Want it delivered daily to your inbox?

-

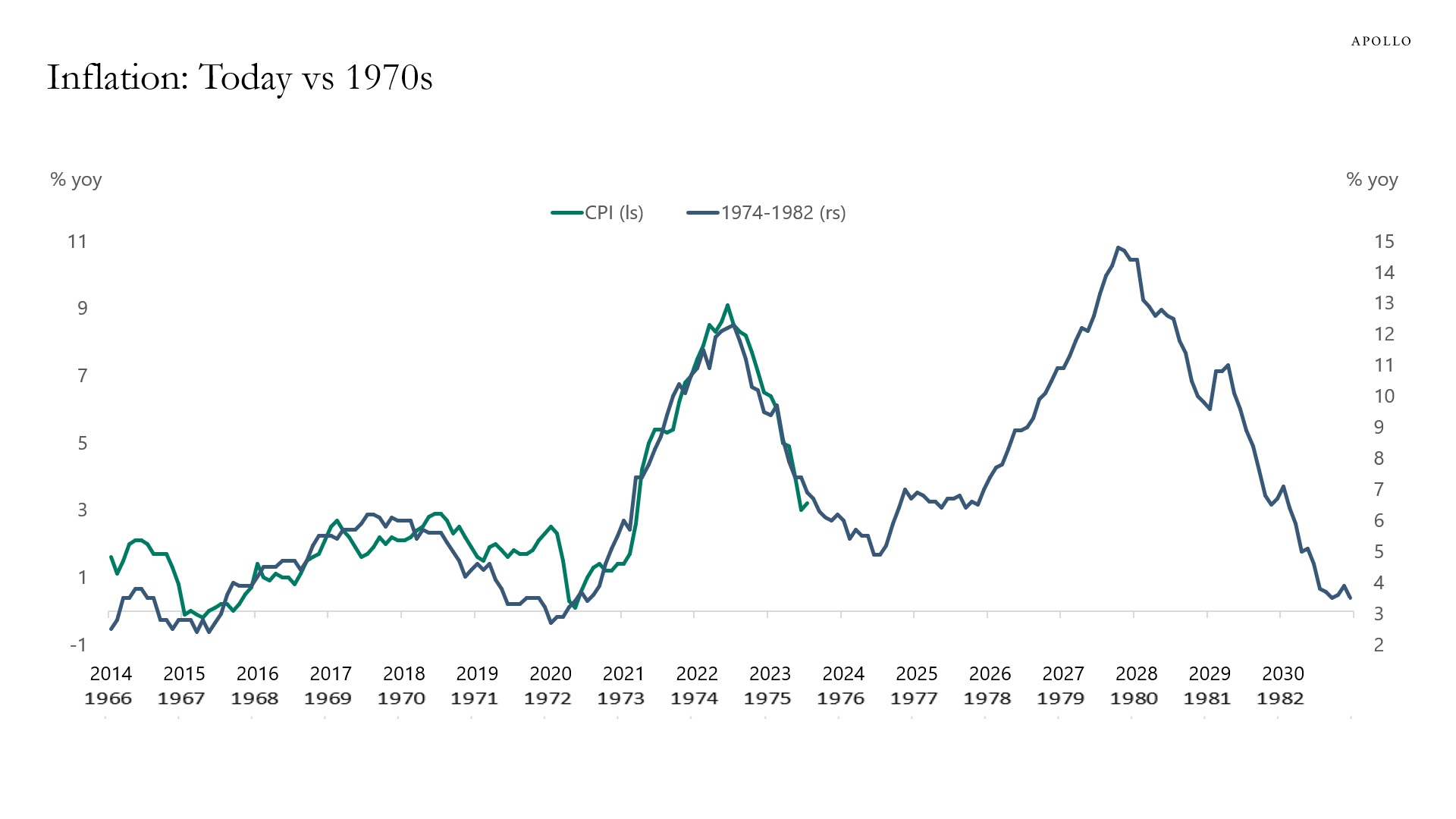

There are two lessons from the 1970s for the Fed today, see chart below.

First, if the Fed turns dovish too quickly, then inflation and inflation expectations will not settle at 2%.

Second, if the economy re-accelerates, the Fed will have to raise rates a lot more.

The implication for markets is that the Fed will be keeping the cost of capital higher for longer than the market is currently pricing to ensure that the FOMC doesn’t repeat the mistakes made in the 1970s.

Source: BLS, Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

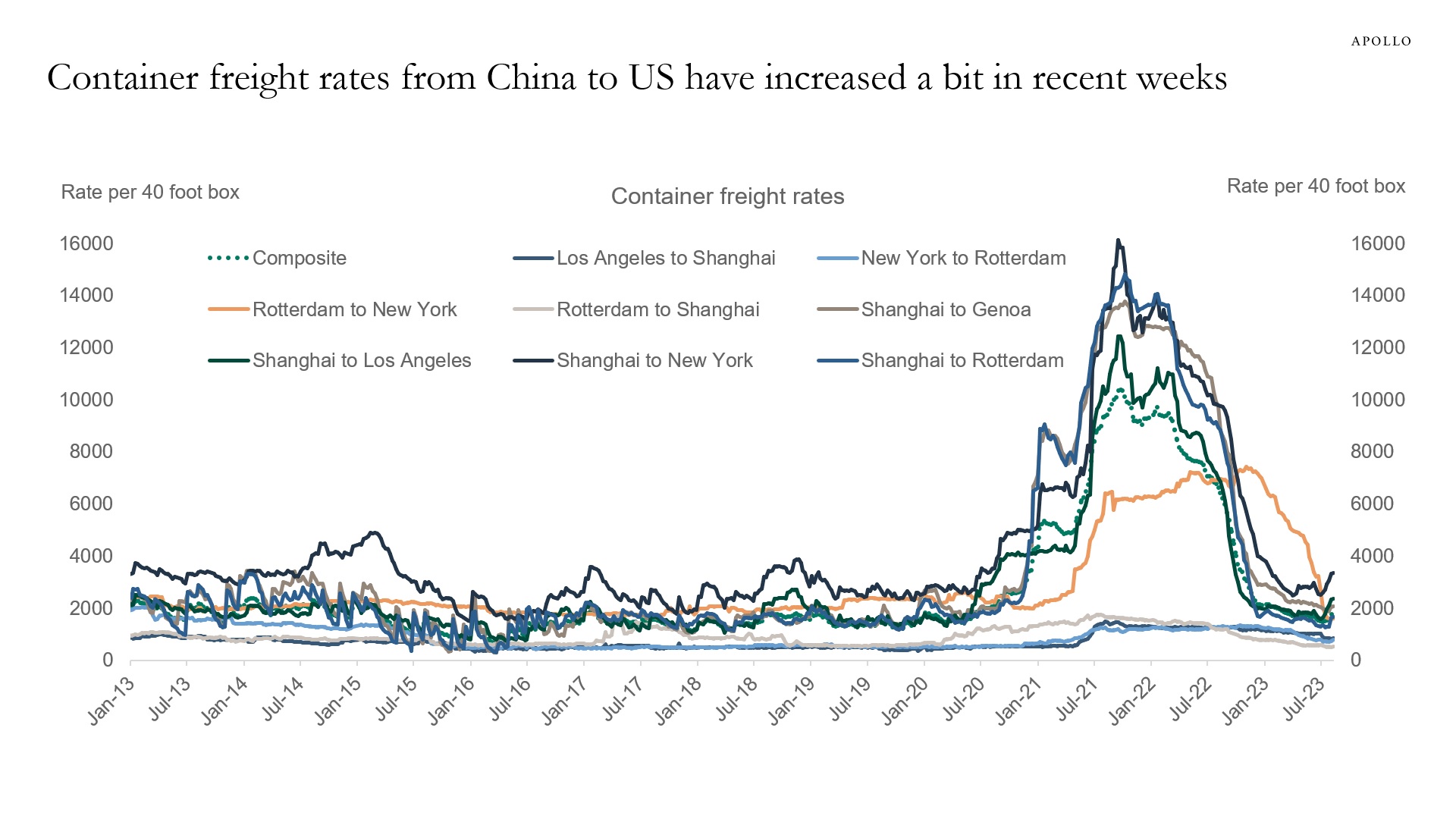

Supply chains are back to normal, but we are monitoring the rise in recent weeks in the price of transporting a container from China to the US. See chart below and this updated presentation.

Source: WCI, Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

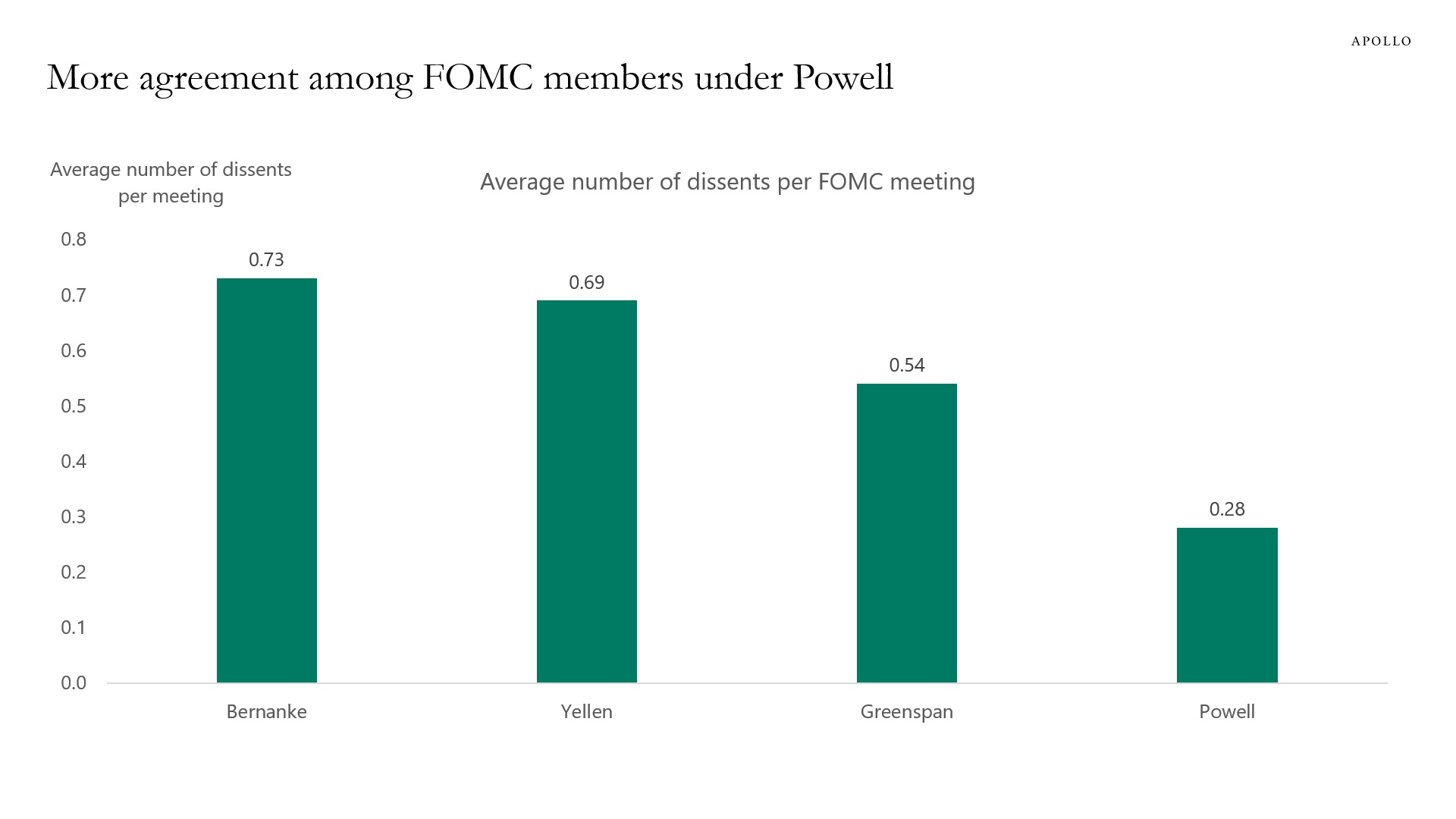

The average number of dissents per FOMC meeting has been lower under Powell, see chart below.

Source: FRB, Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

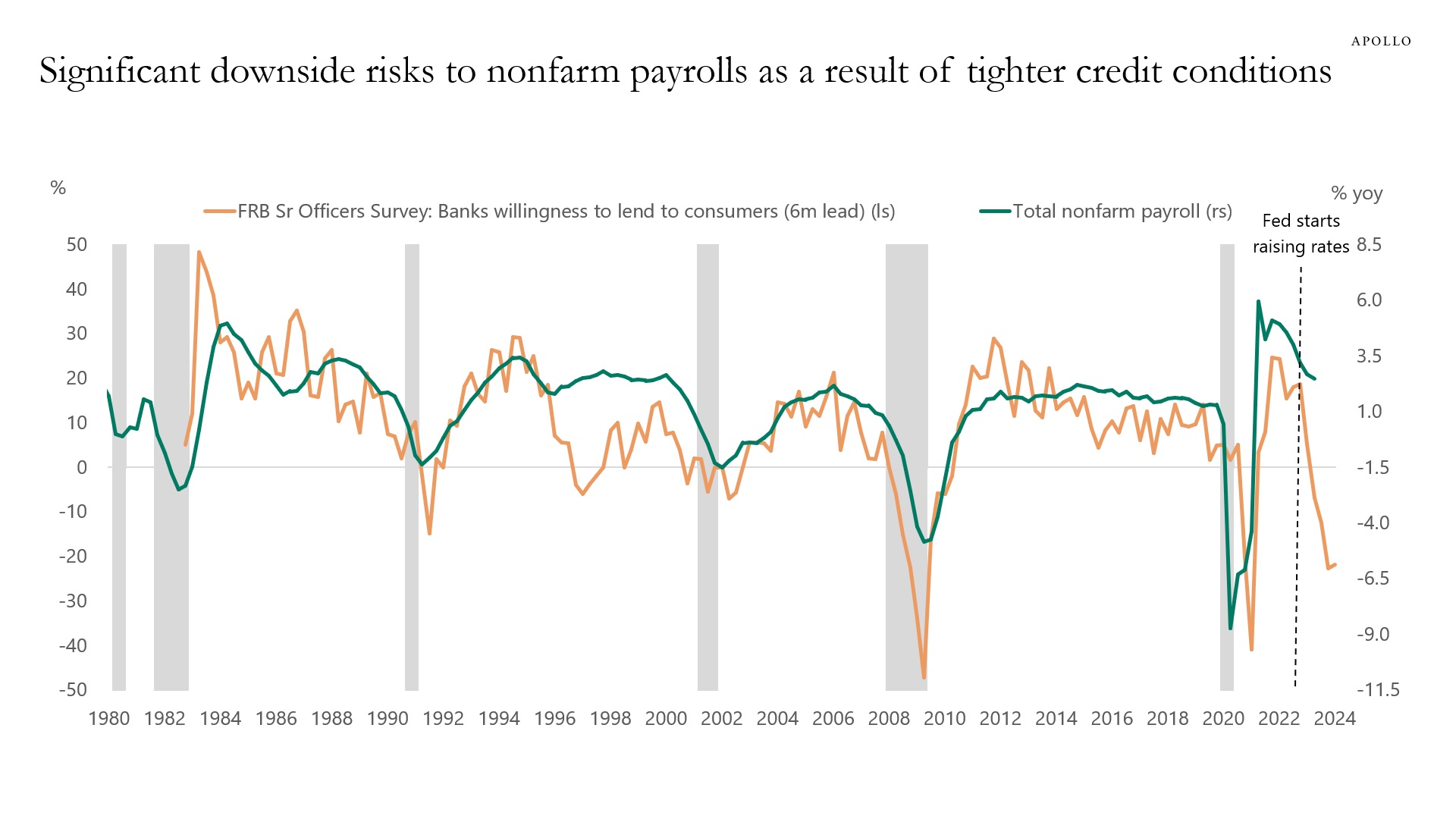

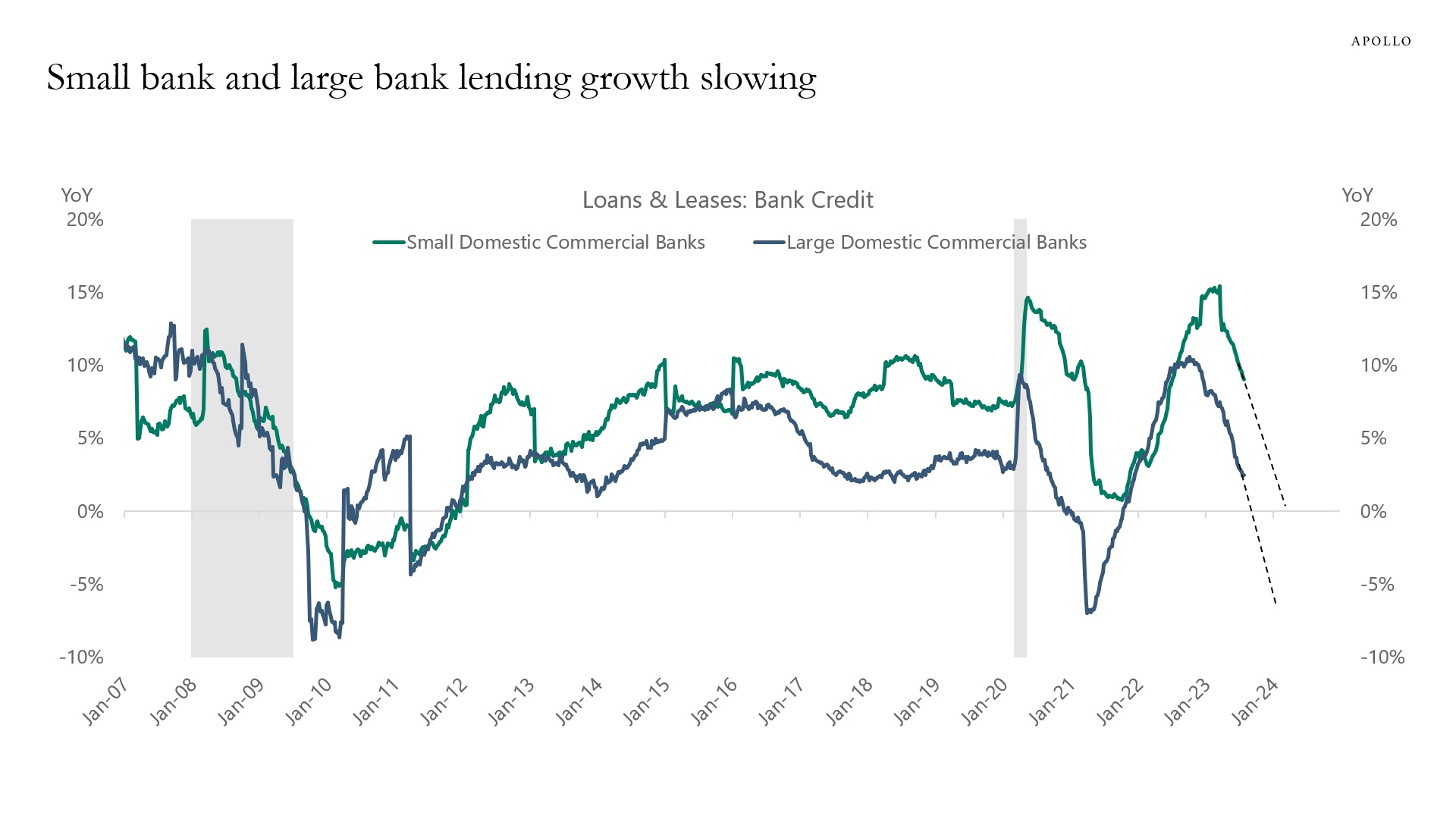

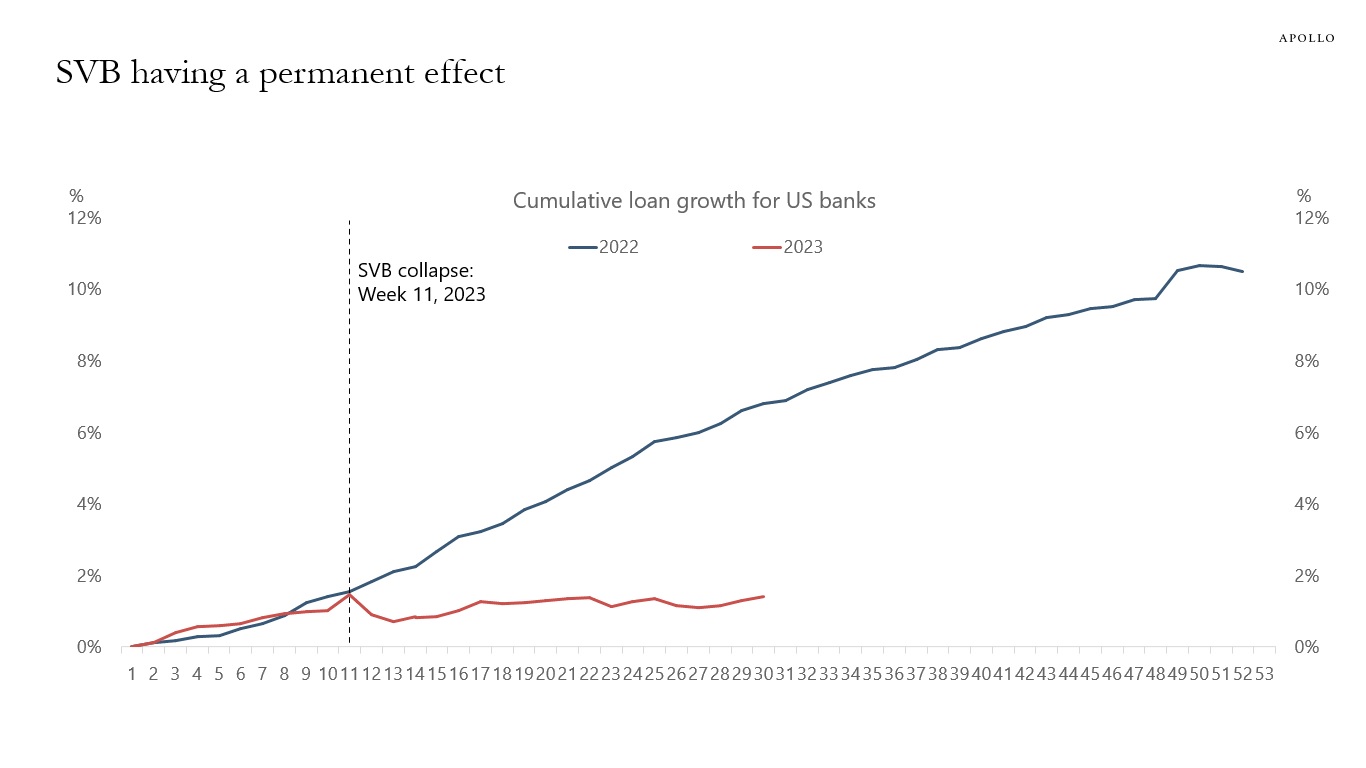

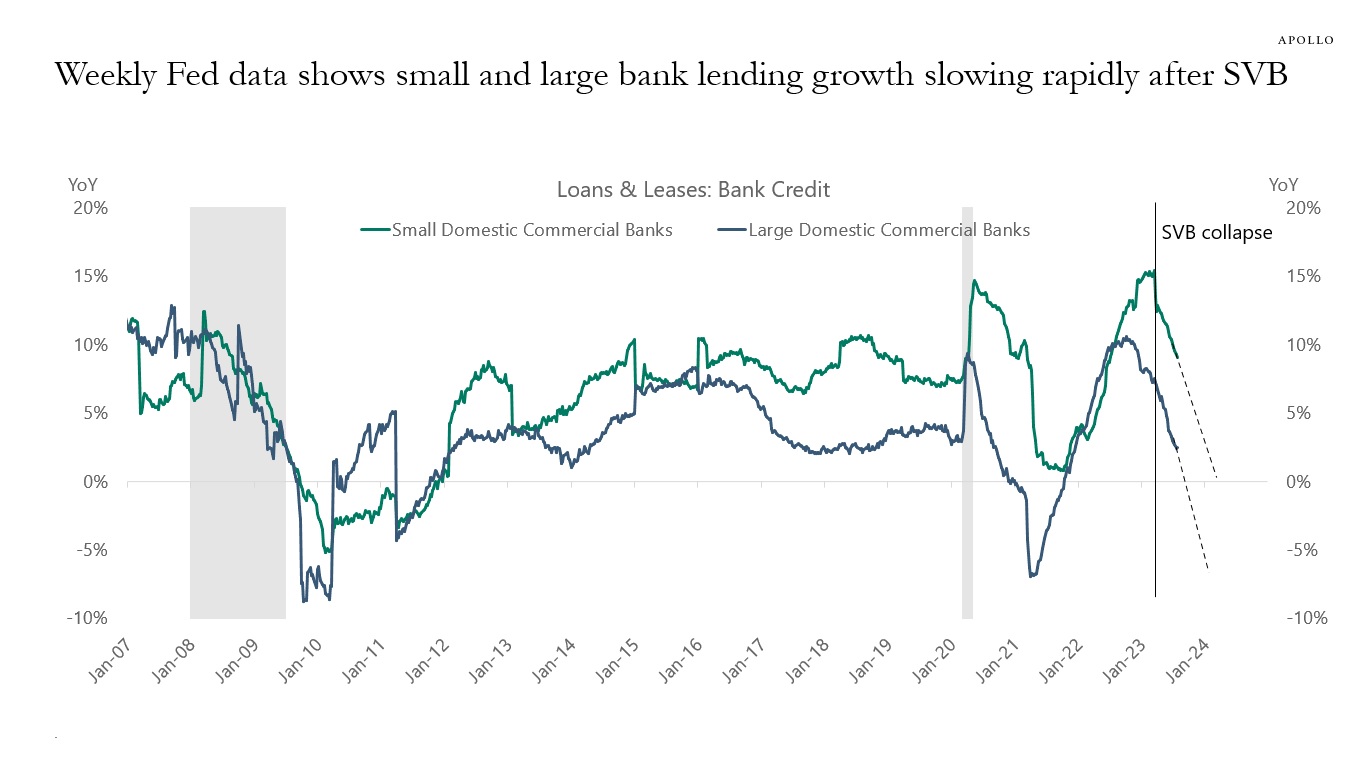

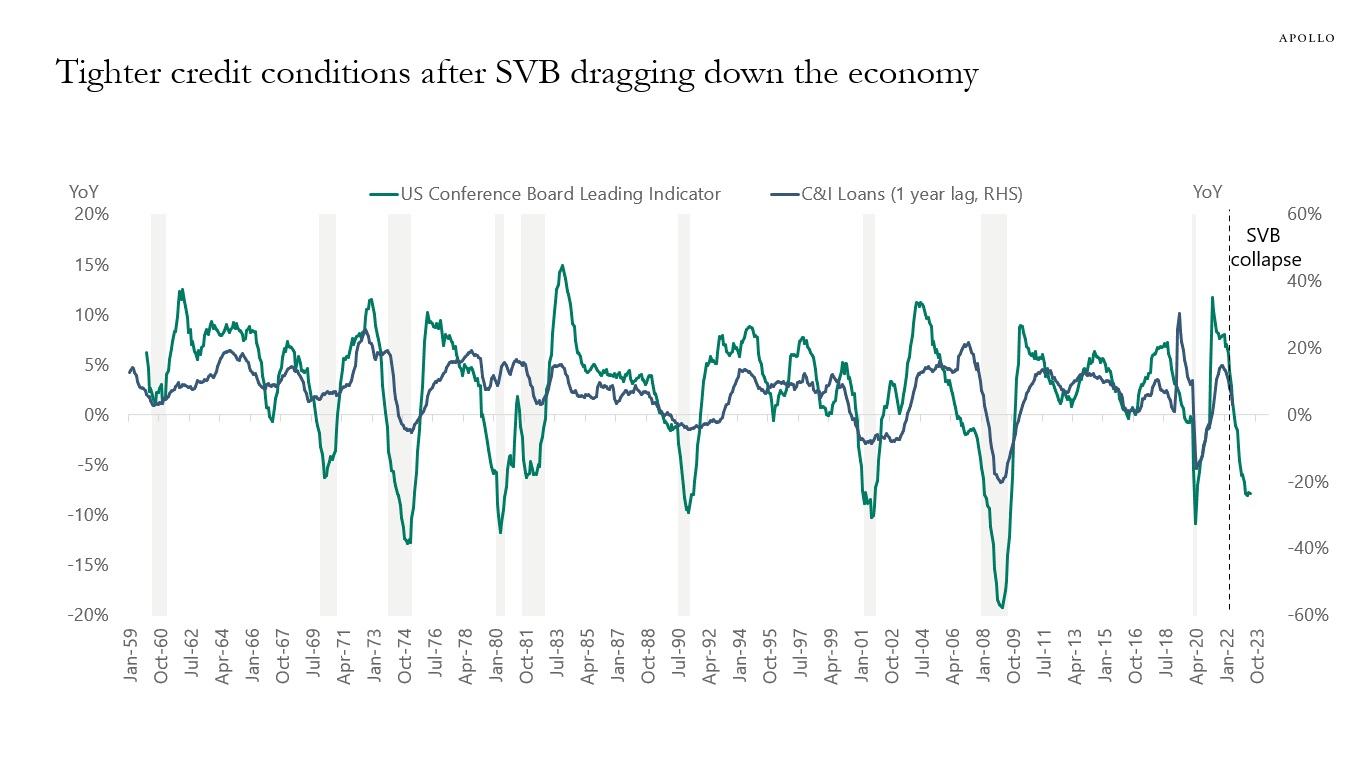

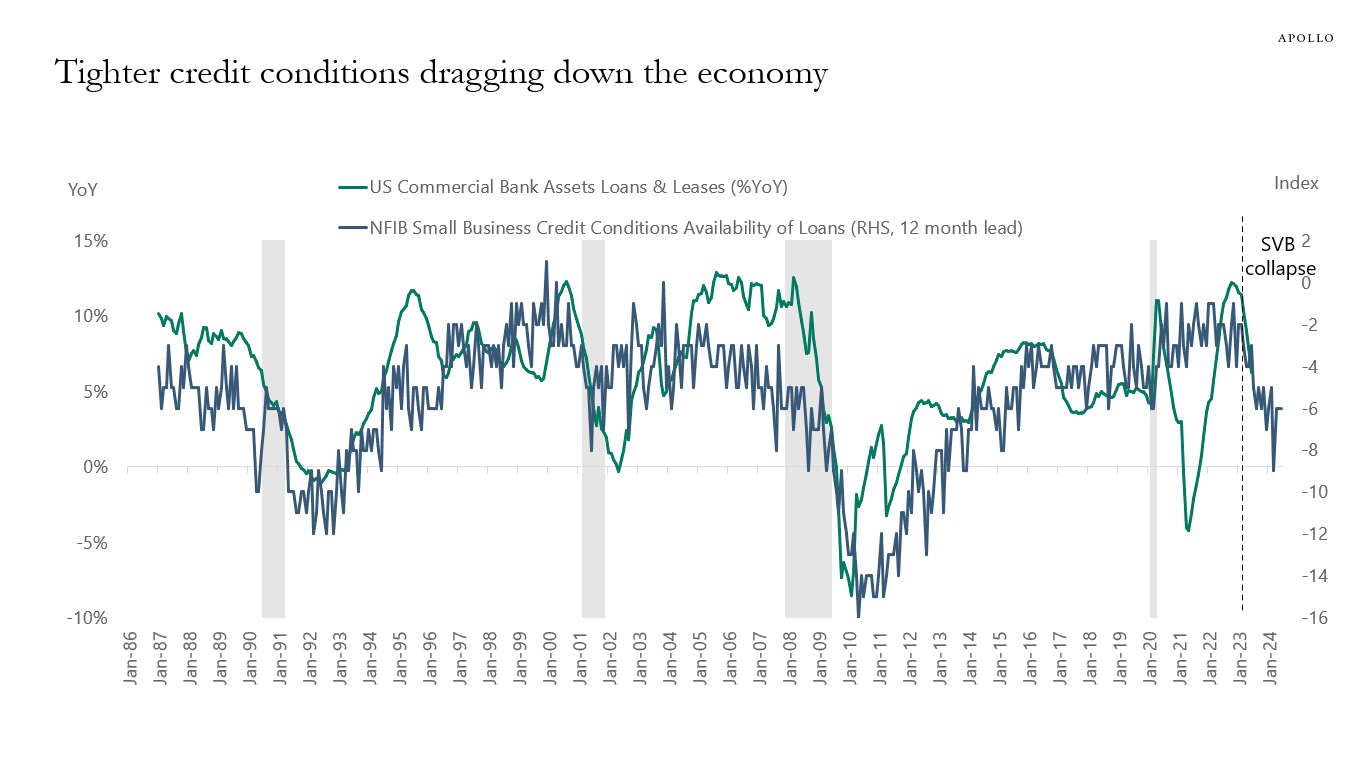

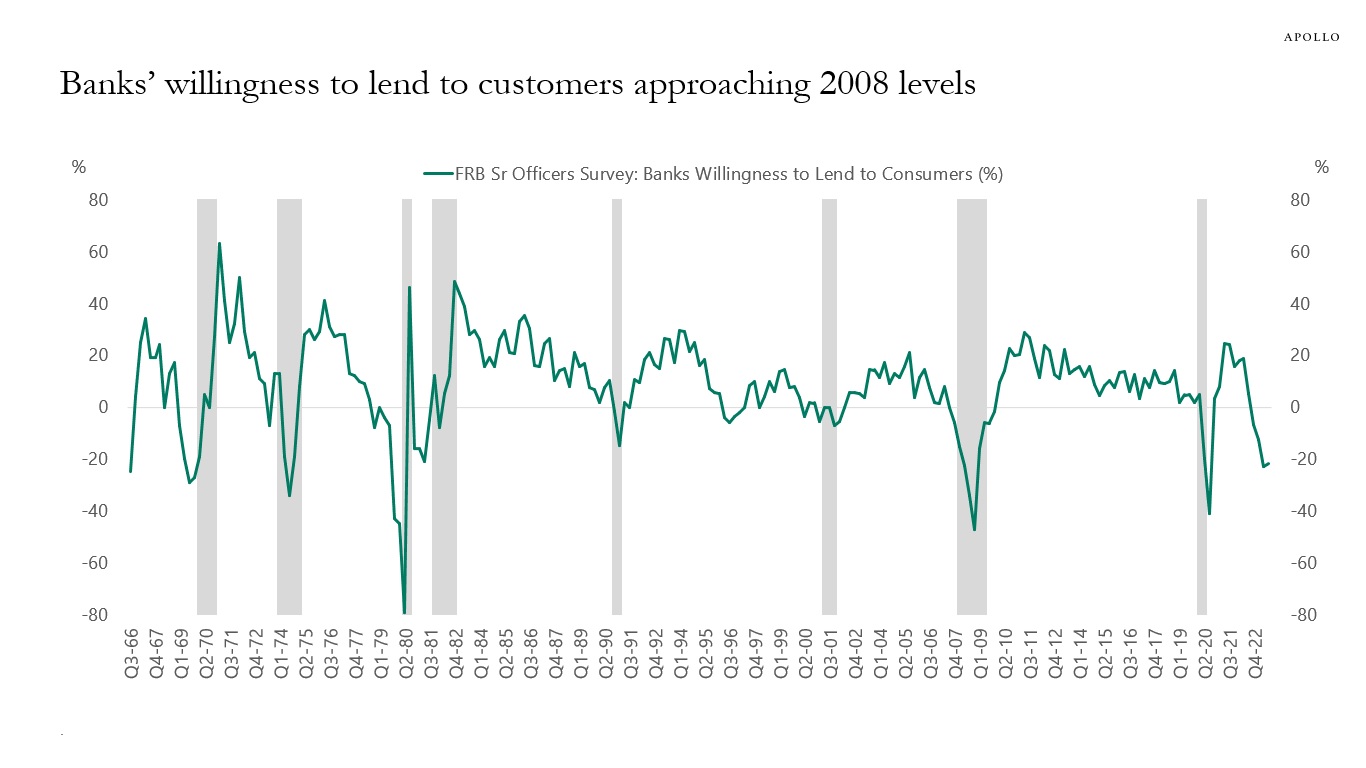

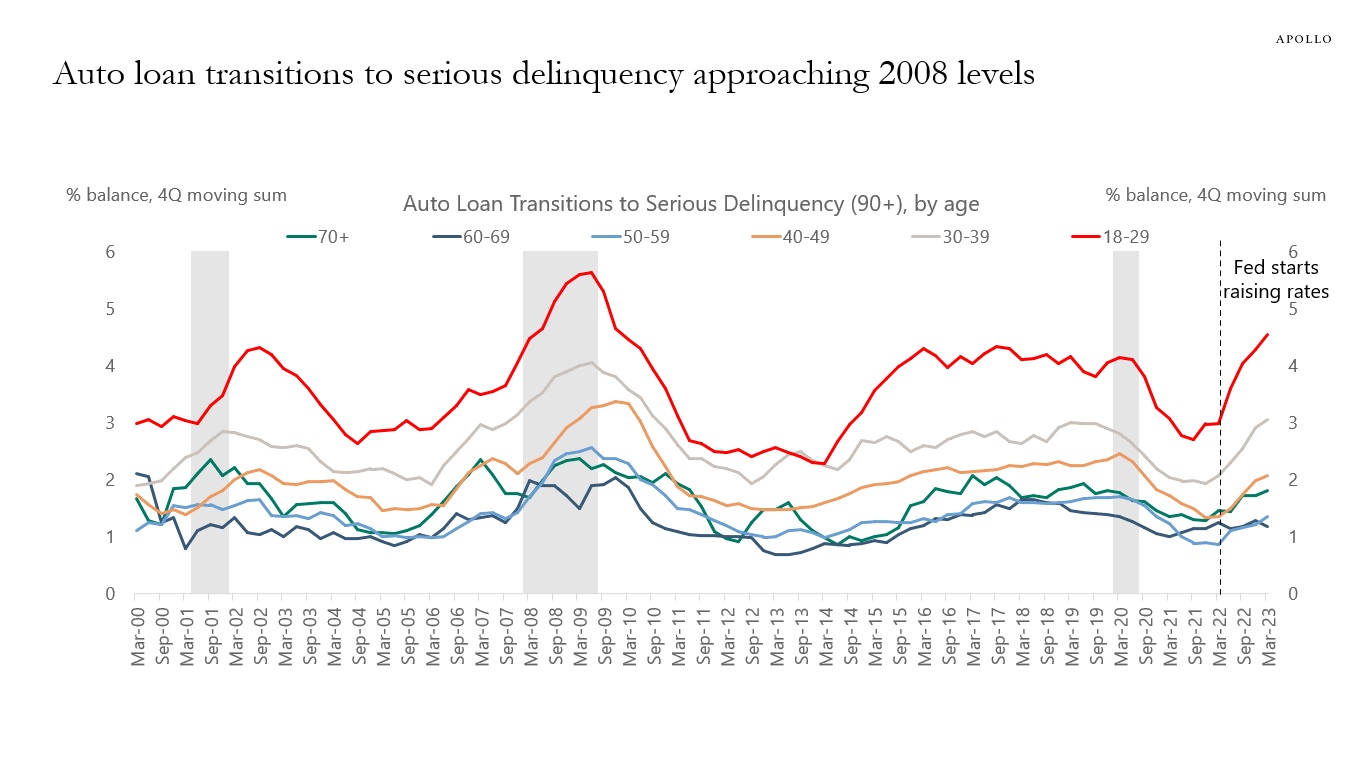

Since the Fed started raising rates, banks are much less willing to lend to consumers, and every day there are more and more consumers who have difficulties getting a credit card, auto loan, or mortgage, see the first chart below.

That is how monetary policy works. By raising interest rates, fewer households can borrow, which is why credit growth is slowing rapidly, see the second chart.

With consumers facing higher interest rates and tighter lending standards, the downside risk to nonfarm payrolls over the coming six months is significant, see again the first chart below.

Source: FRB, BLS, Haver Analytics, Apollo Chief Economist

Source: Federal Reserve Board, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

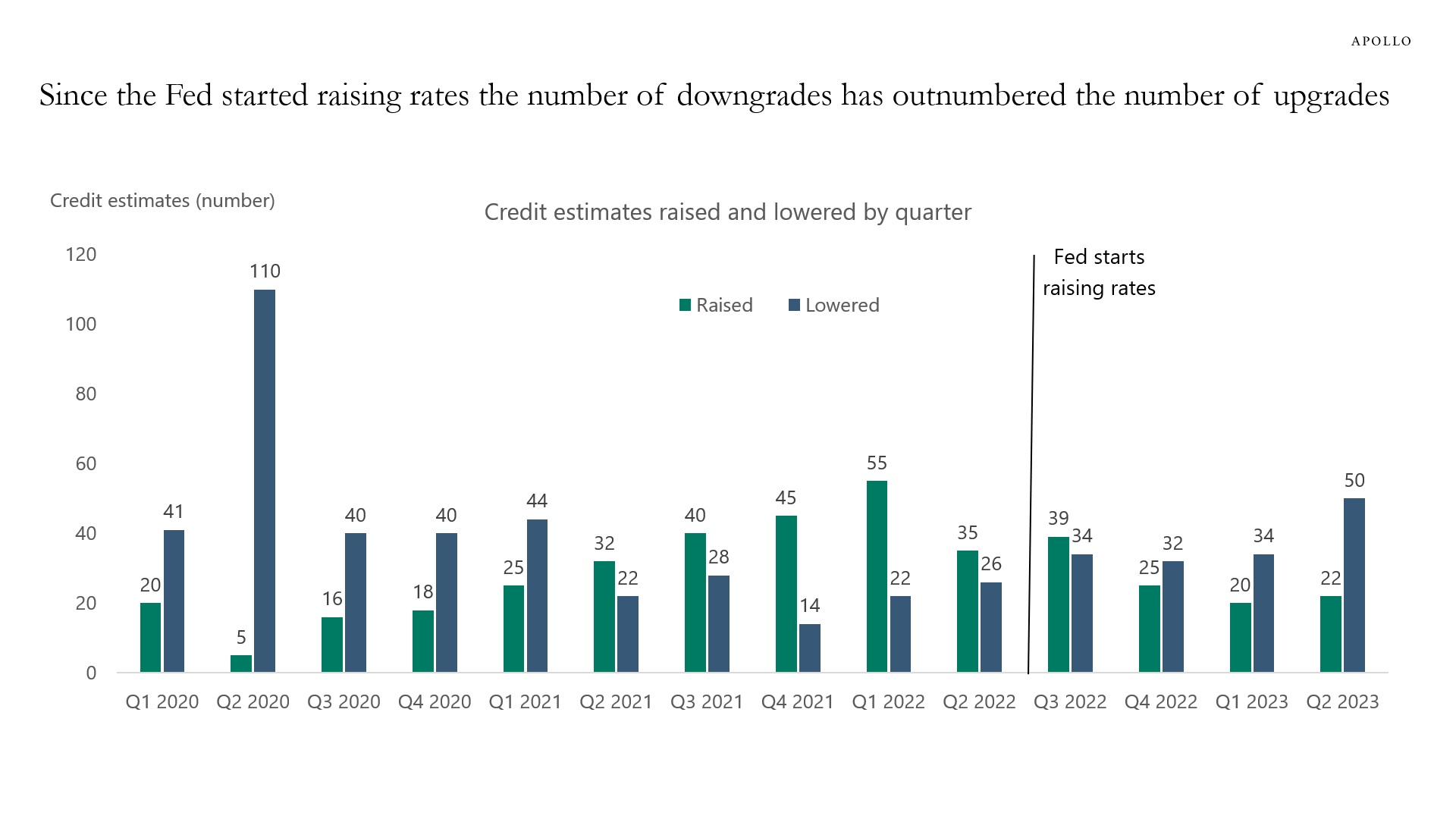

The Fed is trying to slow down the economy to slow down inflation. Specifically, the Fed is trying to slow down hiring, capex spending, and earnings growth.

The tool the FOMC has available is the cost of capital. By raising the cost of capital, the Fed makes it harder for firms to get new loans and to finance existing loans that are maturing.

This monetary policy transmission mechanism first hits companies with high leverage and little or no cash flow, e.g., tech, growth, and venture capital.

This is exactly what is happening at the moment. Companies with high debt and little cash flow are being downgraded, and there are now significantly more downgrades than upgrades, see chart below.

With the Fed funds rate staying at the current level for a couple of years, high cost of capital will continue to create problems for more and more companies characterized by high leverage and low earnings.

Source: S&P Global Ratings, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

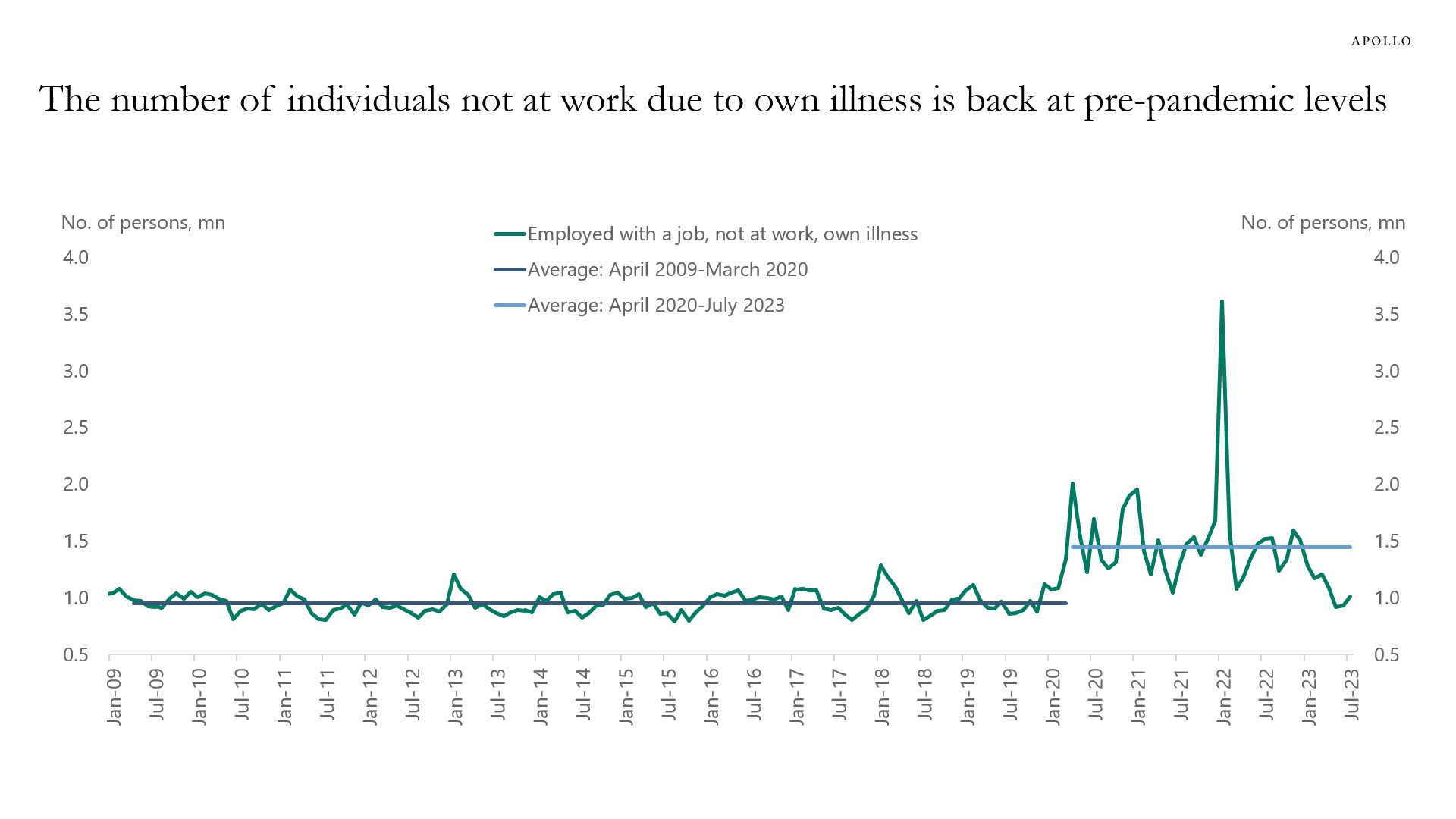

Before the pandemic, the number of workers not at work due to illness was around 1 million people every month. When the pandemic began, this number jumped to 1.5 million. But over the past six months, it has declined back to 1 million, see chart below.

Combined with the normalization in the participation rate and the employment-to-population ratio, the bottom line is that Covid is no longer holding back labor supply.

In other words, the source of strong wage growth has over the past six months shifted from the Covid-induced reduction in labor supply to labor demand. The implication for the Fed is that more demand destruction is needed to get wage inflation under control.

Source: BLS, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

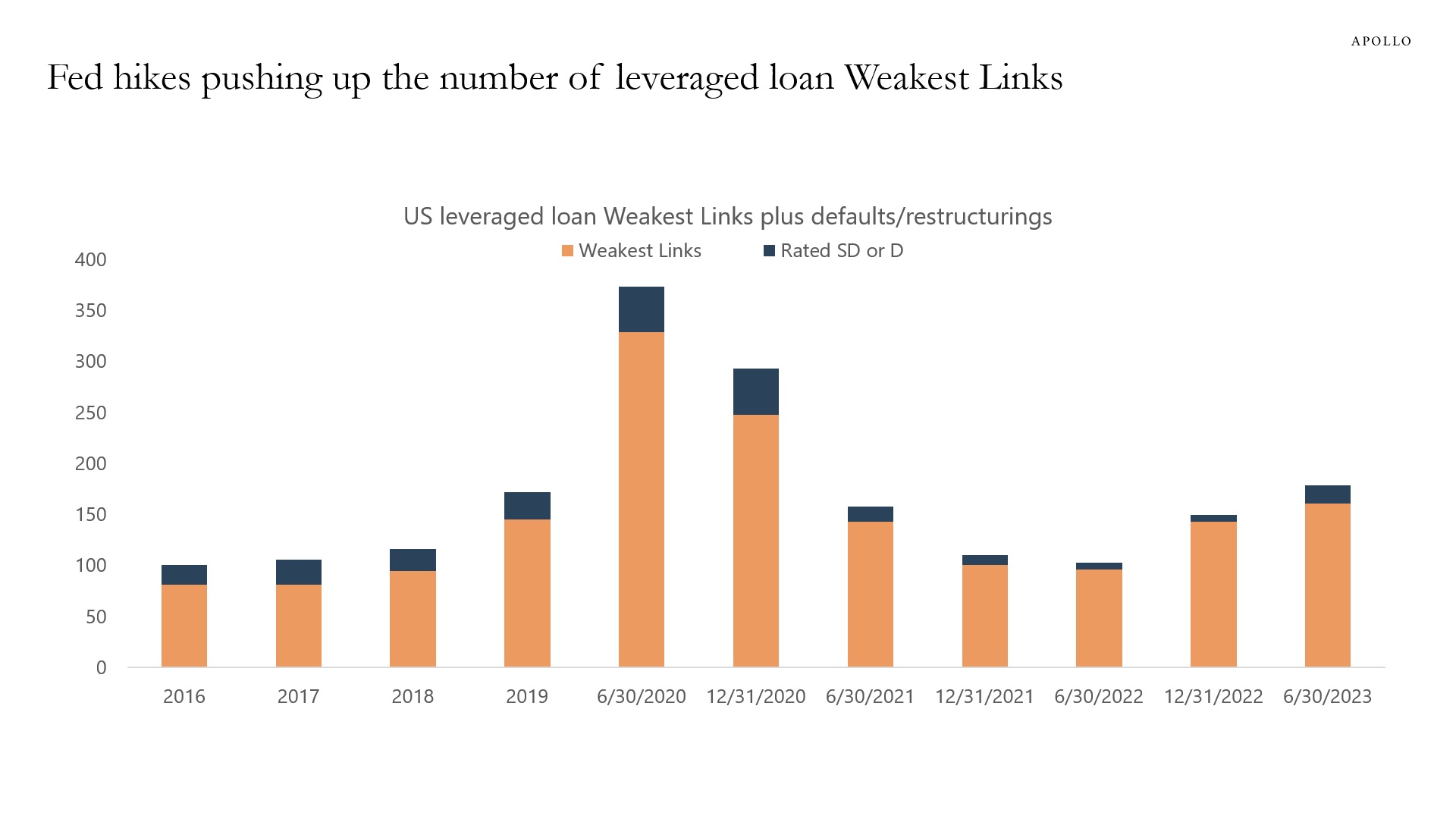

Weakest Links are loan issuers rated B-minus or lower with a negative outlook.

The number of US leveraged loan Weakest Links continues to increase, driven by higher costs of capital and costlier financing terms, see chart below.

This is how monetary policy works. Higher cost of capital makes it harder for more vulnerable companies to get financing.

Source: Pitchbook | LCD, Morningstar LSTA US Leveraged Loan Index, Apollo Chief Economist. Data through June 30, 2023. Note: SD and D – An obligor rated “SD” (Selective Default) or “D” has failed to pay one or more of its financial obligations (rated or unrated) when it came due. A “D” rating is assigned when Standard & Poor’s believes that the default will be a general default and that the obligor will fail to pay all or substantially all of its obligations as they come due. An “SD” rating is assigned when Standard & Poor’s believes that the obligor has selectively defaulted on a specific issue or class of obligations, but it will continue to meet its payment obligations on other issues or classes of obligations in a timely manner. See important disclaimers at the bottom of the page.

-

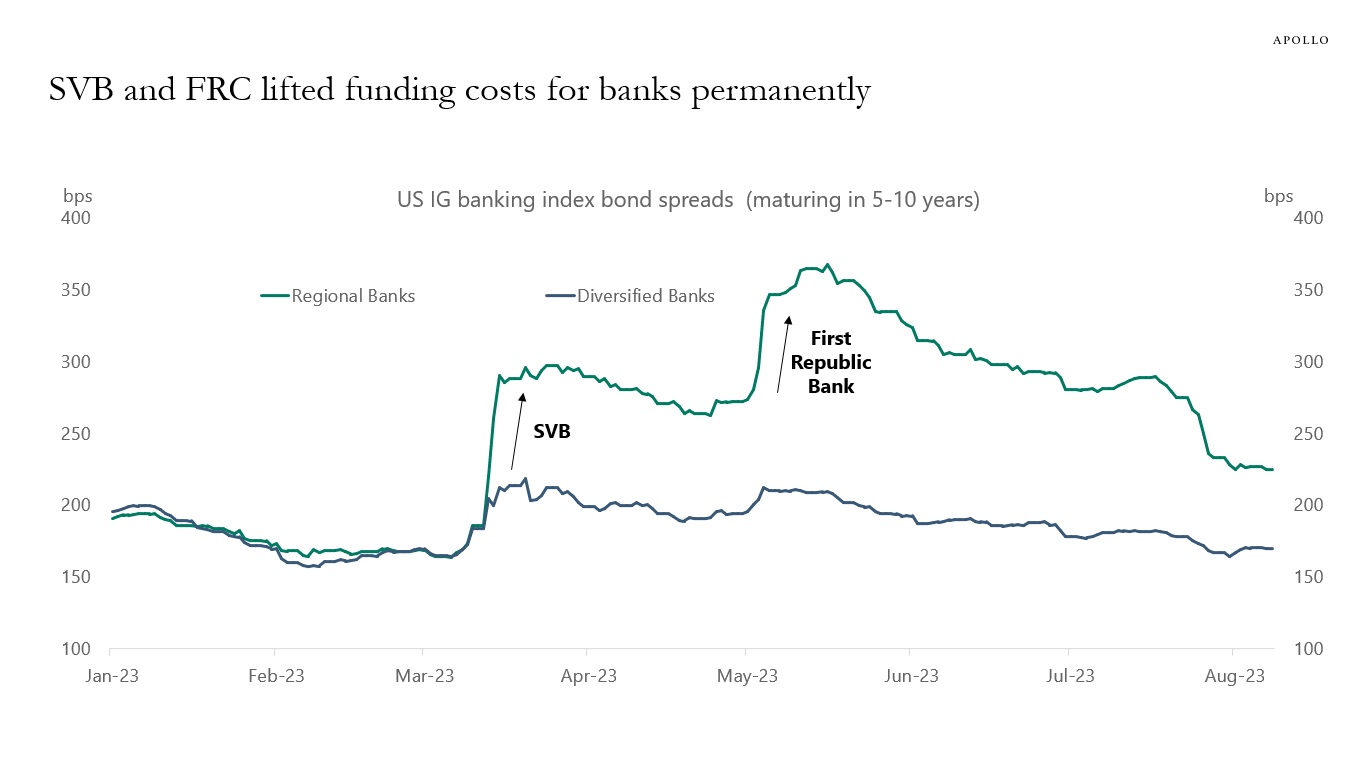

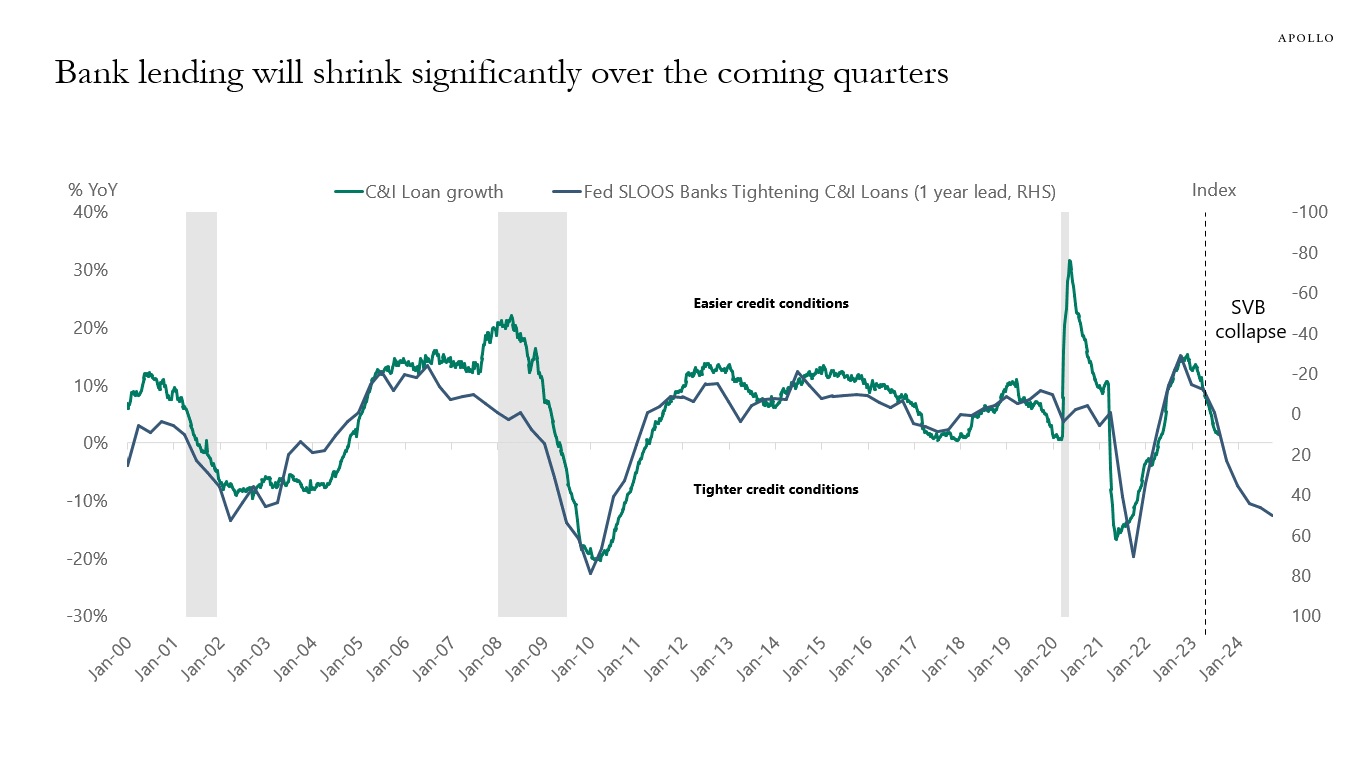

The costs of capital have increased because of Fed hikes and tighter credit conditions. As a result, there are firms every day that cannot get a new loan or refinance their maturing loan.

This is how monetary policy works. Higher costs of capital slow down financings and, ultimately, growth and inflation.

With the Fed saying that interest rates will stay high for “a couple of years,” this process will continue to slow down the economy. Our outlook for regional banks is available here and documents current trends in detail.

Source: FDIC, Apollo Chief Economist. Data as of Q3 2022.

Source: Census, Apollo Chief Economist

Source: FRB, Bloomberg, Apollo Chief Economist

Source: Federal Reserve Board, Haver Analytics, Apollo Chief Economist

Source: ICE BofA, Bloomberg, Apollo Chief Economist. Note: Unweighted average spreads of bonds from ICE 5-10 Year US Banking Index, C6PX Index for bonds issued before Jan 1, 2023. There are eight banks in the Regional index and 41 banks in the Diversified index. Regional banks include BankUnited, Citizens Financial, Huntington, and Zions. Diversified banks include JP Morgan, Citibank, and Bank of America.

Source: FRB, Haver Analytics, Apollo Chief Economist

Source: Conference Board, FRB, Haver Analytics, Apollo Chief Economist

Source: NFIB, FRB, Bloomberg, Apollo Chief Economist

Source: FRB, Bloomberg, Apollo Chief Economist

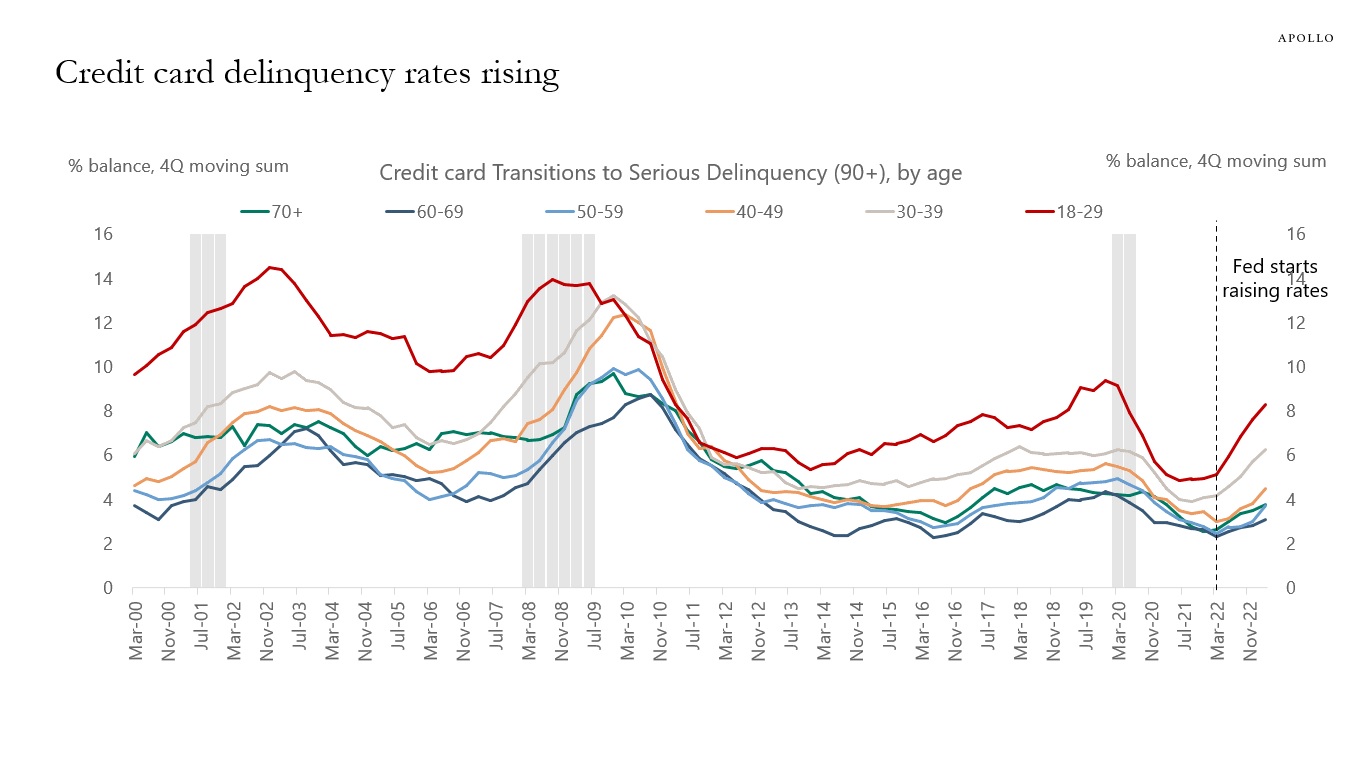

Source: New York Fed Consumer Credit Panel / Equifax, Apollo Chief Economist

Source: FRBNY Consumer Credit Panel, Equifax, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

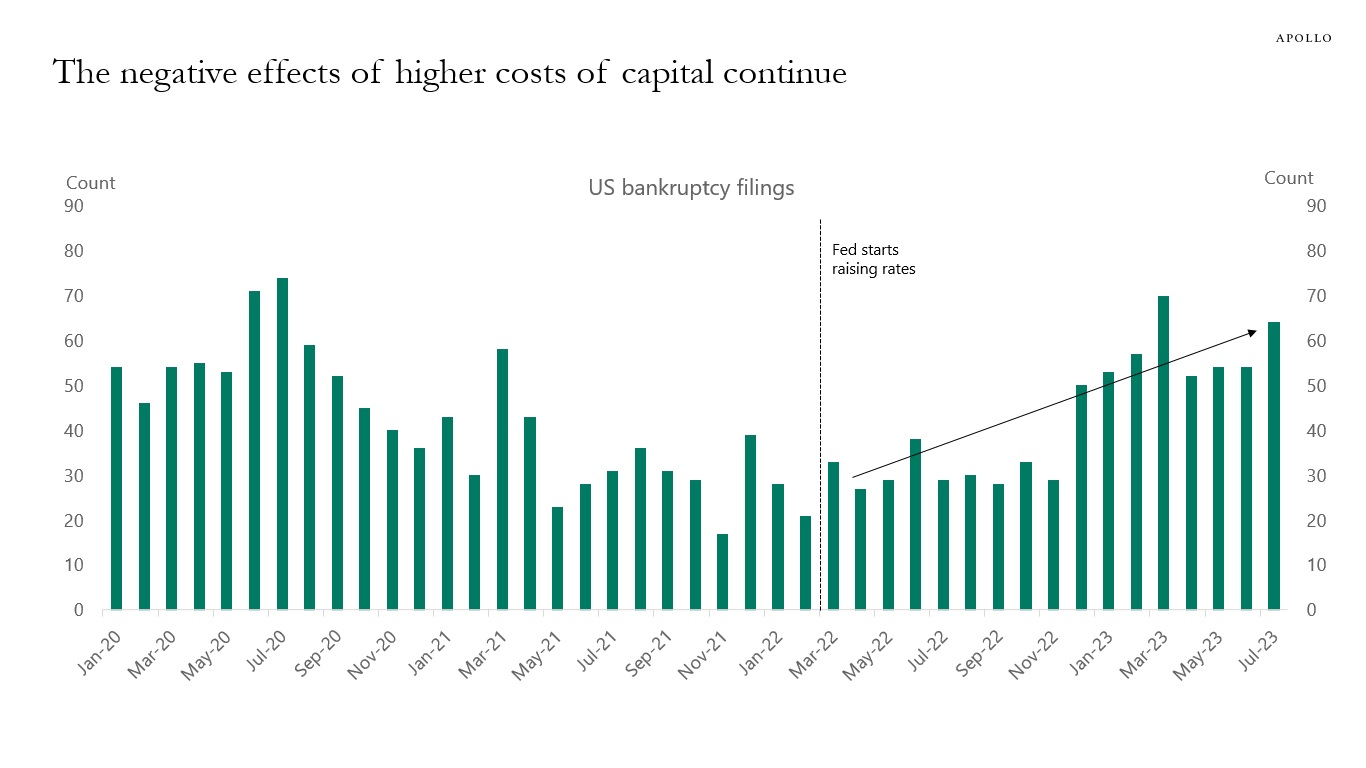

The Fed started raising rates in March 2022, and the effects are clear. Higher costs of capital have pushed more and more companies into bankruptcy. This is the idea behind raising rates: to slow the economy down with the ultimate goal of getting inflation back to 2%. Every day there are companies that cannot get new loans or refinance, and this trend higher in bankruptcies will continue as long as interest rates stay high.

Source: S&P Capital IQ, Bloomberg, Apollo Chief Economist. Note: Bankruptcy figures include public companies or private companies with public debt with a minimum of $2 million in assets or liabilities at the time of filing, in addition to private companies with at least $10 million in assets or liabilities. See important disclaimers at the bottom of the page.

-

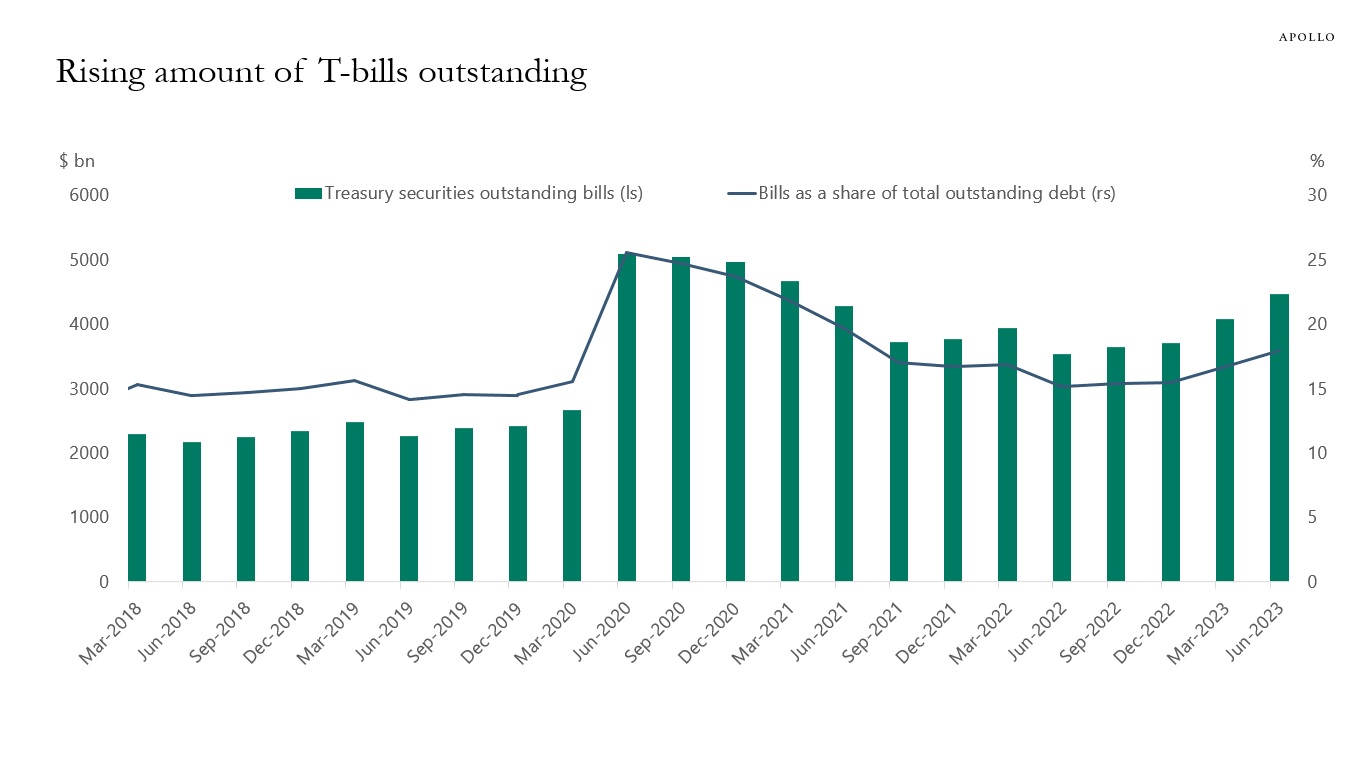

Arguments for US long rates moving higher are QT, the large government budget deficit, BoJ YCC exit, and the significant amount of T-bills outstanding, which need to be rolled into longer-dated Treasury bonds and notes, see chart below.

Arguments for US long rates moving lower are peaking inflation, slowing growth, and the Fed being done with raising rates.

Source: US Treasury, Haver, Apollo Chief Economist See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.