Source: Redbook, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

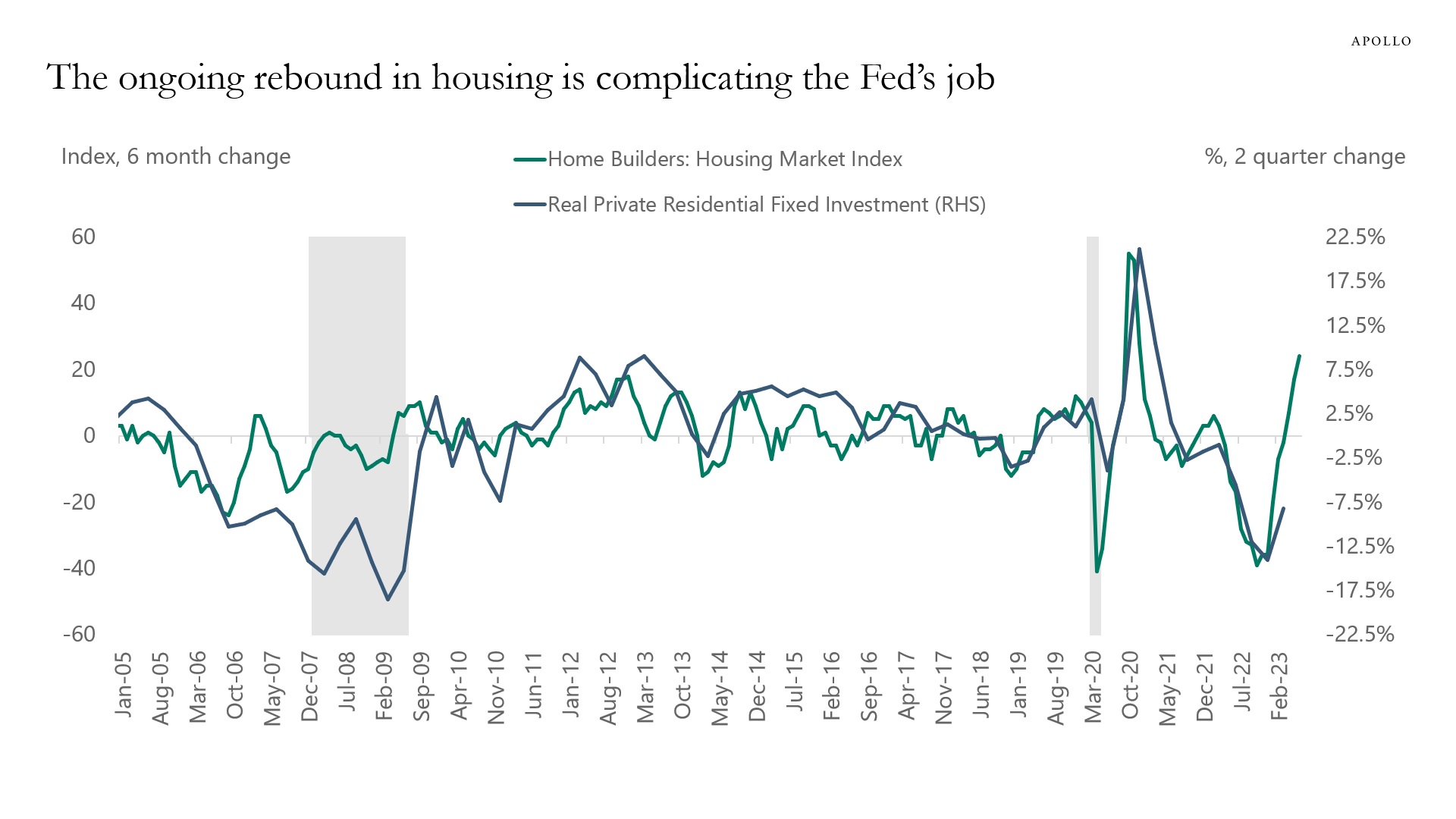

The ongoing rebound in the housing market is putting upward pressure on growth and inflation at a time when the Fed is trying to slow down growth and inflation, see chart below.

Source: BEA, NAHB, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

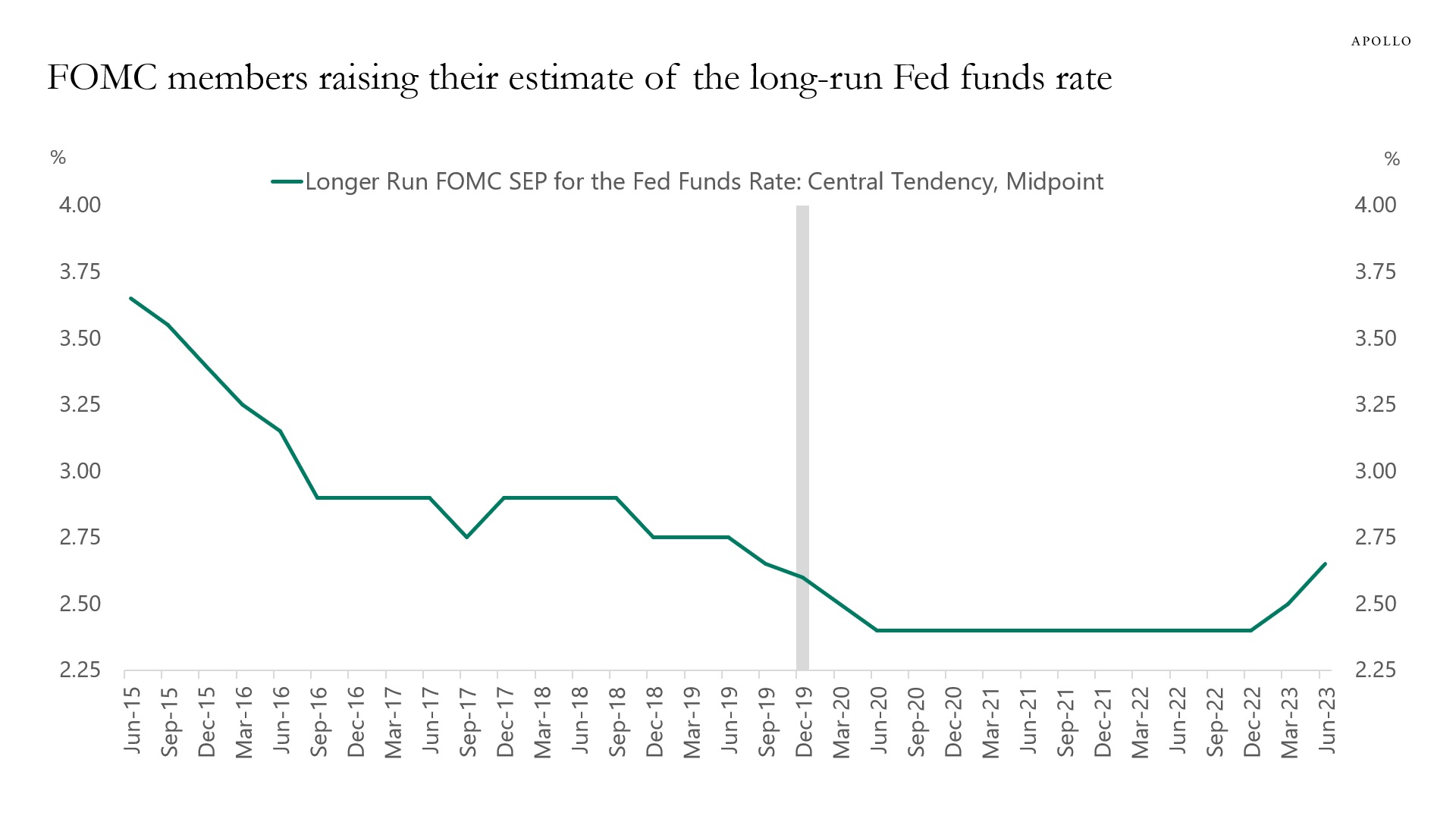

The Fed has started to increase its estimate of the long-run Fed funds rate, see chart below. The implication is that the Fed is beginning to see the costs of capital as permanently higher. A permanent increase in the risk-free rate has important implications for investors.

Source: FRB, Apollo Chief Economist See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.