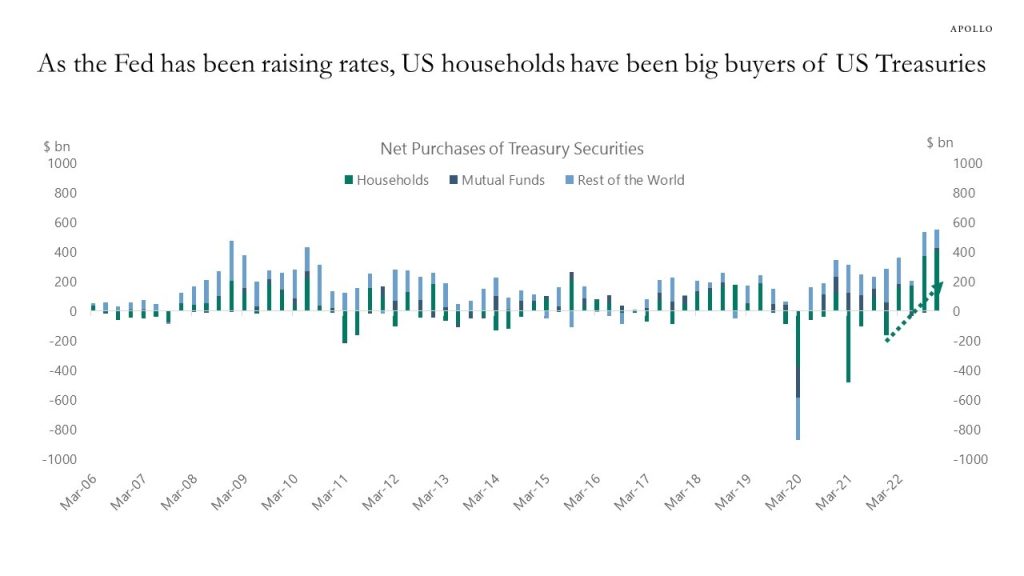

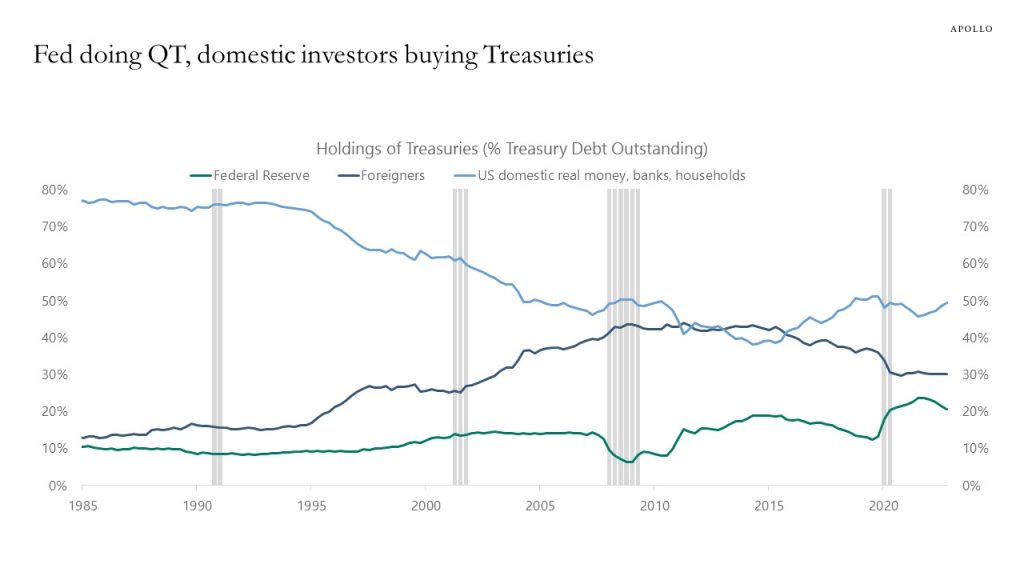

As the Fed has been raising rates, US households have been big buyers of US Treasuries, see the first two charts below.

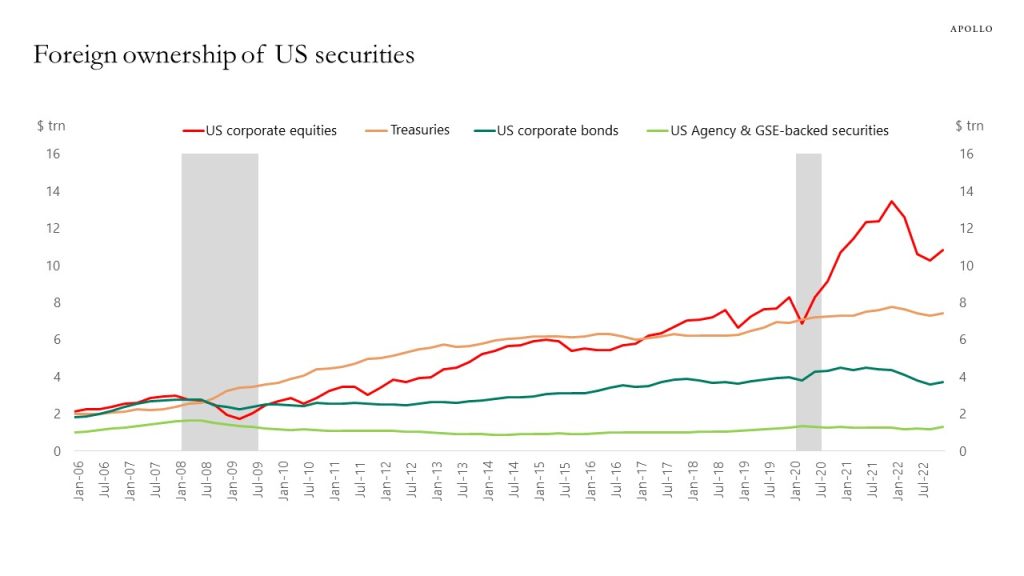

The appetite for Treasuries from foreigners has been more limited because of higher hedging costs. Foreigners have instead increased their holdings of equities by $3 trillion during the pandemic, see the third chart.

With a 5% budget deficit combined with QT and the Treasury’s need to replenish cash in the Treasury General Account, markets will soon begin to focus on who will be buyers of US government debt.