Want it delivered daily to your inbox?

-

We have updated our attached daily and weekly indicators for the US economy, and the daily data for airline travel, consumer mobility, and restaurant bookings are still not showing signs of a slowdown.

The weekly data for hotel occupancy rates is also solid, and weekly jobless claims continue to decline, suggesting that the labor market is still strong. Weekly data for cinema visits is also strong, and so is the weekly data for bank lending and the weekly data for credit and debit card usage.

There are some early signs of weakness in the housing market, with the weekly data for listings starting to trend higher in recent weeks. Traffic of prospective home buyers is also starting to come down.

At the anecdotal level, there are more sound bites about layoffs in tech and startups, but these anecdotes are not yet visible in the macro data.

The bottom line is that the economy is still strong, and the Fed needs to tighten financial conditions further to slow growth and inflation.

See important disclaimers at the bottom of the page.

-

The employment report confirms the Fed narrative that the economy is still strong and more rate hikes are needed. But the report also shows that wage inflation has peaked, allowing the Fed to turn less hawkish as we enter the third quarter. For more, download the PDF.

See important disclaimers at the bottom of the page.

-

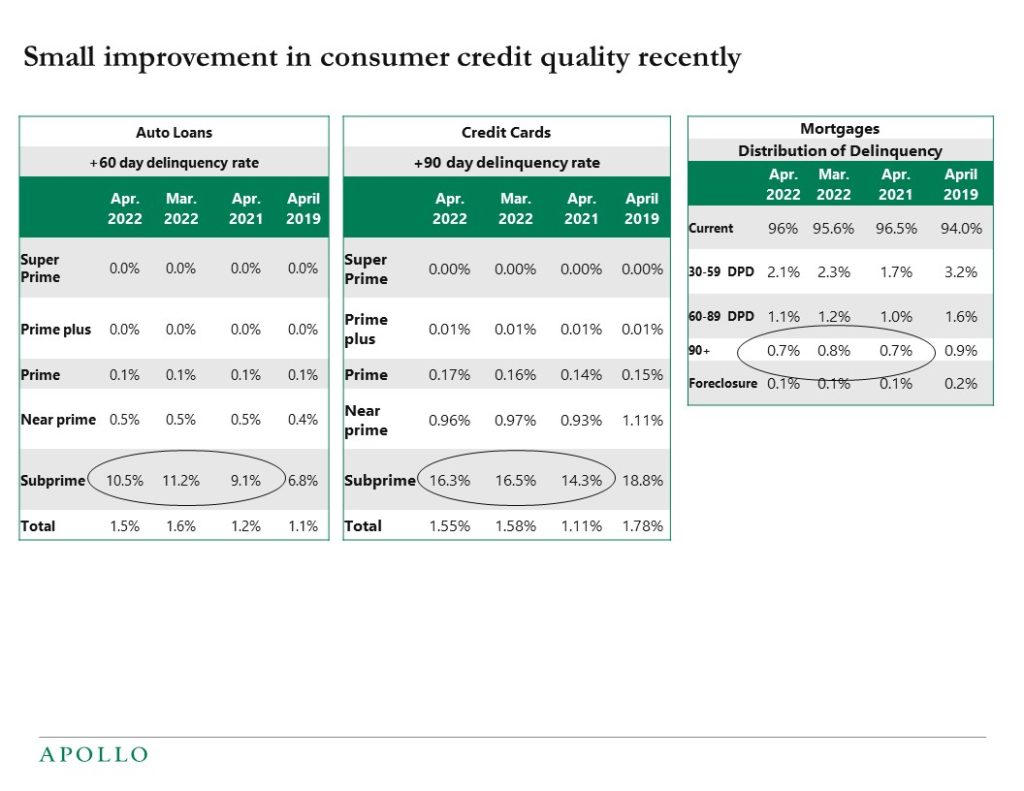

After a brief period of rising delinquency rates on credit cards and auto loans for subprime borrowers, the latest data shows a modest improvement in consumer credit quality with delinquency rates falling, see table below. This is consistent with a strong labor market, high wage growth, and a high level of household savings. US consumer spending will eventually grow at a slower pace because this is what the Fed wants to see, but the bottom line is that there are no signs yet in the macro data of the US consumer slowing down.

Source: Transunion Monthly Industry Snapshot See important disclaimers at the bottom of the page.

-

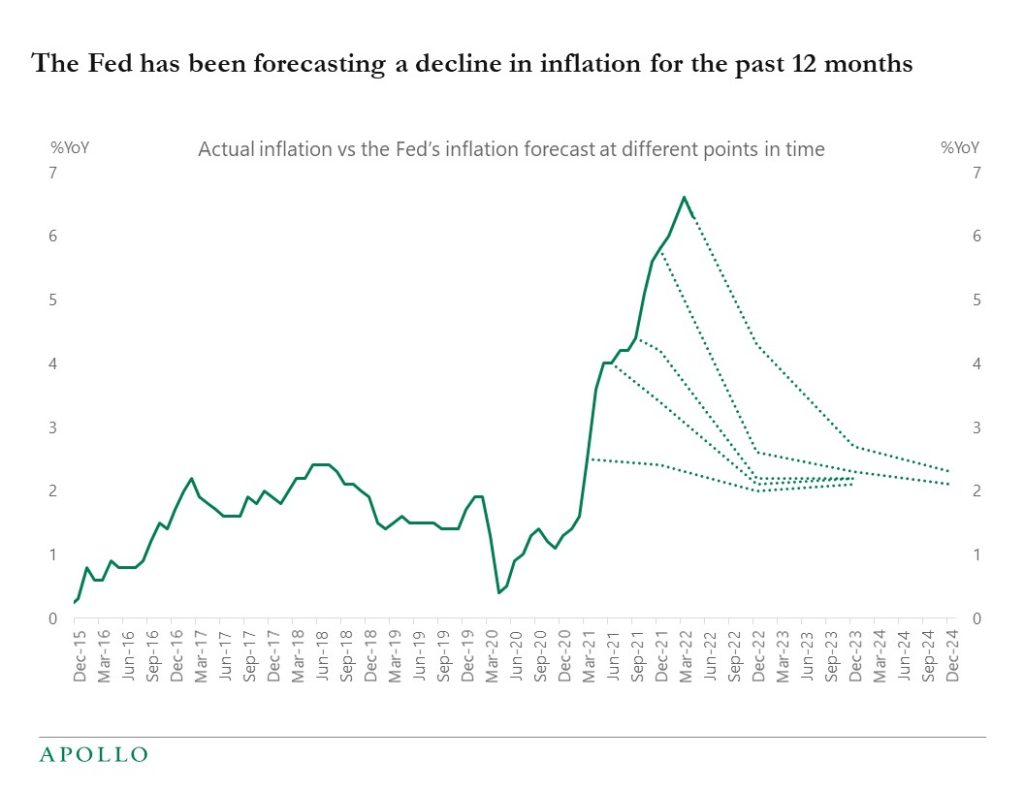

The Fed and markets continue to expect a quick reversal in inflation back to the Fed’s 2% target, see chart below. This raises two questions for investors: As the Fed destroys demand to cool down inflation, what level of the unemployment rate is required to achieve this path, and can the Fed engineer a soft landing without increasing the unemployment rate too much and thereby triggering a recession?

Source: Bloomberg, Fed’s Statement of Economic Projections, Apollo Chief Economist. Note: Headline PCE inflation shown. See important disclaimers at the bottom of the page.

-

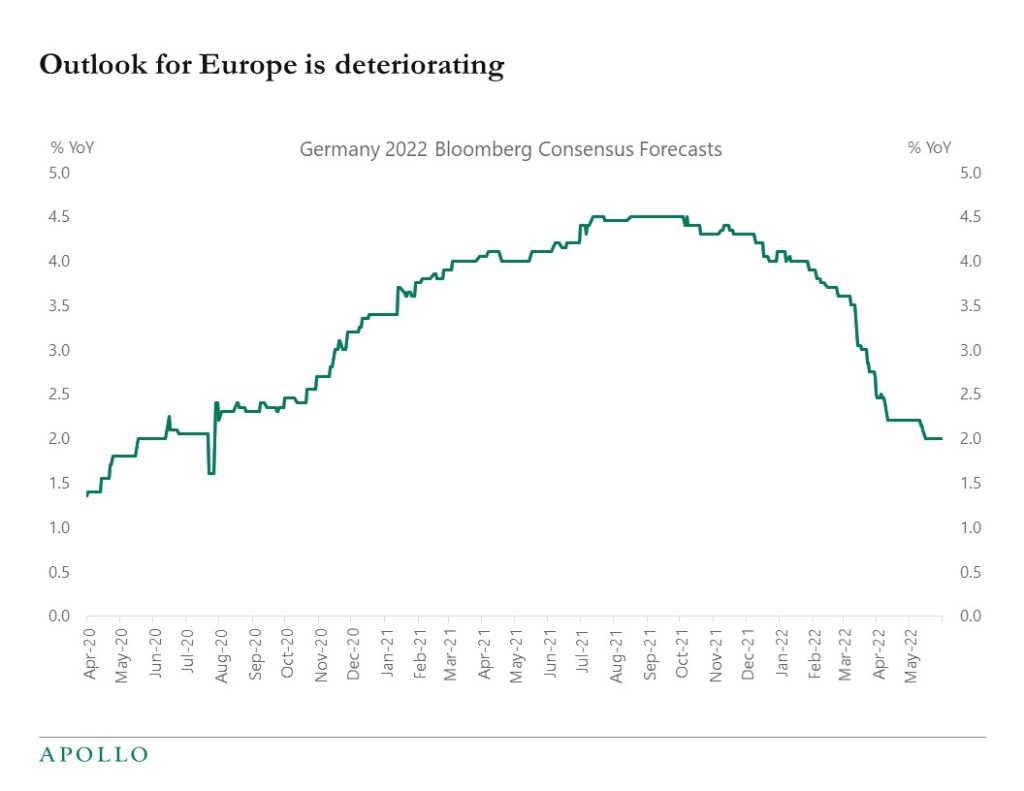

The consensus continues to downgrade growth expectations for Europe, raising questions about ECB rate hikes and the rising risk of loan losses and defaults in Europe, see chart below.

Source: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

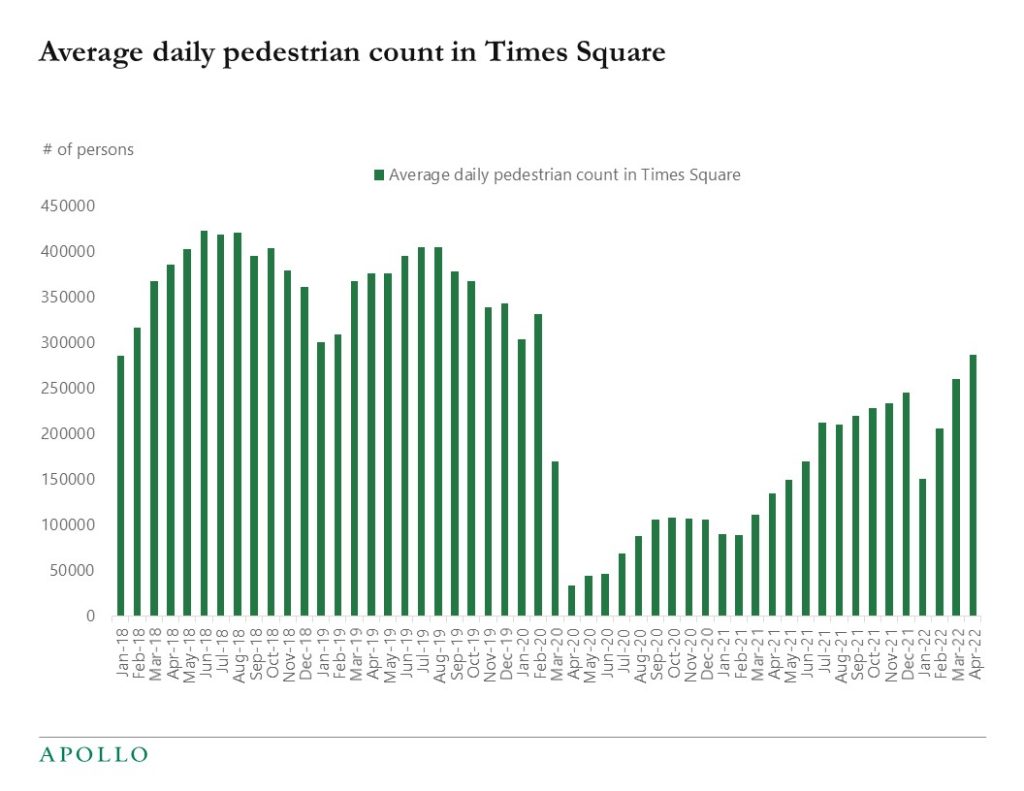

There is more pedestrian traffic in Times Square, but current levels are still 25% below normal, see chart below.

Source: timessquarenyc.com, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

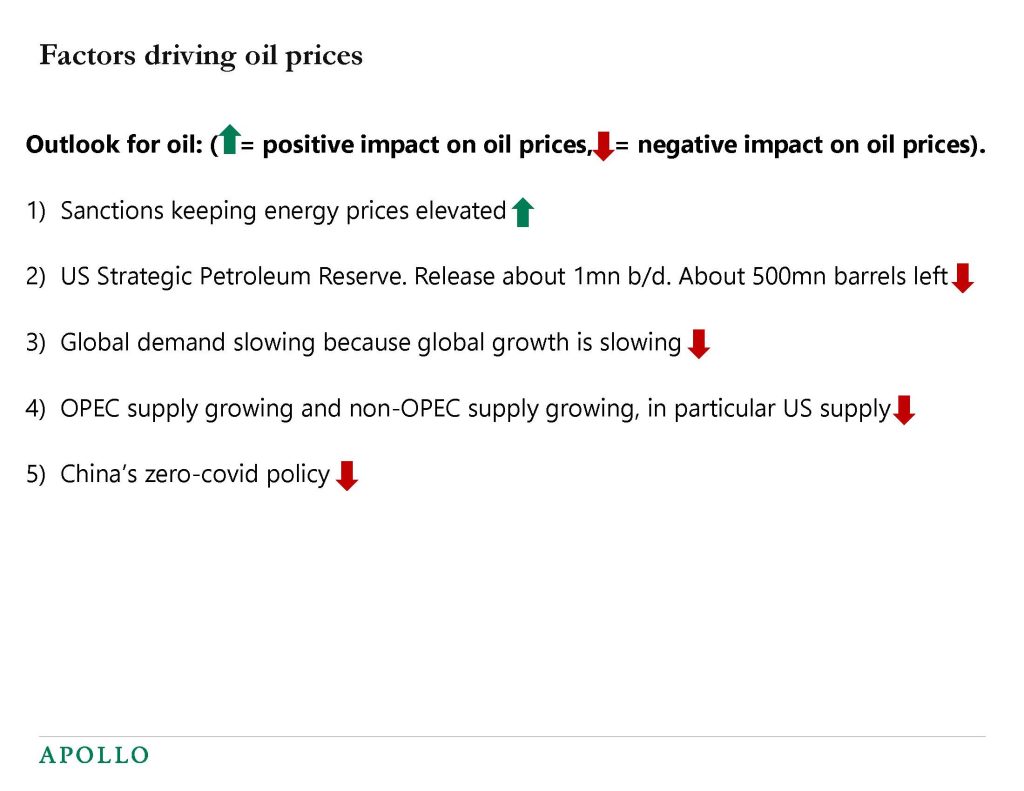

We updated our oil price forecasting model, and while sanctions continue to argue for higher oil prices, the downward pressure is significant from the Strategic Petroleum Reserve release, growing supply, and slowing global growth. As a result, our econometric model points to lower oil prices over the coming 18 months, see charts below.

Source: Apollo Chief Economist See important disclaimers at the bottom of the page.

-

U.S. Retirement Assets: Amount in Pensions and IRAs

https://crsreports.congress.gov/product/pdf/IF/IF12117Reactions of household inflation expectations to a symmetric inflation target and high inflation

https://www.dnb.nl/media/2dzn0i2m/working_paper_no-_743.pdfRussia Sanctions and Cryptocurrencies: Policy Issues

https://crsreports.congress.gov/product/pdf/IN/IN11939See important disclaimers at the bottom of the page.

-

There are some very early signs that the economy is starting to cool down, with layoffs rising in startups and some housing indicators starting to roll over from high levels. But the big picture remains that high-frequency indicators show that the economy is still strong. Most noteworthy this week was the decline in jobless claims. The solid data is consistent with the consensus expectation of nonfarm payrolls coming in at 330K next week and the unemployment rate falling from 3.6% to 3.5%.

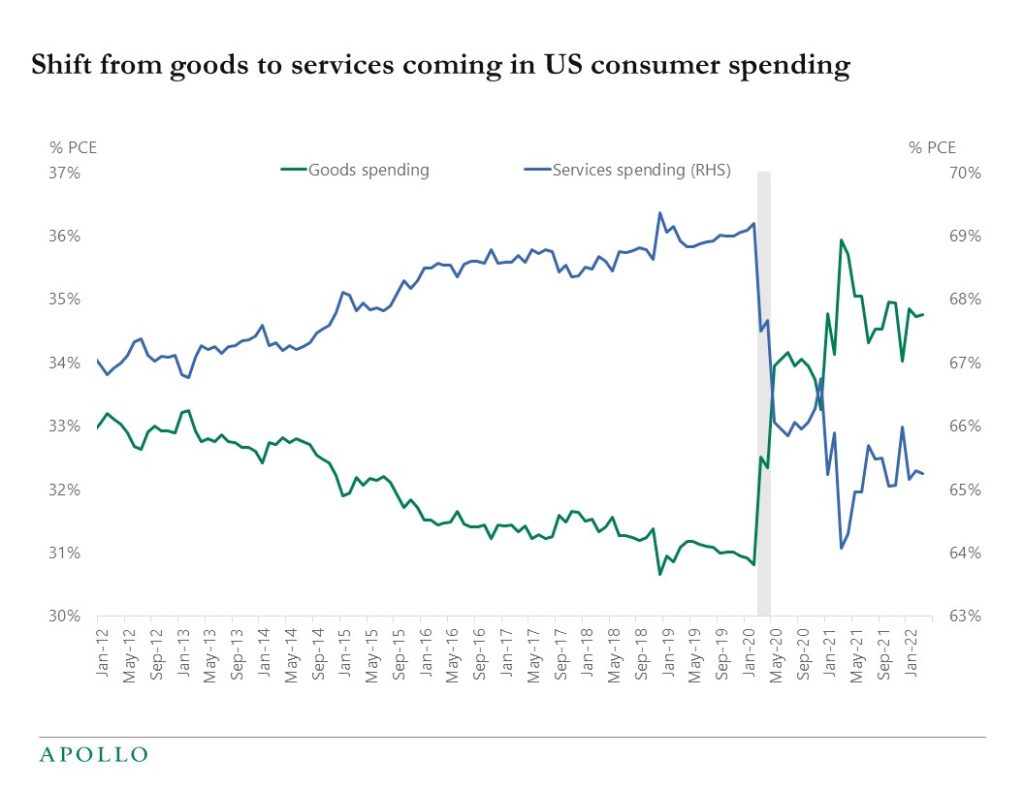

Looking ahead, with the virus subsiding, we should begin to see a shift away from goods toward services. The chart below shows that this shift has not started yet. The surprise has been that consumer goods spending has continued to be so strong. But with more people flying, eating at restaurants, staying at hotels, and going to amusement parks, we should over the coming quarters see growth in consumer services accelerate, and spending on consumer goods begin to slow down.

The trading implication for equity and credit markets is to be long consumer services and short consumer goods. For the Fed the implication is that rate hikes continue. Read our slowdown chart book.

Source: BEA, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

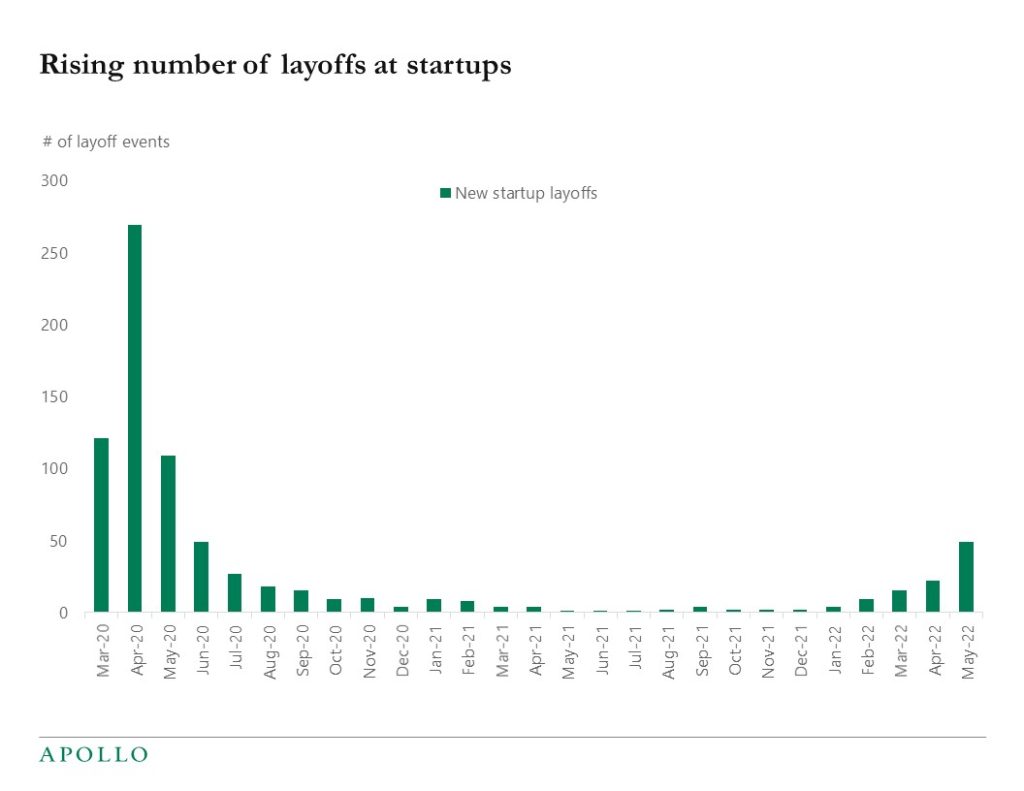

With tech and venture capital taking a severe hit, layoffs at startup companies have started to increase, see chart below. The Fed is trying to destroy demand, including demand for labor, and this is early evidence that they are succeeding.

Source: Layoffs.fyi, Apollo Chief Economist. Note: Top 5 sectors that account for layoffs in May 2022: Transportation, Food, Travel, Finance, and Real Estate. See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.