Want it delivered daily to your inbox?

-

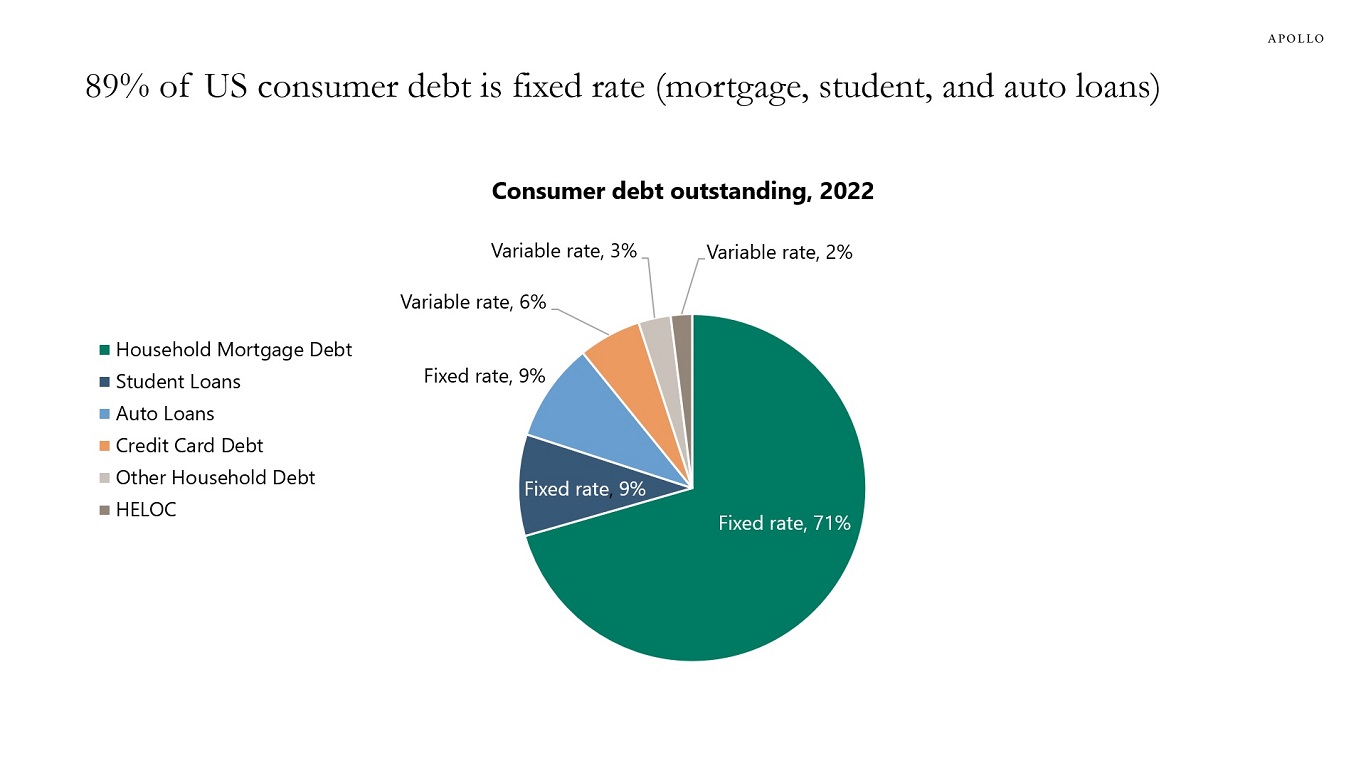

Eighty-nine percent of US household debt is fixed rate (mortgage, student, and auto loans) and 11% is floating rate (credit cards, HELOC, and other types of debt).

As a result, the transmission mechanism of monetary policy has been weak. Combined with significant excess savings during the pandemic, Fed hikes have had a limited impact on the consumer.

Source: FRBNY Consumer Credit Panel, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

Key themes for credit investors:

1) New issuance rallying sharply as demand remains strong from pension, annuity sales, and retail. Credit spreads continue to tighten and are trading near the tight end of the two-year range. Beta compression remains a key theme across credit, with the exception of CCCs.

2) Credit spreads are tight, but all-in yields are attractive with a Fed cutting outlook. Strong demand from yield buyers should limit the extent of any spread widening, barring a material worsening in the macro backdrop.

3) Uncertainty about the ongoing soft landing will keep volatility elevated. Hard landing or reacceleration in inflation are still possible scenarios.

4) Mid-beta credit such as BBB debt offers the attractive combination of wide spreads and stronger sponsorship from yield-driven demand. Financial conditions have eased recently but funding costs remain high, which combined with slowing growth could impact firms with weak balance sheets. Elevated cash balances on investment grade corporate balance sheets could drive a pick-up in M&A activity.

See important disclaimers at the bottom of the page.

-

See important disclaimers at the bottom of the page.

-

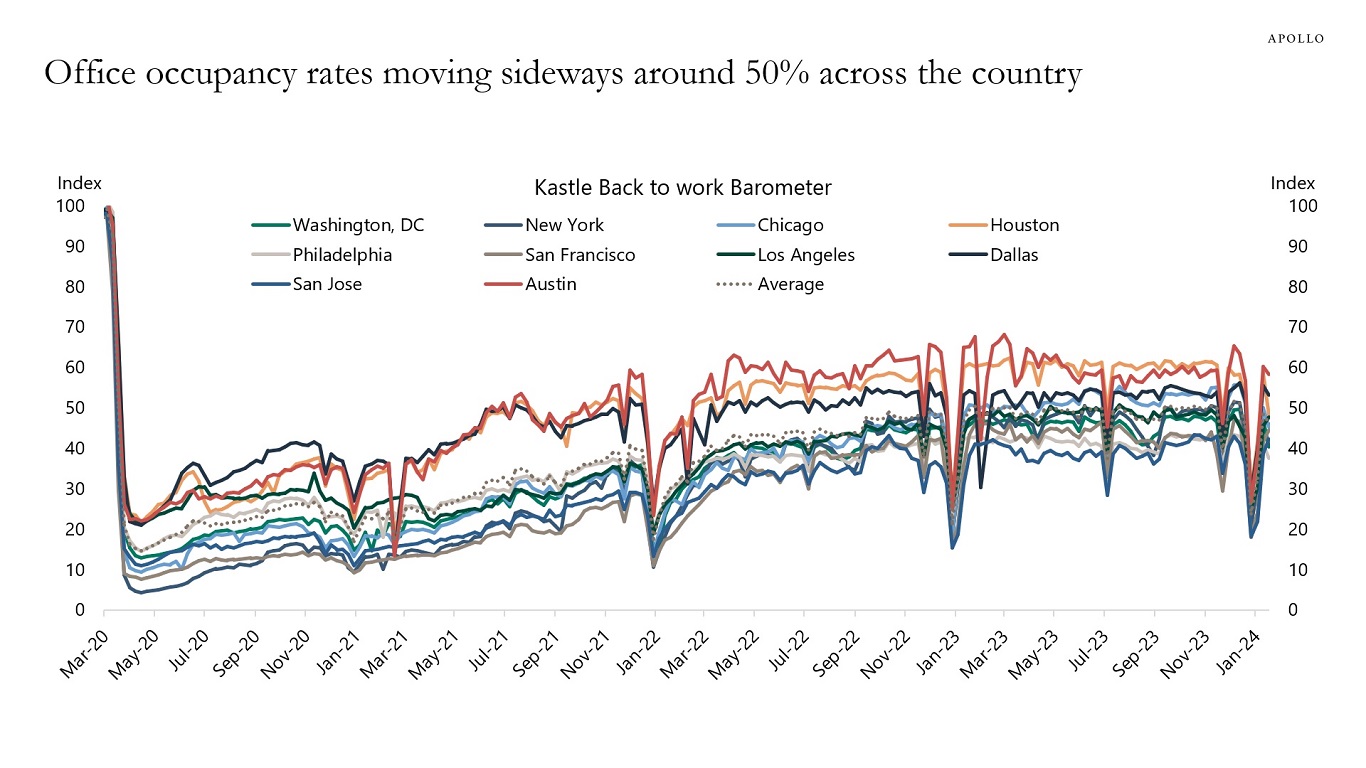

The data for office use across the country shows that hybrid work is here to stay, see chart below.

The numbers show the average for a week where Wednesdays can be as high as 60%, and Mondays and Fridays as low as 30%.

The data is weekly and comes from 300,000 workers in 10 different cities, and in New York, the data covers 200 buildings and 70,000 workers.

The latest data shows that the lowest office occupancy rate is for Philadelphia at 37%, and the highest is Austin at 58%.

For more discussion of this topic, see also here.

Source: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

The price of transporting a container is rising and air freight rates are increasing, but the ongoing supply chain problems are not broad based like the way they were during the pandemic, see our chart book available here.

See important disclaimers at the bottom of the page.

-

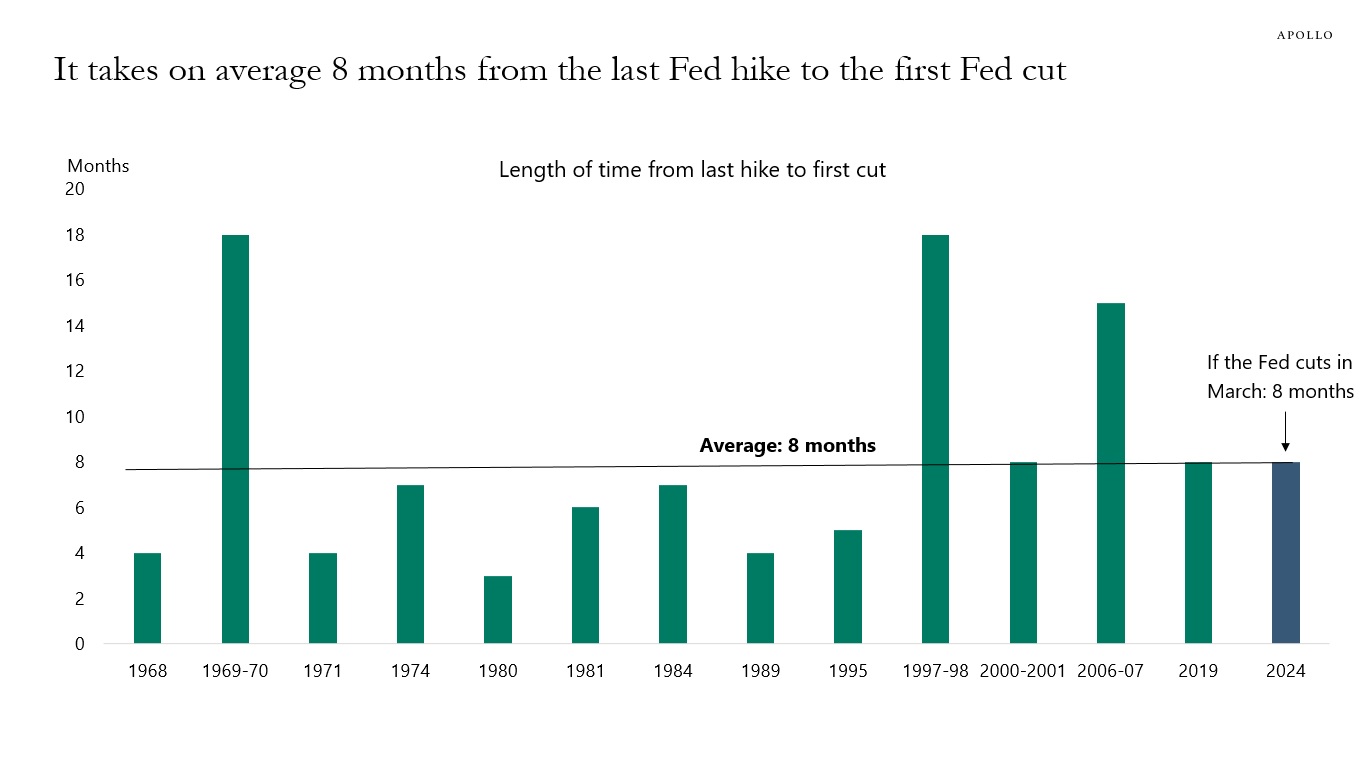

If the Fed cuts in March, it will be eight months after the last Fed hike, which is exactly the average of all previous Fed hike cycles, see chart below.

Source: FRB, Haver Analytics, Apollo Chief Economist. Note: Discount rate used before 1988. See important disclaimers at the bottom of the page.

-

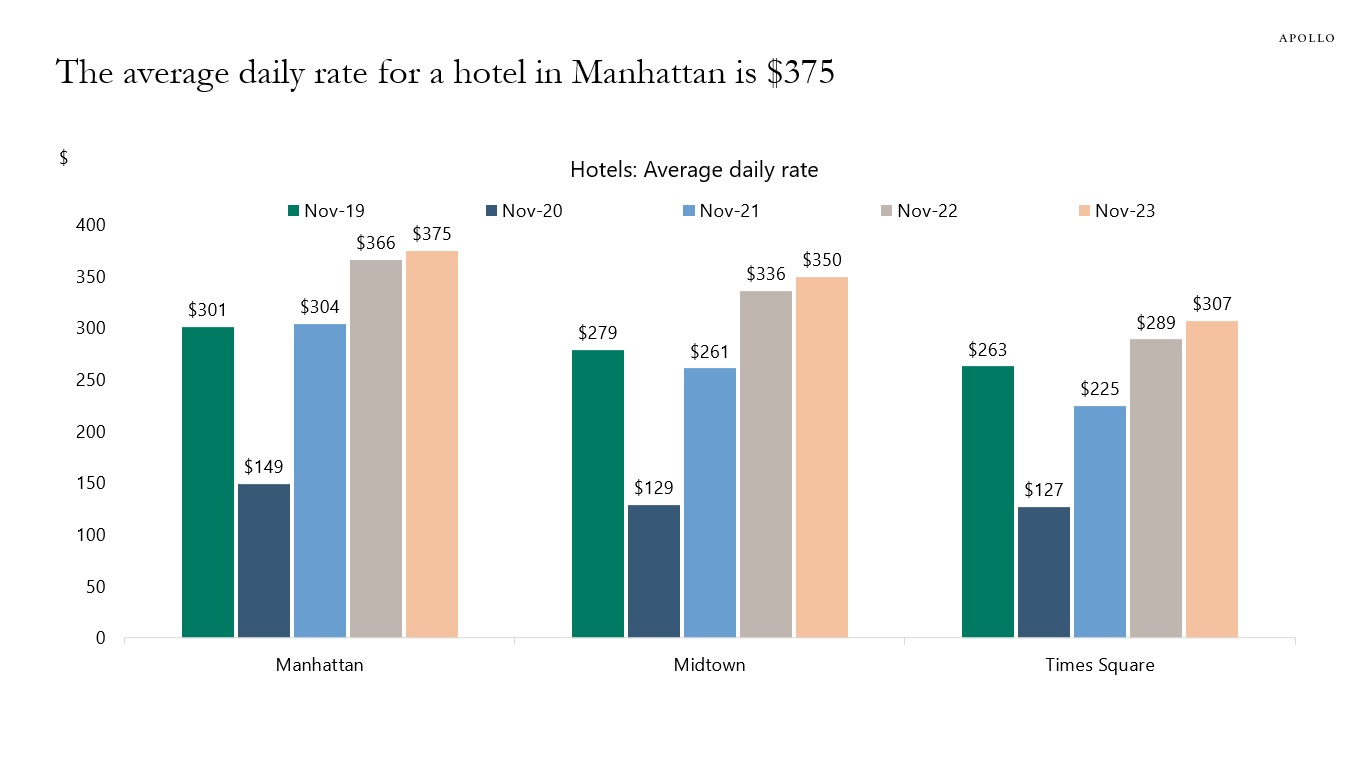

The average price of a hotel room in Manhattan is now $375 per night, see chart below.

Source: Timessquarenyc.org, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

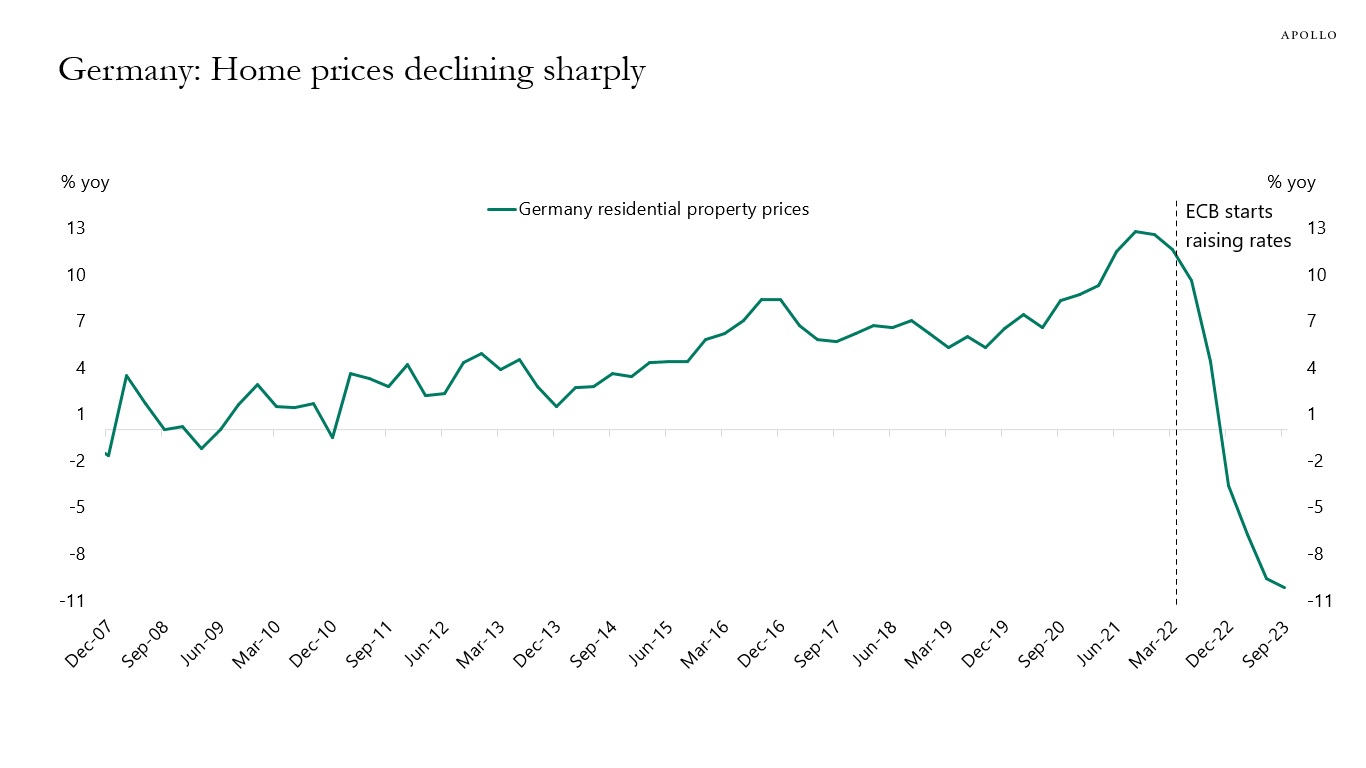

Home prices are in freefall in Germany, driven by higher rates, high construction costs, and massive amounts of red tape in the housing sector, see chart below.

This downtrend is in sharp contrast to the US, where home prices are rising.

With more persistent inflation in Europe, and the ECB therefore cutting after the Fed, the downward pressure on home prices is likely to continue.

Source: Eurostat, Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

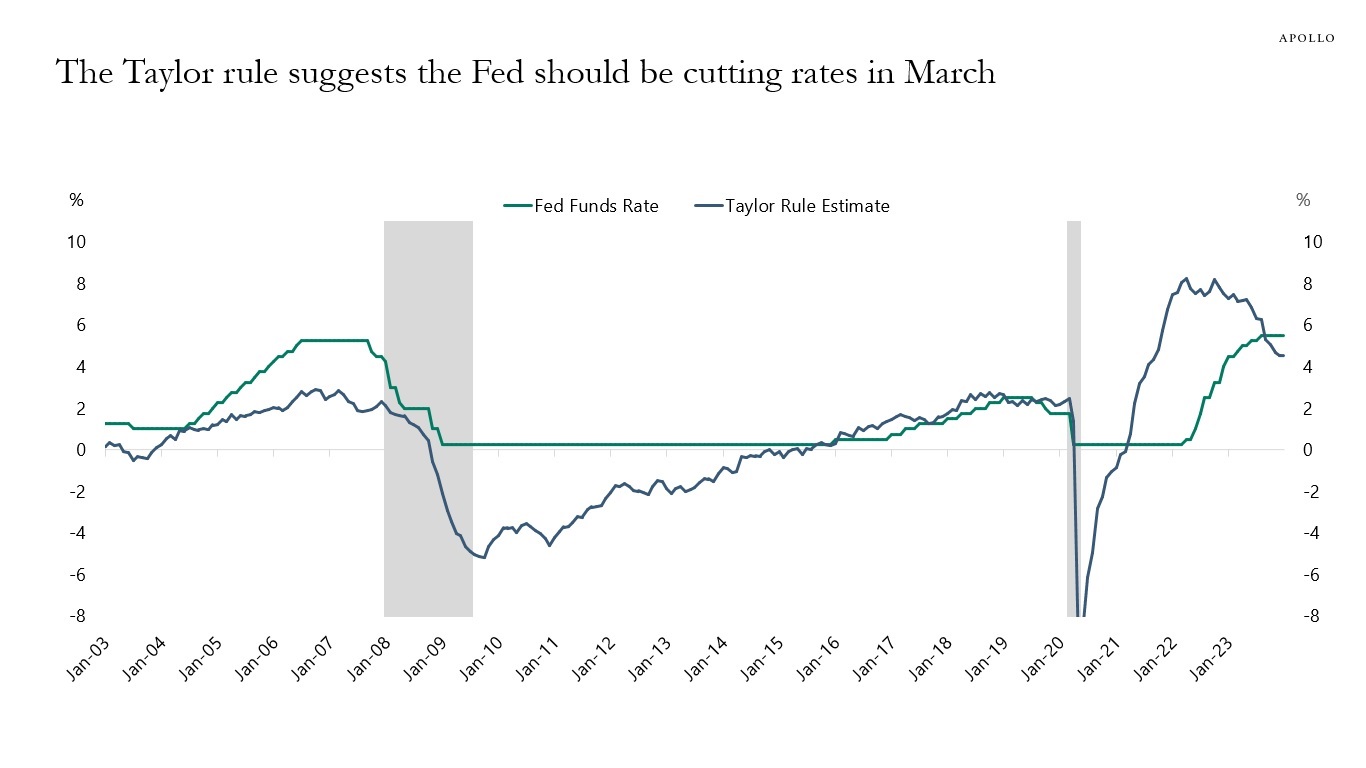

The main argument for the Fed cutting rates in March is that the Fed’s workhorse model says that because of the sharp decline in inflation over the past six months, the Fed funds rate today should not be 5.5% but 4.5%, see chart below. Specifically, the Fed has used the Taylor rule framework for decades to understand what the Fed funds rate should be, and inserting the current level of inflation and unemployment into the Taylor rule shows that the Fed funds rate today should be 4.5%, see chart below and Daily Spark here.

Source: Bloomberg, Apollo Chief Economist. Note: Neutral real rate = 0.5, inflation target rate = 2, and NAIRU = 4. See important disclaimers at the bottom of the page.

-

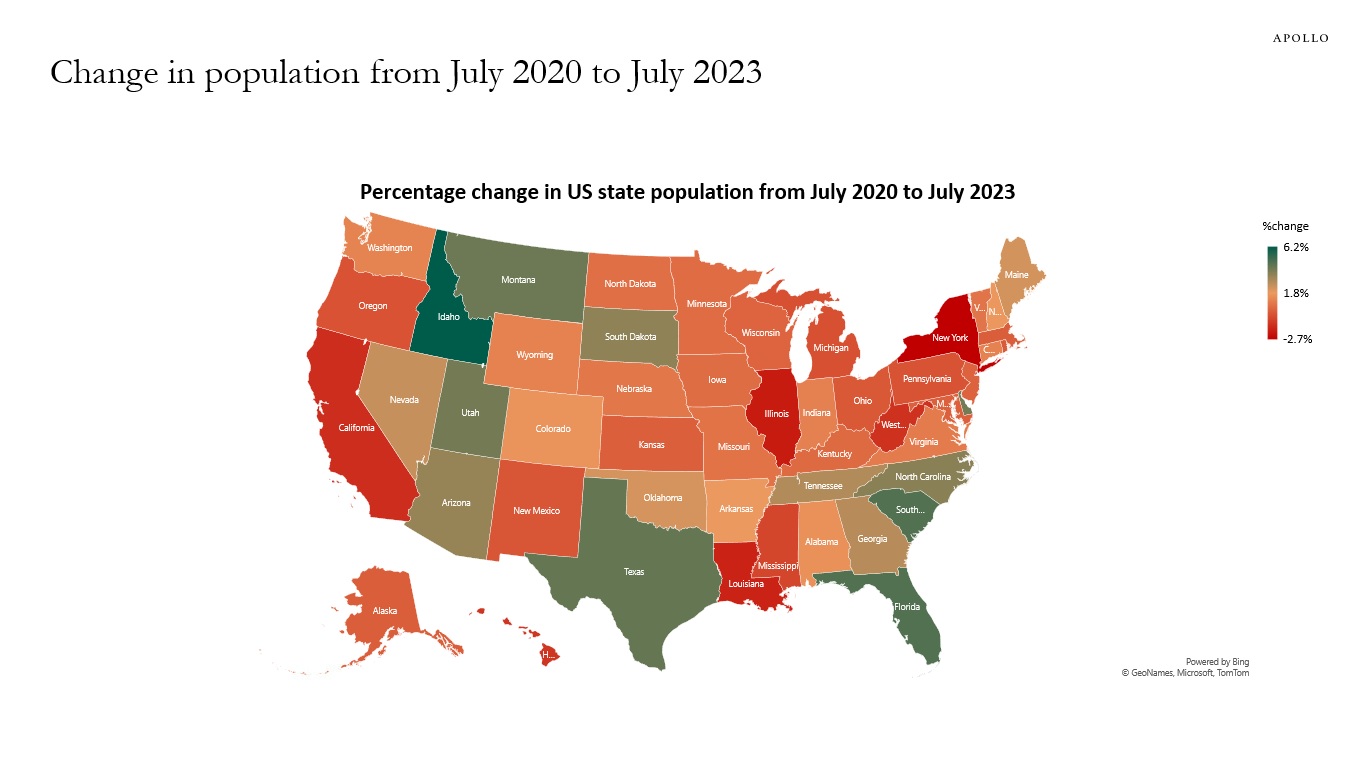

Since the middle of the pandemic, the population has been declining in New York and California, and growing in Florida and Texas, see map below.

Source: Census Bureau, Apollo Chief Economist See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.