Want it delivered daily to your inbox?

-

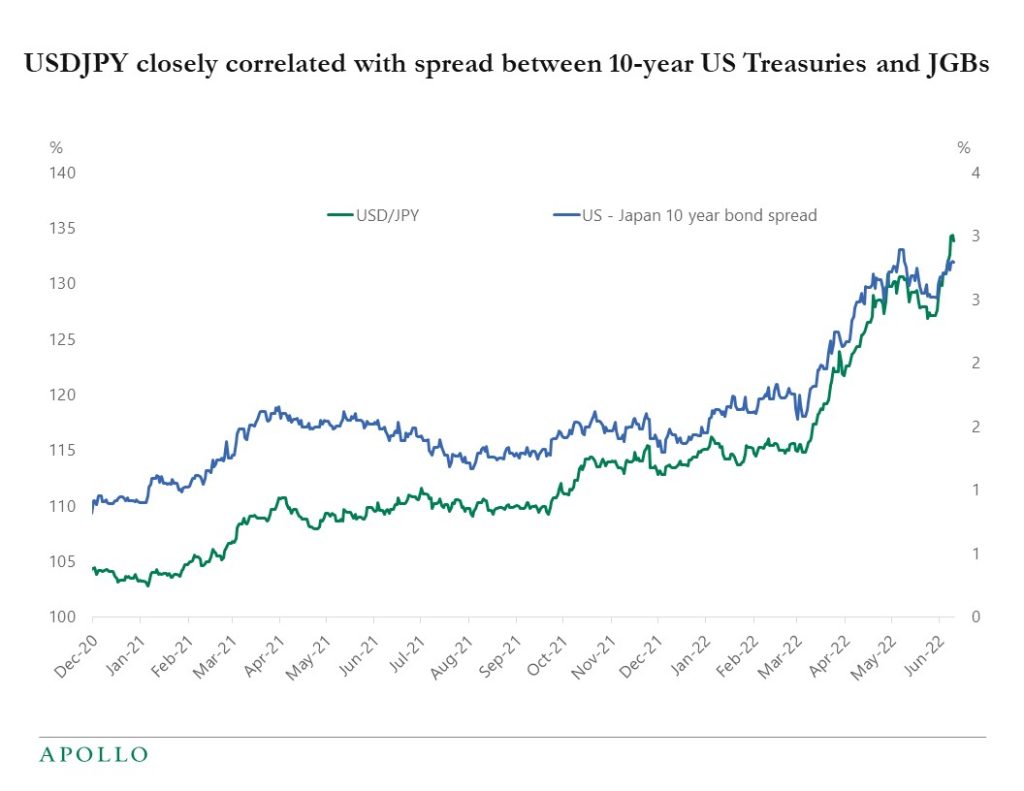

The biggest foreign holder of US Treasuries is Japan, but Japanese investors have in recent months been selling Treasuries. With the Fed raising rates, hedging costs have increased, making US Treasuries less attractive for foreign investors. This is likely to continue as long as the Bank of Japan does yield curve control. The bottom line is that with rising hedging costs, foreign investors have less appetite to buy US Treasuries, which adds to the upward pressure on US rates.

Source: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

Larry Summers: Comparing Past and Present Inflation

https://www.nber.org/papers/w30116Buy Now, Pay Later (BNPL)…On Your Credit Card

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4001909China’s Economic and Trade Ties with Russia

https://crsreports.congress.gov/product/pdf/IF/IF12120See important disclaimers at the bottom of the page.

-

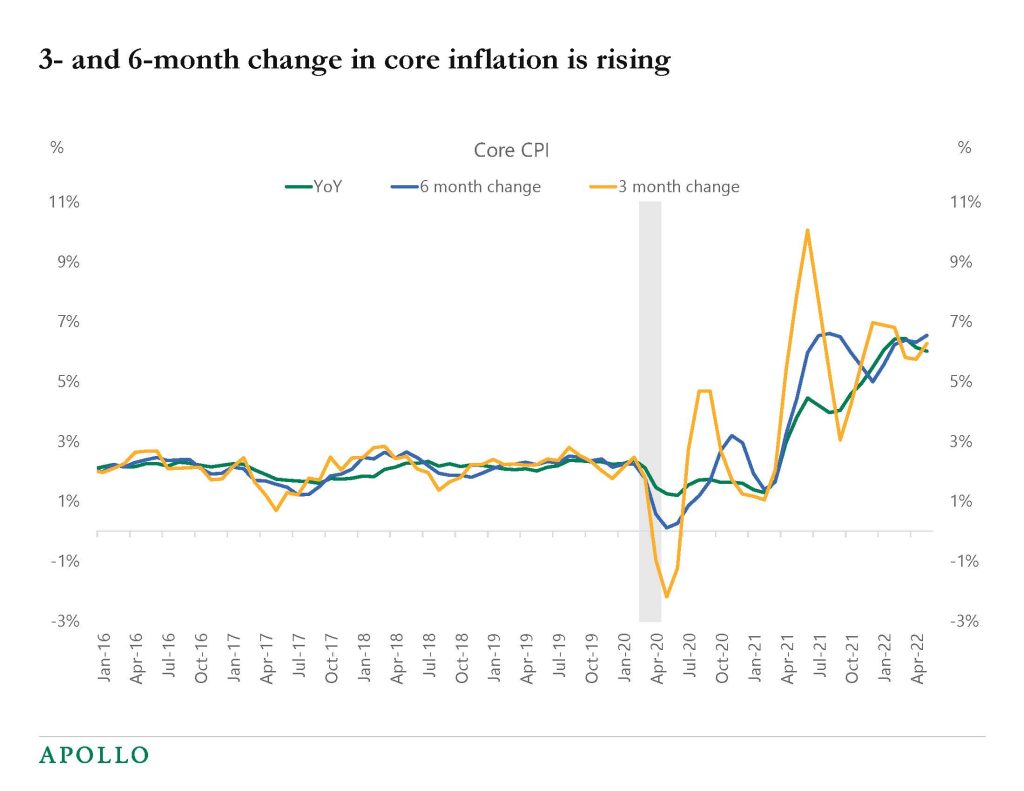

The most important economic data this week was inflation, and both the 3-month change and the 6-month change in core CPI moved higher, raising the risk that inflation will not come down as quickly as the Fed and the consensus expect. View the report here.

Source: BLS, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

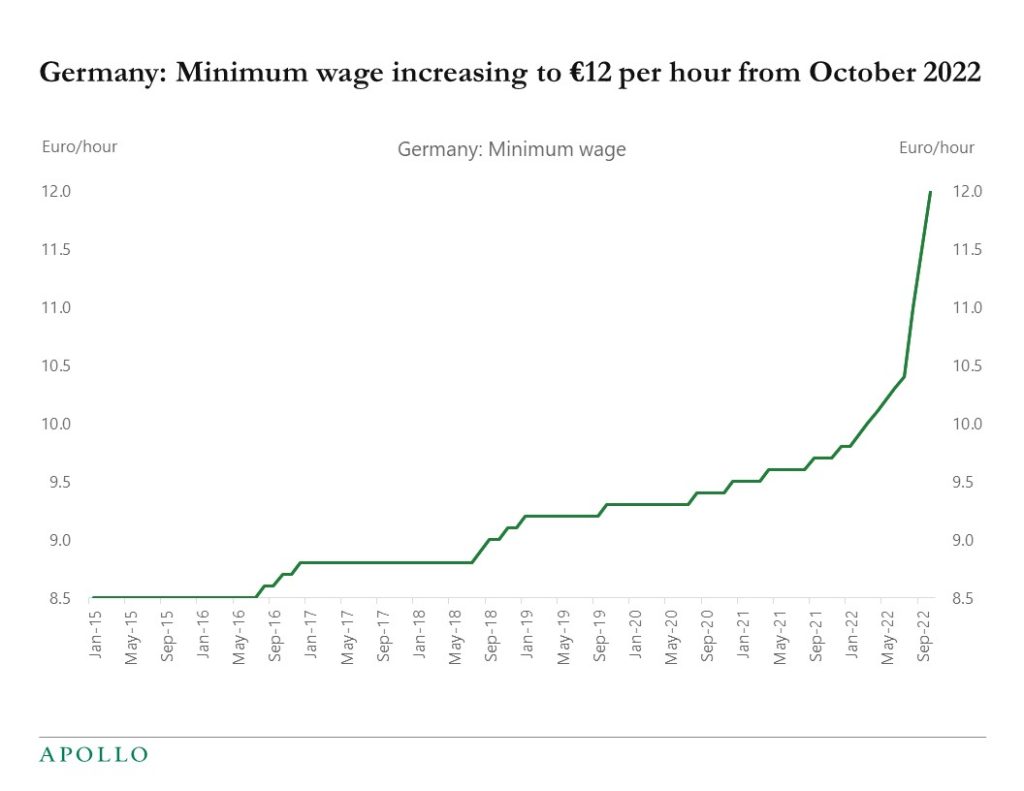

The minimum wage in Germany will increase in October to 12 euros per hour, see chart below, which will lift the income for about 6 million workers. Total employment in Germany is about 45 million.

Source: Federal Statistics Office, Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

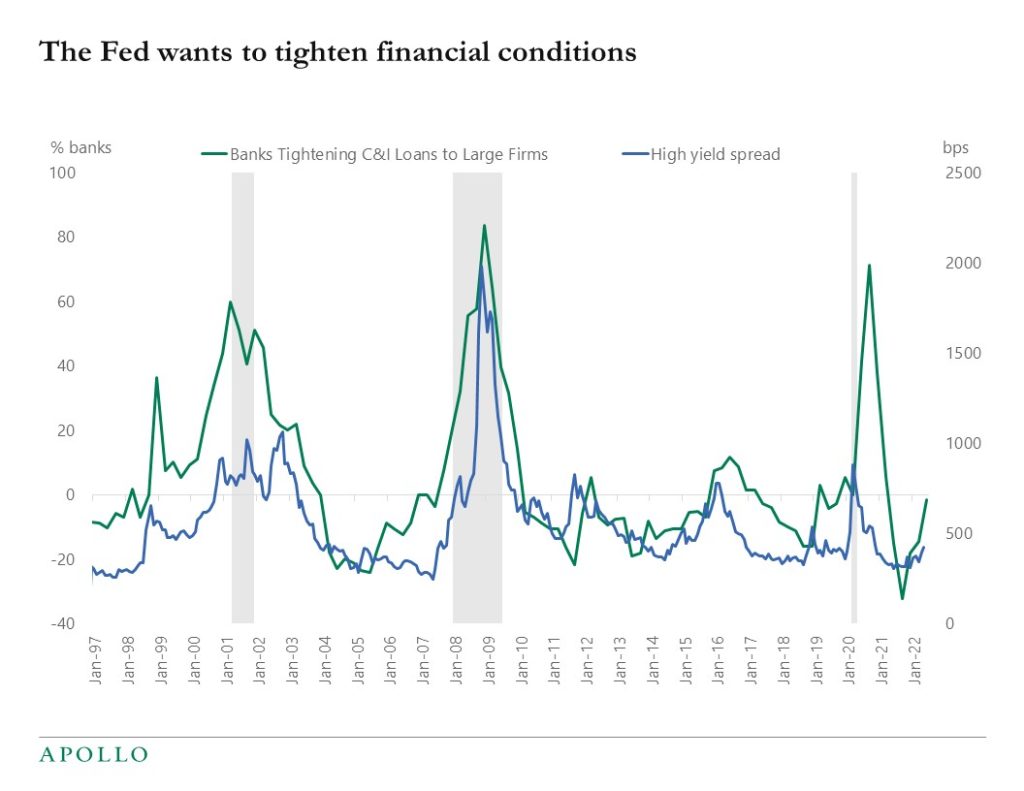

A crucial part of the Fed’s goal to tighten credit conditions is to push credit spreads wider. So far, HY spreads have not widened as much as the tightening in lending conditions in banks, see chart below.

Source: FRB, Haver Analytics, Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

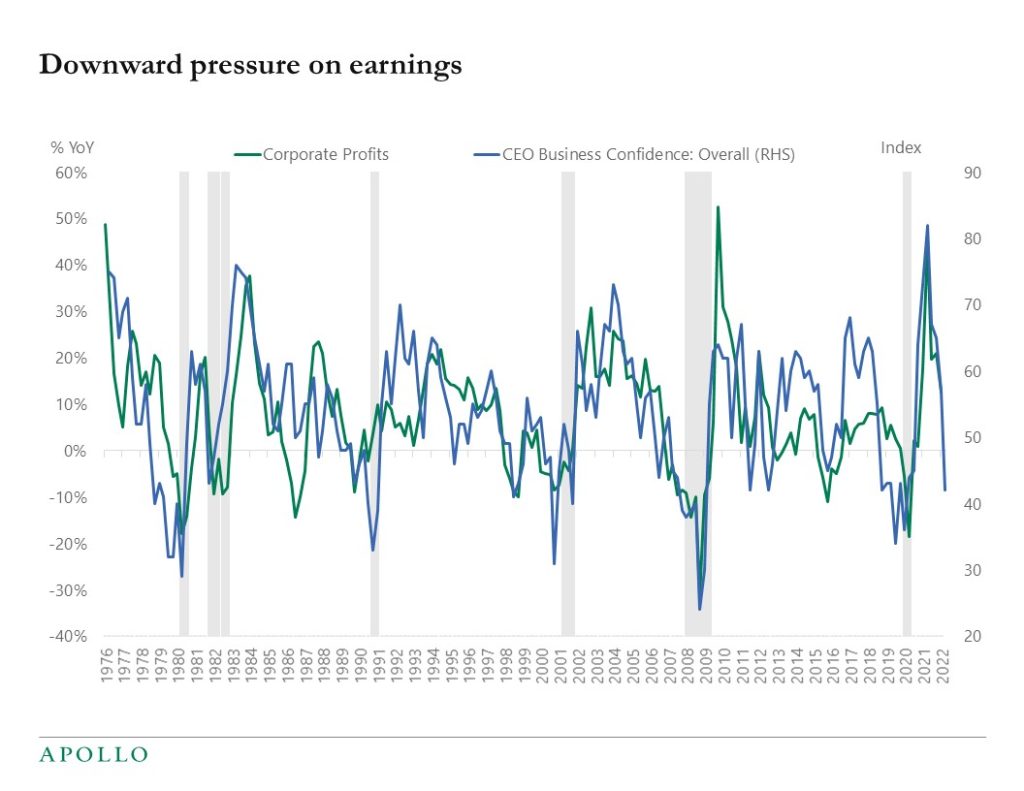

The Fed is cooling down the economy, and CEO confidence is plunging. That is why the E in the P/E ratio is going lower, see chart below.

Source: BEA, Conference Board, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

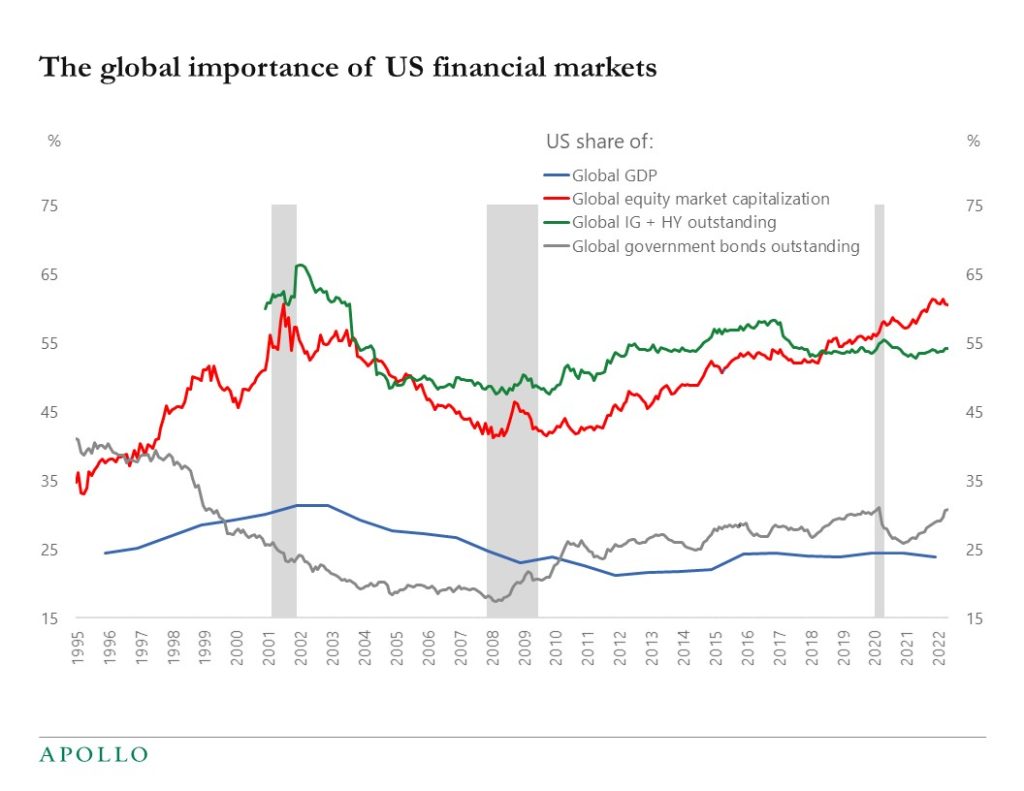

US is 25% of global GDP but 61% of global stock markets and 54% of global credit markets, see chart below.

Source: Bloomberg, Haver, Apollo Chief Economist. Note: Bloomberg tickers: MXUS Index, MXWD Index , LUATTRUU Index, BTSYTRUU Index, LF98TRUU Index, LG30TRUU index, LUACTRUU Index, I09805US index. See important disclaimers at the bottom of the page.

-

We have updated our US consumer outlook chart book, see the attached PDF.

See important disclaimers at the bottom of the page.

-

Fed: How Did It Happen?: The Great Inflation of the 1970s and Lessons for Today

https://www.federalreserve.gov/econres/feds/files/2022037pap.pdfThe Rest of the World’s Dollar-Weighted Return on U.S. Treasurys

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3928006IMF: Sovereign Eurobond Liquidity and Yields

https://www.imf.org/-/media/Files/Publications/WP/2022/English/wpiea2022098-print-pdf.ashxFed: Neighborhood Types and Demographics

https://files.stlouisfed.org/files/htdocs/publications/economic-synopses/2022/06/01/neighborhood-types-and-demographics.pdfSee important disclaimers at the bottom of the page.

-

We have updated our attached daily and weekly indicators for the US economy, and the daily data for airline travel, consumer mobility, and restaurant bookings are still not showing signs of a slowdown.

The weekly data for hotel occupancy rates is also solid, and weekly jobless claims continue to decline, suggesting that the labor market is still strong. Weekly data for cinema visits is also strong, and so is the weekly data for bank lending and the weekly data for credit and debit card usage.

There are some early signs of weakness in the housing market, with the weekly data for listings starting to trend higher in recent weeks. Traffic of prospective home buyers is also starting to come down.

At the anecdotal level, there are more sound bites about layoffs in tech and startups, but these anecdotes are not yet visible in the macro data.

The bottom line is that the economy is still strong, and the Fed needs to tighten financial conditions further to slow growth and inflation.

See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.