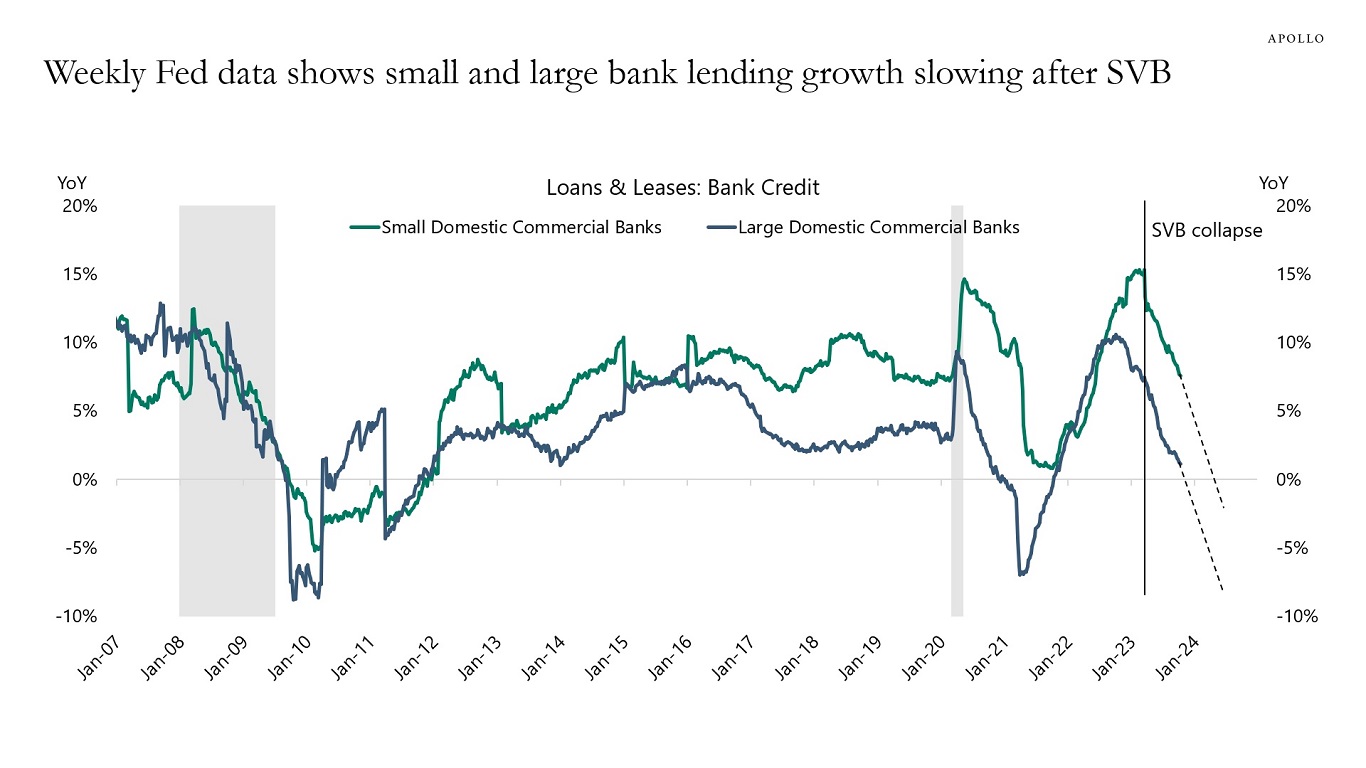

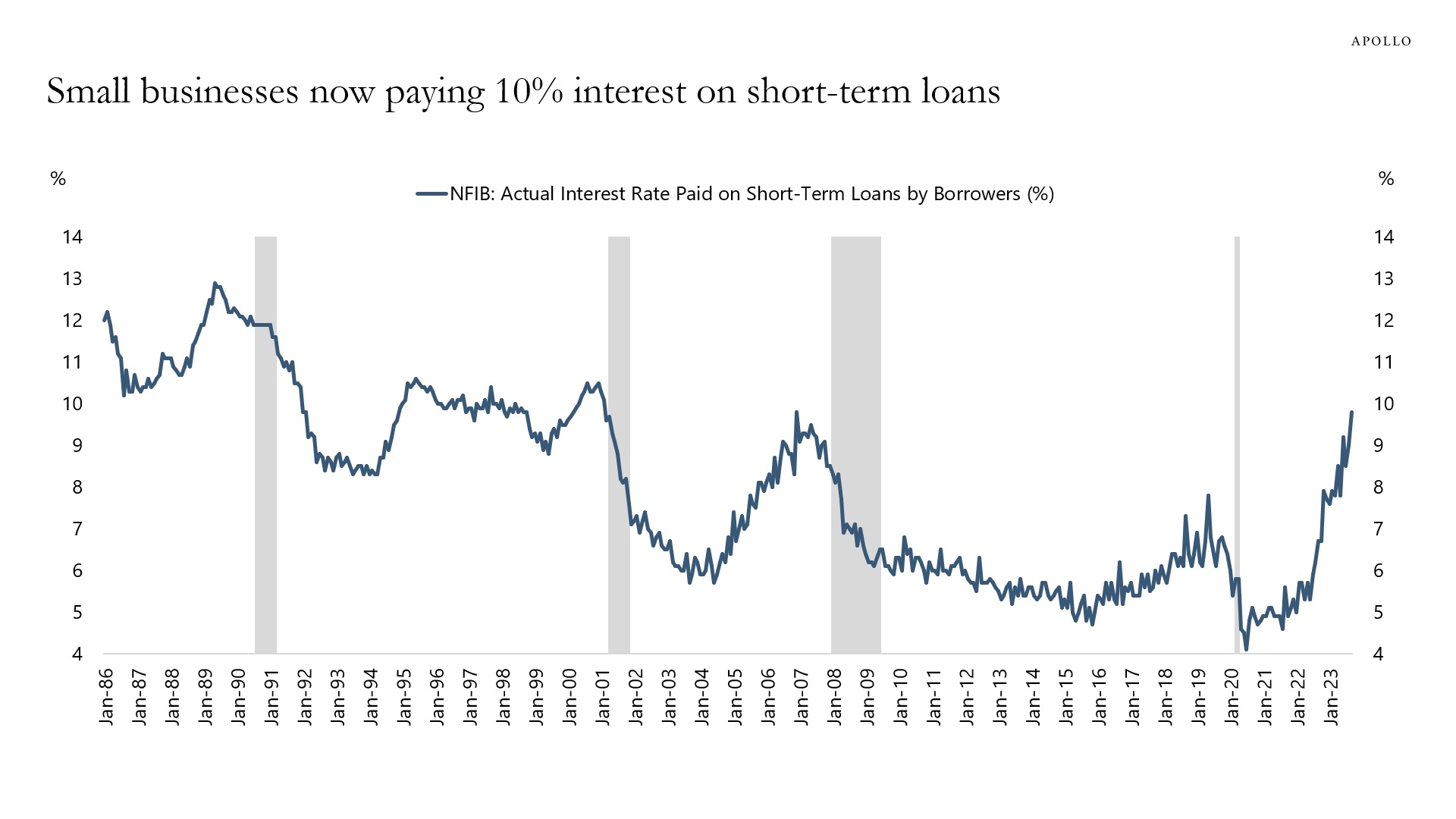

Our updated regional banking sector outlook is available here, and the weekly data shows a continued decline in loan growth in small and large banks, see the first chart.

The slowdown in loan growth is driven by Fed hikes and tighter lending standards following the SVB collapse.

With the Fed on hold until the middle of next year, these trends are likely to continue, and loan growth will soon turn negative.